A credit spread in options is a spread where the option sold brings in more premium than the option bought, creating a net credit. The structure is often shown through a simplified expiration payoff boundary, but its value before expiration can also change with implied volatility, time decay, liquidity, and assignment or exercise risk.

In bond markets, credit spread can also refer to the yield difference between debt instruments with different credit risk. In this context, the term refers to an options spread structure, not a macro credit-risk indicator.

What a Credit Spread Means in Options

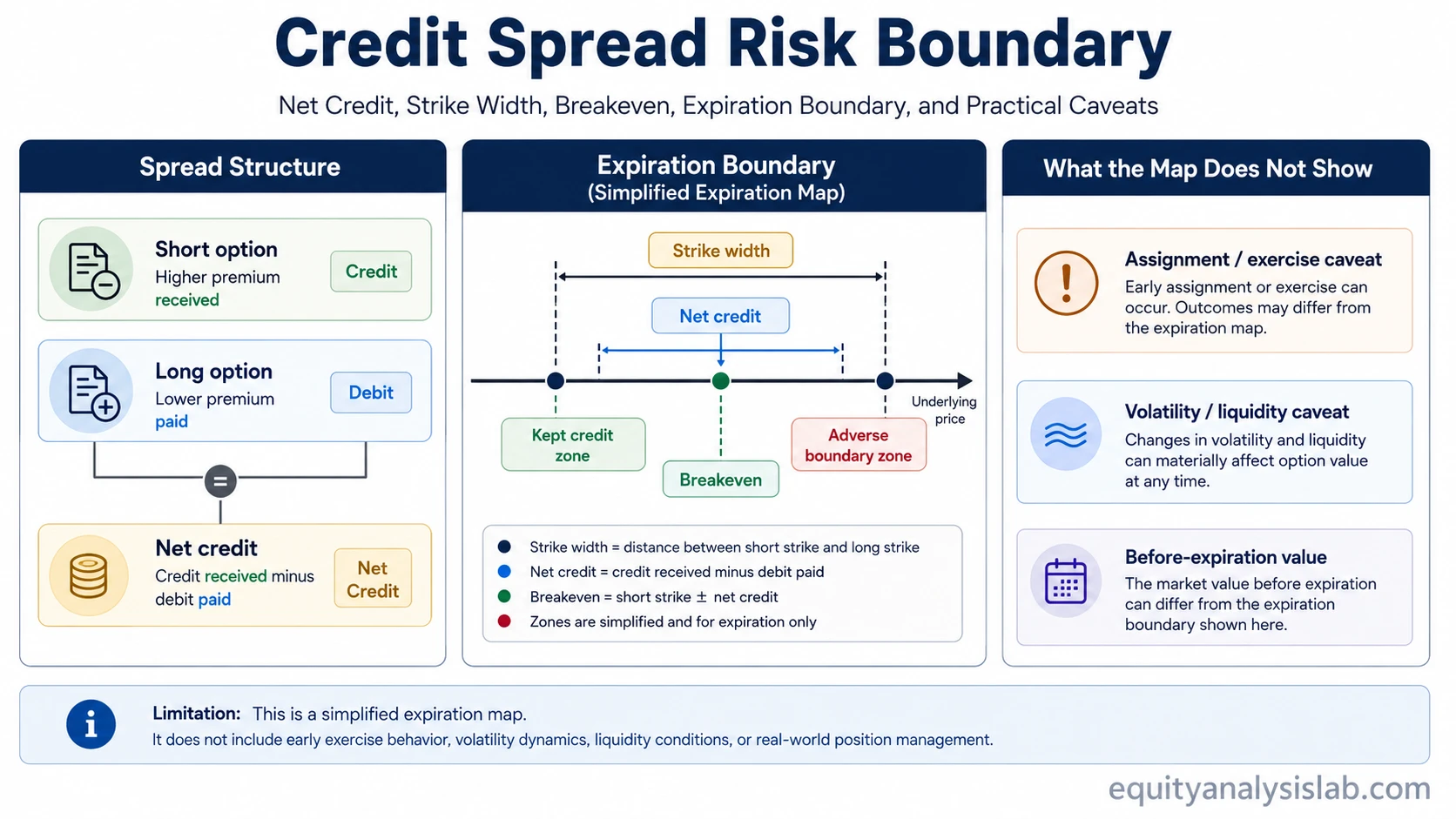

A standard vertical options credit spread combines a short option and a long option on the same underlying asset, with the same expiration and the same option type, but with different strike prices. The short option receives more premium than the long option costs, so the opening premium flow is a net credit.

