A long strangle is a two-leg options structure that combines a lower-strike long put and a higher-strike long call on the same underlying with the same expiration. It is built for two-sided price exposure, but it starts with a net debit: the combined premium paid for both options, plus any transaction costs.

Definition: A long strangle uses one long put below the current underlying price and one long call above it, usually with the same expiration date. The structure loses value at expiration if the underlying stays inside the middle zone, and it needs a move beyond one of two breakeven levels before the debit is overcome.

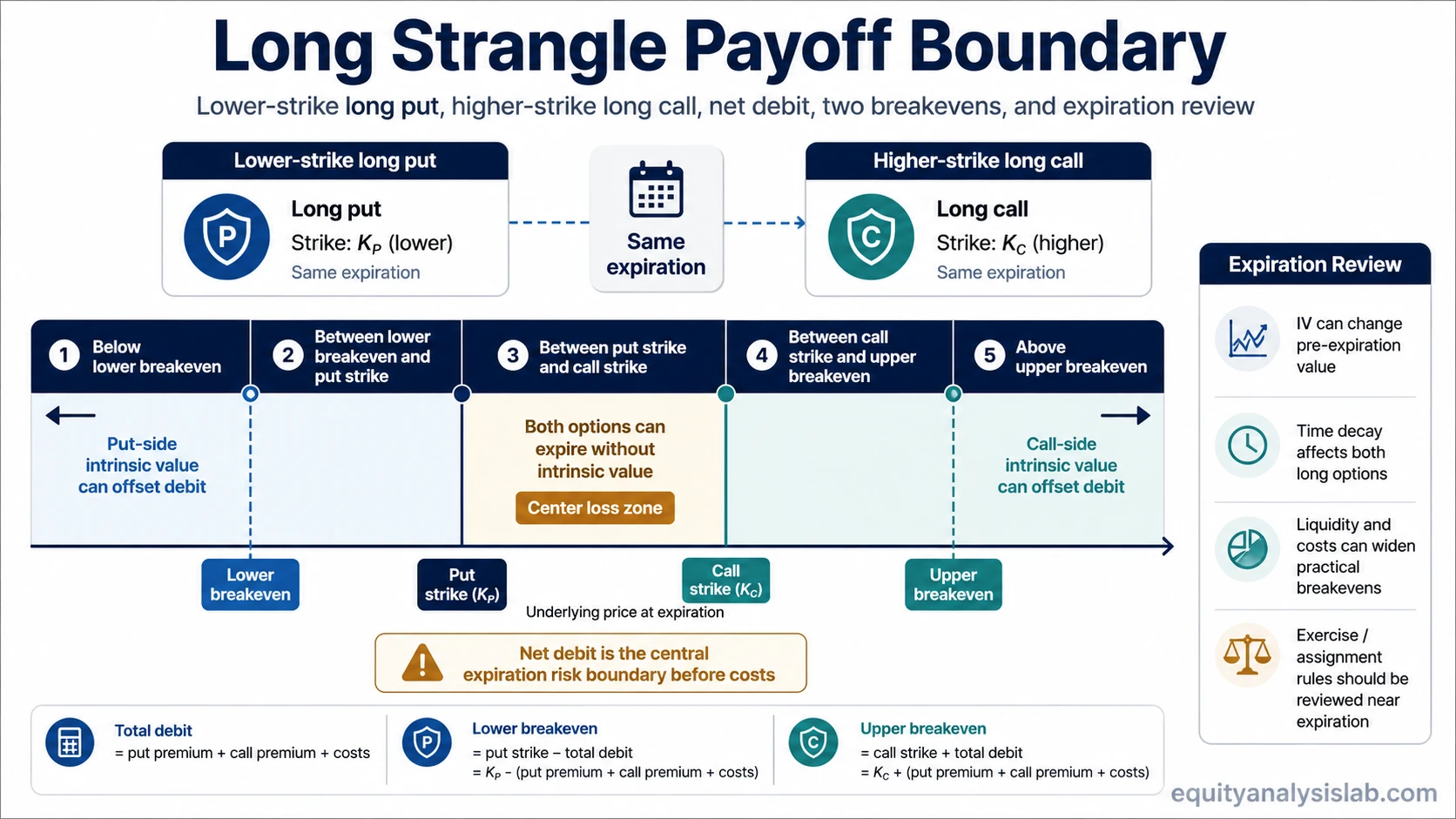

Key Points

- A long strangle has two long options: a lower-strike put and a higher-strike call.

- The maximum expiration loss is generally the total debit paid, plus costs, if both options expire out of the money.

- The lower breakeven is the put strike minus total debit; the upper breakeven is the call strike plus total debit.

- The structure has theoretical downside exposure through the put and theoretical upside exposure through the call, but the debit and costs push the required move farther away.

- Before expiration, implied volatility, time decay, bid-ask spreads, and remaining time can make the position value differ from the simple expiration payoff.

How a Long Strangle Is Structured

The structure has four core terms: the underlying, the put strike, the call strike, and the expiration date. The put strike sits below the call strike. Both options are long, so the position begins with premium paid rather than premium received.

The debit is the contract cost that the payoff must overcome. If the put costs 2.00 and the call costs 1.50, the total option debit is 3.50 before commissions, fees, and bid-ask effects. That debit is not just a cost line; it moves the two breakeven points farther away from the strikes.

