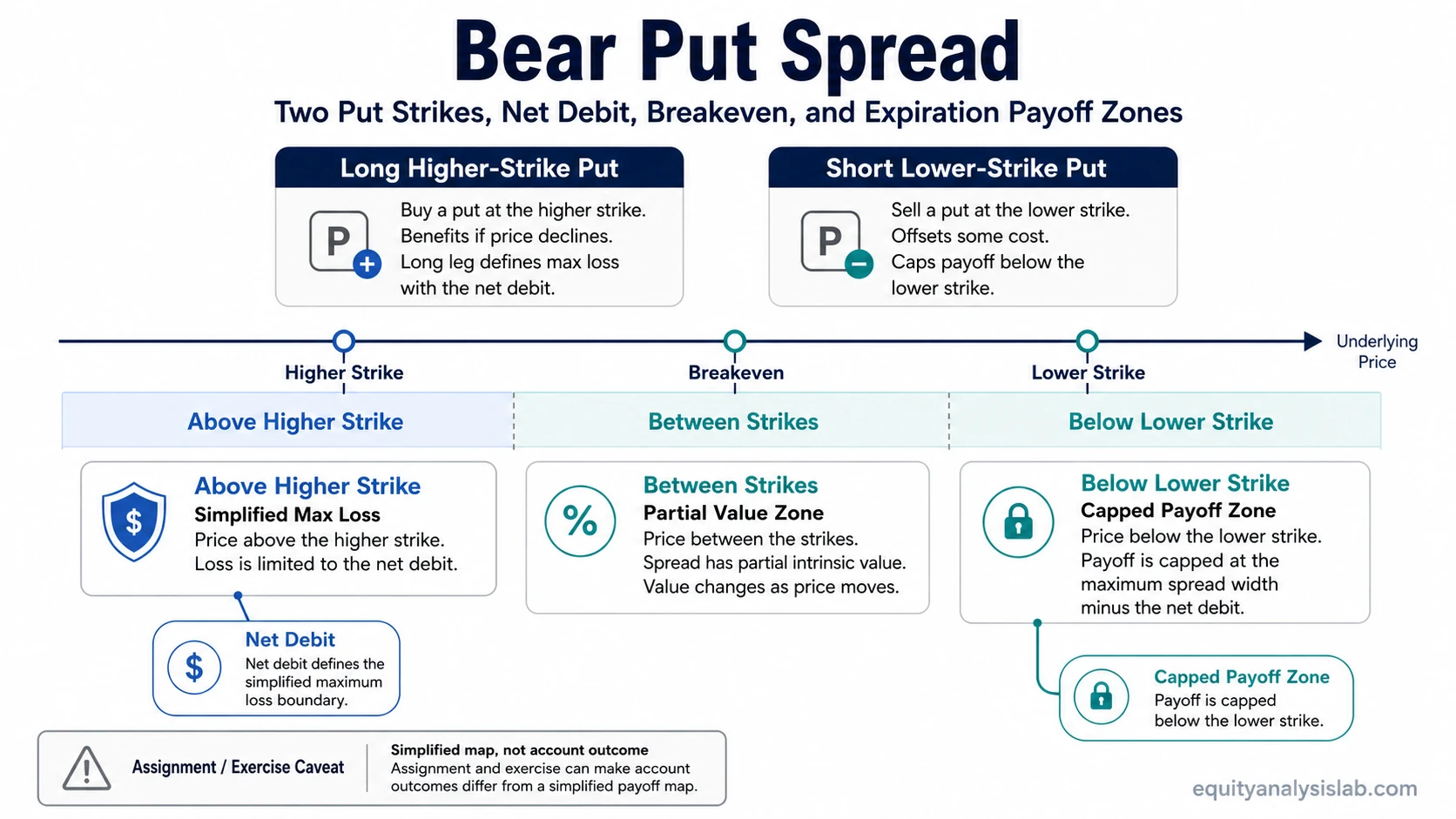

A bear put spread is a two-leg put option spread that combines a long higher-strike put with a short lower-strike put on the same underlying and expiration. The position is usually entered for a net debit, which creates a defined maximum loss under simplified assumptions and a capped maximum profit if the underlying finishes below the lower strike at expiration.

The structure is bearish in payoff shape, but it is not a forecast, recommendation, or safety label. It defines a risk and reward boundary around two put strikes while leaving assignment, exercise, liquidity, transaction costs, and pre-expiration pricing outside the simplified payoff diagram.

