A bull put spread is a defined-risk put credit spread built by selling a higher-strike put and buying a lower-strike put with the same expiration. The position receives a net credit, but the short put still creates assignment risk.

Definition: A bull put spread combines a short put at a higher strike with a long put at a lower strike. The credit received is the most the spread can keep before costs, while the distance between the strikes minus that credit defines the maximum loss before costs.

The structure is bounded, not risk-free. The long put limits losses beyond the lower strike at expiration, but it does not erase the obligation created by the short put. The spread is clearer when read through payoff, credit, volatility and time, and assignment exposure.

Key Points

- A bull put spread is a same-expiration vertical put credit spread.

- The higher-strike put is sold, and the lower-strike put is bought.

- Maximum profit equals the net credit received before costs.

- Maximum loss equals the strike width minus the net credit before costs.

- Breakeven equals the short put strike minus the net credit.

- The short put can still be assigned, even though the long put limits the final downside at expiration.

How to Read the Structure

First, identify the two legs: the short higher-strike put creates the obligation, and the long lower-strike put limits the downside at expiration.

Second, read the credit: the net credit sets the maximum possible gain before costs and lowers the breakeven below the short strike.

Third, map the expiration zones: the outcome changes above the short strike, between the strikes, at breakeven, and below the long strike.

Fourth, review the path risk: volatility, time remaining, liquidity, and assignment can affect the account before the expiration payoff is reached.

How a Bull Put Spread Is Built

A bull put spread has two put option legs on the same underlying and the same expiration date. The short put is placed at the higher strike, and the long put is placed at the lower strike. Because the higher-strike put usually has more value than the lower-strike put, the structure opens for a net credit.

| Component | Role in the spread | Risk effect |

|---|---|---|

| Short higher-strike put | Creates the main obligation and brings in premium | Assignment risk and downside exposure begin around the short strike |

| Long lower-strike put | Caps further downside beyond the lower strike | Maximum loss is bounded once price is below the long strike at expiration |

| Net credit | Reduces the net cost basis of the spread | Sets maximum profit and moves breakeven below the short strike |

| Strike width | Measures the distance between the short and long put strikes | Forms the gross downside range before subtracting the credit |

| Same expiration | Keeps the structure as a vertical put spread | Creates one expiration payoff map rather than a calendar exposure |

The spread is often described as a put credit spread because the net premium is received at entry. That credit changes the economics, but it does not remove the short-put obligation or the need to understand the expiration payoff zones.