Structure note: The long put creates downside exposure below the put strike. The long call creates upside exposure above the call strike. Between the two strikes, neither option has intrinsic value at expiration, so the debit is the central risk boundary.

How the Debit Creates the Payoff Boundary

At expiration, the long strangle has two outside breakevens. The lower breakeven is the put strike minus the total debit. The upper breakeven is the call strike plus the total debit. The underlying must finish below the lower breakeven or above the upper breakeven before the expiration payoff exceeds the debit, before costs.

The area between the put strike and the call strike is the full-debit loss zone at expiration. In that range, both options expire without intrinsic value. A move outside one strike can still be insufficient if it does not pass the relevant breakeven after accounting for the debit and costs.

| Expiration price zone | Option with intrinsic value | Payoff interpretation before costs |

|---|---|---|

| Below the lower breakeven | Long put | The put value exceeds the total debit, so the structure has positive expiration payoff before costs. |

| Between the lower breakeven and the put strike | Long put | The put has intrinsic value, but not enough to fully overcome the total debit. |

| Between the put strike and the call strike | Neither option | Both options expire without intrinsic value, creating the maximum expiration loss of the debit plus costs. |

| Between the call strike and the upper breakeven | Long call | The call has intrinsic value, but not enough to fully overcome the total debit. |

| Above the upper breakeven | Long call | The call value exceeds the total debit, so the structure has positive expiration payoff before costs. |

Observable Inputs That Shape the Payoff

A long strangle is easier to interpret when the observable inputs are separated from the payoff result. The important inputs are the underlying price, put strike, call strike, expiration, put premium, call premium, total debit, implied volatility, bid-ask spread, transaction costs, and the relevant exercise or assignment rules around expiration.

| Input | Why it matters |

|---|---|

| Put strike | Sets the downside strike where put intrinsic value begins at expiration. |

| Call strike | Sets the upside strike where call intrinsic value begins at expiration. |

| Total debit | Defines the maximum expiration loss before costs and pushes both breakevens away from the strikes. |

| Expiration | Determines when the simple expiration payoff map becomes final. |

| Implied volatility | Can increase or decrease option value before expiration even if the underlying has not crossed a breakeven. |

| Liquidity and costs | Bid-ask spreads, commissions, and fees can widen the practical distance between theoretical and realized outcomes. |

| Exercise and assignment rules | Expiration handling can vary by contract type and broker process, so the final position state needs review before expiration. |

Illustrative Breakeven Example

Assume an underlying is near 100. A long strangle uses a 95-strike put for 2.00 and a 105-strike call for 1.50, both with the same expiration. The total debit is 3.50 before costs.

The lower breakeven is 95 minus 3.50, or 91.50. The upper breakeven is 105 plus 3.50, or 108.50. At expiration, a finish at 94 would give the put 1.00 of intrinsic value, but that would still be less than the 3.50 debit. A finish at 100 would leave both options without intrinsic value. A finish beyond 91.50 or 108.50 would be needed before the expiration payoff clears the option debit, before costs.

What Can Change Before Expiration

The expiration payoff map is only one view of the structure. Before expiration, option value can change because of underlying movement, implied volatility, time remaining, bid-ask spreads, and the market’s pricing of both tails. A long strangle can gain or lose market value before either breakeven is crossed at expiration.

Time decay usually works against long premium positions because both options lose extrinsic value as expiration approaches, all else equal. Implied volatility can work in either direction: rising implied volatility may support option value, while falling implied volatility may reduce it. Liquidity also matters because wide spreads can make theoretical values harder to realize in practice.

Expiration review: Exercise, assignment, and auto-exercise handling can depend on contract specifications and broker procedures. The payoff diagram shows structural exposure, not every operational detail near expiration.

Common Misunderstandings and Limits

Limited max loss does not make the structure low-risk. The entire debit can be lost at expiration if the underlying stays between the two strikes. A defined loss boundary is still a real loss boundary.

A large move may still be too small. The underlying can move beyond one strike without clearing the relevant breakeven. The debit and costs determine how far the move must extend before expiration payoff turns positive before costs.

The payoff diagram is not the full pre-expiration value model. Implied volatility, time decay, liquidity, and remaining time can change the position’s market value before expiration.

A long strangle is not the same as a straddle. A long straddle uses the same strike for both the put and call, while a long strangle uses different strikes.

Related Structures

A long strangle belongs to the long-volatility side of options education because both legs are purchased and the structure depends on the relationship between debit, movement, time, and volatility. Directional debit spreads have a different payoff boundary.

- A bull call spread uses a bullish debit-spread structure with a long call and a higher-strike short call, creating capped upside exposure.

- A bear put spread uses a bearish debit-spread structure with a long put and a lower-strike short put, creating capped downside exposure.

- A short strangle is the opposite premium orientation because it sells both outside options; that changes the risk profile and should not be mixed with the long-strangle payoff map.

FAQ

What is the maximum loss on a long strangle?

The maximum expiration loss is generally the total debit paid for the put and call, plus costs, if the underlying finishes between the two strikes and both options expire without intrinsic value.

How are long strangle breakevens calculated?

The lower breakeven is the put strike minus the total debit. The upper breakeven is the call strike plus the total debit. Costs can make the practical breakevens wider than the simple formula.

Can a long strangle change value before expiration?

Yes. Before expiration, the structure can change value because of underlying movement, implied volatility, time decay, remaining time, and liquidity, even before the final expiration payoff is known.