Key Points

- A bear put spread uses one long higher-strike put and one short lower-strike put with the same expiration.

- The spread is usually opened for a net debit.

- Maximum loss is the net debit paid under simplified assumptions, excluding commissions and fees.

- Maximum profit is the strike width minus the net debit under simplified assumptions, excluding commissions and fees.

- Breakeven is the higher strike minus the net debit under simplified assumptions.

- Assignment, exercise, liquidity, and transaction costs can make real outcomes differ from a simplified payoff chart.

What Is a Bear Put Spread?

Bear put spread definition: A bear put spread is a defined-risk bearish put debit spread built by buying a put at a higher strike and selling another put at a lower strike, usually with the same underlying asset and the same expiration date.

The long put creates downside exposure below the higher strike. The short put helps reduce the net cost of the spread, but it also caps the maximum profit below the lower strike and introduces assignment and exercise considerations.

Because both legs use puts with the same expiration, the structure is a vertical spread. The important boundary is the distance between the two strikes compared with the net debit paid for the spread.

Bear Put Spread Components

The components of a bear put spread define the payoff before any interpretation about market direction. The spread only works as a clean concept when the strikes, expiration, underlying, and net debit are kept separate.

| Component | Role in the spread | Risk boundary effect |

|---|---|---|

| Long higher-strike put | Gains intrinsic value as the underlying falls below the higher strike. | Creates the main bearish payoff exposure. |

| Short lower-strike put | Brings in premium that reduces the net debit. | Caps the payoff below the lower strike and can create assignment risk. |

| Same expiration | Keeps the spread as a vertical put spread. | Makes expiration payoff easier to map across price zones. |

| Same underlying | Keeps both legs tied to the same asset. | Prevents the position from becoming a cross-asset or pairs structure. |

| Net debit | The cost paid for the spread after premium received from the short put. | Usually represents the maximum loss under simplified assumptions. |

Bear Put Spread Payoff, Max Profit, Max Loss, and Breakeven

The payoff of a bear put spread depends on three numbers: the higher strike, the lower strike, and the net debit. The higher strike sets where the long put starts gaining intrinsic value. The lower strike sets where the spread stops gaining additional intrinsic value at expiration.

Maximum loss: net debit paid, excluding commissions and fees.

Maximum profit: strike width minus net debit, excluding commissions and fees.

Breakeven: higher strike minus net debit.

These formulas describe a simplified expiration payoff. Before expiration, the market value of the spread can also reflect implied volatility, time remaining, liquidity, interest rates, dividends where relevant, and the bid-ask spread of each option leg.

| Underlying price at expiration | Payoff zone | What the simplified payoff means |

|---|---|---|

| Above the higher strike | Outside the spread payoff range | Both puts typically expire out of the money, and the loss is limited to the net debit paid under simplified assumptions. |

| Between the two strikes | Partial intrinsic value zone | The long put has intrinsic value, while the short put is usually out of the money. Profit or loss depends on price relative to breakeven. |

| Below the lower strike | Capped maximum payoff zone | Both puts are typically in the money, and the spread value is capped near the strike width under simplified assumptions. |

Bear Put Spread Example

Assume a hypothetical bear put spread uses a 100-strike long put and a 95-strike short put with the same expiration. If the long put costs 4.00 and the short put brings in 1.50, the net debit is 2.50.

Higher strike: 100

Lower strike: 95

Strike width: 5.00

Net debit: 2.50

Maximum loss: 2.50, excluding commissions and fees

Maximum profit: 5.00 – 2.50 = 2.50, excluding commissions and fees

Breakeven: 100 – 2.50 = 97.50

If the underlying finishes above 100 at expiration, both puts are usually out of the money and the simplified loss is the 2.50 debit. If it finishes at 97.50, the simplified expiration payoff is near breakeven. If it finishes below 95, the simplified spread value is near 5.00, so the profit is capped near 2.50 after subtracting the debit.

What Happens at Expiration?

Expiration changes the spread from a market-priced option position into an exercise and assignment question. The simplified payoff table is useful, but it does not remove contract mechanics.

| Expiration price zone | Long higher-strike put | Short lower-strike put | Potential result |

|---|---|---|---|

| Above the higher strike | Usually out of the money | Usually out of the money | Both legs may expire worthless, leaving the net debit as the simplified loss. |

| Between the strikes | Usually in the money | Usually out of the money | The long put may be exercised or closed, while the short put may expire worthless. |

| Below the lower strike | Usually in the money | Usually in the money | The long put and short put can offset much of the price movement, but assignment and exercise processing still matter. |

Assignment and exercise caveat: A short put can be assigned, especially when it is in the money. A long put can also be exercised or may require action depending on the account, broker, and expiration procedures. The simplified spread payoff should not be treated as the same thing as the operational outcome in an account.