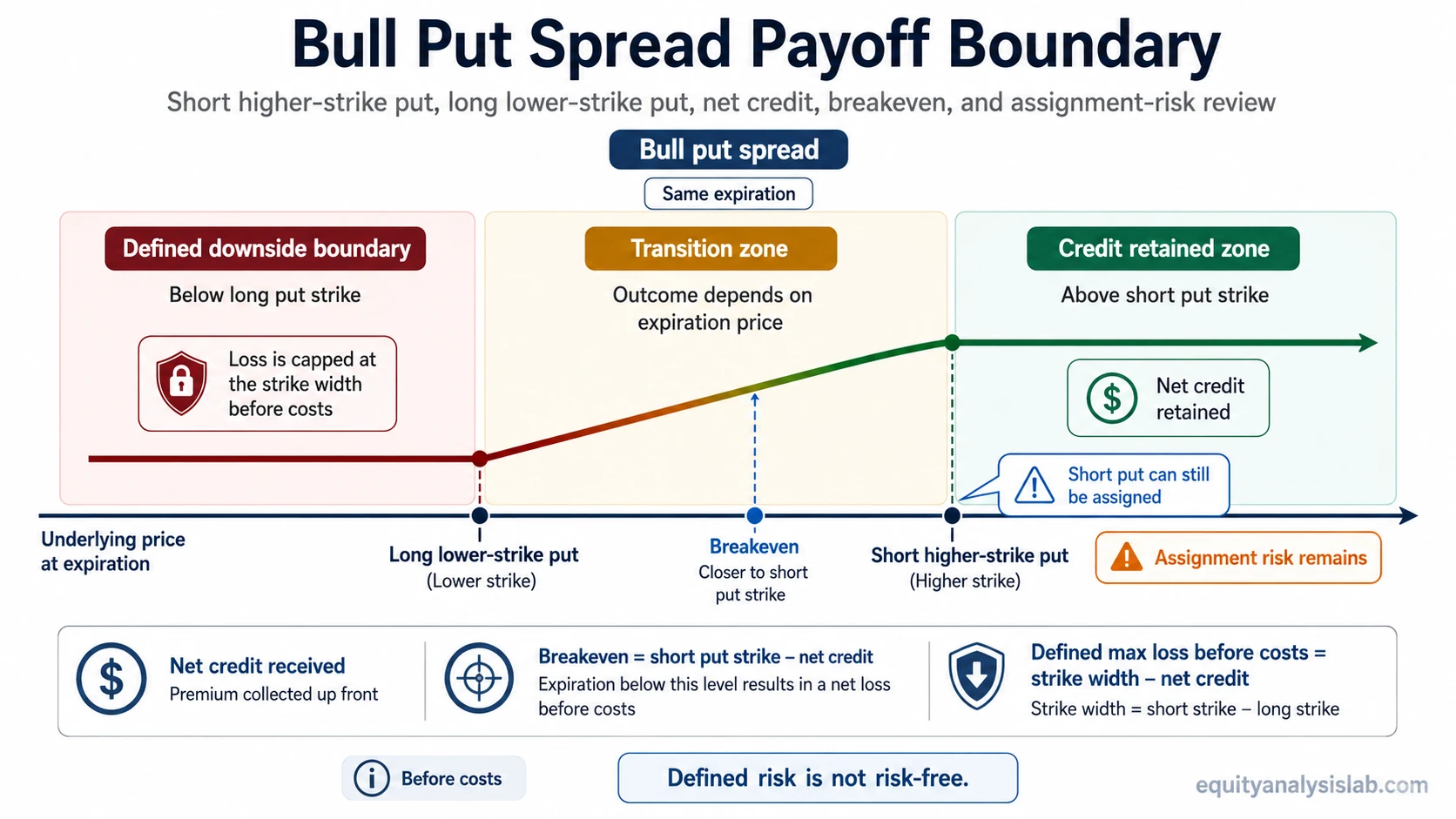

Payoff Boundary

The payoff is controlled by the short strike, the long strike, the net credit, and the underlying price at expiration. The spread has a capped gain because the maximum gain is limited to the credit received. It also has a capped expiration loss because the long put offsets further losses below the lower strike.

| Expiration zone | What happens to the spread | Payoff interpretation |

|---|---|---|

| Above the short put strike | Both puts expire out of the money before costs and contract-specific effects | The spread keeps the net credit before costs |

| Between the two strikes | The short put has intrinsic value, while the long put may remain out of the money | Profit or loss depends on how far the expiration price is below the short strike |

| At breakeven | The short-put loss equals the credit received | The spread is approximately flat before costs |

| Below the long put strike | Both puts are in the money | The maximum loss is reached before costs because the long put caps further downside |

The formulas are compact, but each formula describes only the expiration map before costs and account-specific effects:

Maximum profit: net credit received.

Maximum loss: strike width minus net credit.

Breakeven: short put strike minus net credit.

Premium and Credit Boundary

The net credit is the premium received from the short put minus the premium paid for the long put. It is not a separate source of safety. It shifts the payoff map by reducing the net loss and creating the maximum possible gain before costs.

A higher credit can make the breakeven lower, but it usually exists because the spread is carrying meaningful short-put exposure. The credit should be read as part of the risk structure, not as a stand-alone benefit.

Defined risk is not no risk: the long put limits the final downside at expiration, but the spread can still lose money, require capital, change value before expiration, and create assignment exposure through the short put.

Volatility and Time Boundary

A bull put spread is exposed to changes in option value before expiration. Time decay often affects a net-credit spread differently from a single long option because both legs lose time value. The short put may benefit from time decay, while the long put can lose value as time passes.