How Volatility and Time Affect a Bear Put Spread

Before expiration, a bear put spread is not valued only by the final payoff formula. Implied volatility, time remaining, and the relative sensitivity of both option legs can change the spread’s market value.

| Input | How it can affect the spread before expiration | Boundary to remember |

|---|---|---|

| Implied volatility | Can change the value of both the long put and the short put. | The net effect is not identical to holding a single long put because the short put offsets part of the exposure. |

| Time remaining | Can affect both legs as extrinsic value changes. | Time decay is path-dependent and should not be simplified into “always good” or “always bad.” |

| Bid-ask spread and liquidity | Can affect the cost to enter, close, or adjust the spread. | Payoff formulas normally exclude execution frictions. |

| Commissions and fees | Can reduce the realized result compared with simplified payoff math. | Formula examples usually exclude these costs unless stated otherwise. |

How to Close a Bear Put Spread

Closing a bear put spread generally means offsetting both legs: selling the long higher-strike put and buying back the short lower-strike put. That converts the spread back into cash value based on the market prices available at the time.

Closing only one leg changes the structure. For example, removing the short put leaves a different risk profile from removing the long put. The mechanics can also depend on option liquidity, bid-ask spreads, assignment status, broker procedures, and time remaining before expiration.

Non-advisory boundary: Closing mechanics can be described without implying that a spread should be opened, closed, held, rolled, or exercised. Operational outcomes can depend on account permissions, contract status, risk tolerance, and the investor’s own process.

Bear Put Spread vs Related Option Spreads

A bear put spread is easiest to understand when it is separated from nearby spread structures. The defining traits are put options, a net debit, a higher-strike long put, a lower-strike short put, and the same expiration.

| Structure | Main difference from a bear put spread | Why the distinction matters |

|---|---|---|

| Bull Call Spread | Uses call options and has a bullish debit-spread payoff shape. | It is not a bearish put debit spread. |

| bull put spread structure | Uses puts but is usually a bullish credit spread. | The debit versus credit distinction changes the payoff boundary and risk framing. |

| Long put | Uses only the long put leg and does not sell a lower-strike put. | It has different cost, volatility exposure, and profit potential from a capped two-leg spread. |

| multi-leg range spread | Uses more legs and is usually centered around a range or target zone. | It is not the same as a two-strike bearish put debit spread. |

Common Misunderstandings

Defined risk does not mean safe. A bear put spread can define the maximum debit at risk under simplified assumptions, but the position can still lose money and can still be affected by liquidity, assignment, timing, and transaction costs.

A payoff chart is not the whole account outcome. Payoff charts usually show simplified expiration values. They may not show early assignment, exercise processing, bid-ask spreads, commissions, margin treatment, or operational constraints.

The short put is not just a cost reducer. Selling the lower-strike put lowers the net debit, but it also caps the payoff and creates assignment exposure if the contract is in the money.

FAQ

What is a bear put spread?

A bear put spread is a two-leg put debit spread that buys a higher-strike put and sells a lower-strike put with the same expiration. The structure usually has a defined maximum loss equal to the net debit and a capped maximum profit equal to the strike width minus the debit, excluding commissions and fees.

What is the maximum loss on a bear put spread?

The simplified maximum loss is generally the net debit paid for the spread, excluding commissions and fees. This assumes the spread is held to expiration and both puts expire out of the money.

What is the maximum profit on a bear put spread?

The simplified maximum profit is generally the difference between the two strikes minus the net debit paid, excluding commissions and fees. This maximum is usually reached at expiration when the underlying finishes below the lower strike.

What is the breakeven on a bear put spread?

The simplified breakeven is generally the higher strike minus the net debit paid. For example, if the higher strike is 100 and the net debit is 2.50, the breakeven is 97.50.

How do you close a bear put spread?

Closing generally means offsetting both legs by selling the long higher-strike put and buying back the short lower-strike put. Closing only one leg changes the risk profile and should not be treated as the same spread.

Can assignment matter in a bear put spread?

Yes. The short lower-strike put can be assigned if it is in the money, and the long put may also involve exercise decisions or broker procedures. Assignment and exercise mechanics can make real outcomes differ from a simplified payoff chart.