Implied volatility can also change the spread value before expiration. A rise in implied volatility can increase put values and make the spread more expensive to close, especially if the underlying price moves closer to or below the short strike. A fall in implied volatility can reduce put values, but the effect depends on both legs, strike distance, time remaining, and liquidity.

| Input | Why it matters | Common misread |

|---|---|---|

| Time remaining | More time leaves more room for the spread value to change | Assuming the expiration payoff map describes the full path before expiration |

| Implied volatility | Higher option values can change the mark-to-market value of both legs | Reducing volatility exposure to a simple “high IV is good” rule |

| Liquidity | Bid-ask spreads and execution costs can affect the account impact | Treating formula values as identical to realized account outcomes |

Assignment and Exercise Boundary

The short put is the leg that creates assignment risk. If assigned, the short put can create an obligation to buy shares at the short strike. The long put can limit the overall downside at expiration, but it does not prevent the assignment notice from occurring on the short leg.

Assignment risk can matter before expiration, especially when the short put is in the money, extrinsic value is low, or contract terms make exercise more likely. The long put may provide a hedge against further downside, but the account can still face position, margin, cash, timing, and exercise-management consequences.

Risk limitation: maximum loss formulas describe the defined expiration boundary before costs. They do not remove early assignment risk, liquidity risk, margin effects, transaction costs, tax effects, or the practical account impact of carrying the spread before expiration.

Simple Bull Put Spread Example

Consider a generic bull put spread with a short put at 50 and a long put at 45. If the spread receives a net credit of 1.50, the strike width is 5.00.

| Item | Calculation | Result before costs |

|---|---|---|

| Net credit | Credit received from short put minus debit paid for long put | 1.50 |

| Maximum profit | Net credit | 1.50 |

| Maximum loss | 5.00 strike width – 1.50 credit | 3.50 |

| Breakeven | 50 short strike – 1.50 credit | 48.50 |

If the underlying finishes above 50 at expiration, both puts expire out of the money before costs and the spread keeps the credit. Between 50 and 45, the short put has intrinsic value and the result depends on whether the expiration price is above or below the 48.50 breakeven. Below 45, the long put caps the expiration loss at the strike width minus the credit before costs.

Why the example matters: the credit improves the breakeven compared with the short strike, but it does not make the spread harmless. The downside boundary remains tied to the distance between the strikes, and the short put remains the assignment-sensitive leg.

Bull Put Spread vs Related Spreads

A bull put spread belongs to the broader credit spread family because it receives a net credit and contains one short option with one protective long option. The exact structure matters because different spread families have different premium timing, payoff boundaries, and assignment profiles.

| Related structure | Main distinction | Why the distinction matters |

|---|---|---|

| Bull call spread | Uses calls and usually opens for a debit | Premium timing differs, and the structure does not create the same short-put assignment obligation |

| Bear put spread | Uses puts but expresses a bearish debit structure | The payoff direction and premium setup differ from a bullish or neutral put credit spread |

| Short put | Contains only the short-put obligation without the lower-strike protective put | The downside is not capped by a paired long put in the same way |

| Options spread structures | Groups spreads by payoff, premium, volatility, expiration, and range behavior | The broader map helps separate vertical spreads from range, wing, and expiration-based structures |

The important distinction is not only whether a spread is bullish or bearish. Premium direction, option type, expiration structure, and short-leg obligation all change how the position behaves.

Common Misunderstanding

Mistake: treating the received credit as protection against the full downside.

Cleaner interpretation: the credit reduces the net loss and sets the maximum gain, but the defined-risk boundary still depends on the distance between the short put and long put strikes. Assignment risk remains attached to the short put.

A bull put spread can have a clearly defined maximum loss at expiration and still carry meaningful risk before expiration. Option value, implied volatility, liquidity, early assignment, and account requirements can all affect the path before the final payoff boundary is reached.

FAQ

Is a bull put spread the same as a put credit spread?

A bull put spread is a type of put credit spread. It sells a higher-strike put and buys a lower-strike put with the same expiration, usually creating a net credit and a defined expiration risk boundary.

What is the maximum profit on a bull put spread?

The maximum profit is the net credit received before costs. That outcome occurs when both puts expire out of the money at expiration.

What is the maximum loss on a bull put spread?

The maximum loss before costs is the strike width minus the net credit. The long lower-strike put caps further downside at expiration.

Can the short put in a bull put spread be assigned?

Yes. The short put can be assigned. The long put can limit the overall downside boundary, but it does not eliminate the assignment risk attached to the short put.

Does defined risk mean a bull put spread is low risk?

No. Defined risk means the expiration loss is bounded by the structure before costs. It does not mean the risk is small, risk-free, or free from liquidity, assignment, margin, or timing effects.