Credit spread definition: a credit spread is an options spread that starts with premium received, because the sold option has a higher premium than the purchased option. The long option helps define the spread boundary, while the short option creates the initial credit.

The net credit is not the same as guaranteed profit. It is the initial premium difference before transaction costs, contract assignment, exercise behavior, liquidity, and mark-to-market changes are considered.

Credit Spread Anatomy

The structure is easier to read when the premium flow, strike width, expiration, and risk boundary are separated. A credit spread is not only a two-leg order; it is a defined payoff structure whose simplified result depends on where the underlying finishes at expiration.

| Component | Role in a credit spread | Risk boundary note |

|---|---|---|

| Short option | The sold option receives the larger premium. | This leg creates assignment or exercise exposure before expiration. |

| Long option | The bought option costs less than the premium received from the short option. | This leg helps define the simplified spread boundary. |

| Net credit | Premium received minus premium paid. | It is the initial credit, not a guaranteed outcome. |

| Strike width | The distance between the two strike prices. | Strike width helps determine the simplified maximum loss boundary. |

| Expiration | Both legs usually share the same expiration. | The standard payoff map describes the expiration result, not every before-expiration path. |

| Breakeven | The underlying price where the simplified expiration result moves from profit to loss, before costs. | The breakeven formula differs between put and call credit spreads. |

| Volatility and liquidity | Implied volatility and bid-ask spreads can change the spread’s market value before expiration. | A clean payoff diagram can hide these practical changes. |

Credit Spread Payoff Boundary

A simplified credit spread payoff map usually focuses on three ideas: the maximum credit that can be kept, the maximum loss boundary, and the breakeven price at expiration. This model is useful, but it should be read as an expiration framework rather than a complete position-management model.

In simplified expiration terms, maximum profit is usually the net credit received, before costs and practical complications. Simplified maximum loss is usually the strike width minus the net credit, before costs and before any assignment, exercise, or liquidity issue changes the practical result.

Simplified example: if a spread has a 5-point strike width and receives a 1-point net credit, the simplified expiration maximum loss is 4 points before costs. The example only shows the expiration boundary; it does not model changes in implied volatility, bid-ask spread, early assignment risk, or mark-to-market value before expiration.

Breakeven depends on the side of the structure. In a put credit spread, breakeven is generally the short put strike minus the net credit. In a call credit spread, breakeven is generally the short call strike plus the net credit. These formulas describe simplified expiration math, not a guarantee of how the spread will trade before expiration.

Bull Put Credit Spread vs Bear Call Credit Spread

A bull put credit spread uses put options. It sells a higher-strike put and buys a lower-strike put on the same expiration, creating a net credit and a defined expiration boundary. The put-side credit structure shows how the same credit-spread logic is organized with put options.

A bear call credit spread uses call options. It sells a lower-strike call and buys a higher-strike call on the same expiration, also creating a net credit and a defined expiration boundary. The two variants differ by option type and price direction exposure, but both belong to the credit-spread family because the initial premium flow is positive.

| Variant | Option type | Basic structure | Classification role |

|---|---|---|---|

| Bull put credit spread | Puts | Sell higher-strike put, buy lower-strike put. | Put-side credit spread. |

| Bear call credit spread | Calls | Sell lower-strike call, buy higher-strike call. | Call-side credit spread. |

What the Payoff Chart Does Not Show

A payoff chart can make a credit spread look cleaner than the contract behavior may feel before expiration. The chart usually shows a simplified final payoff at expiration, while the quoted value of the spread can move before expiration as price, volatility, time, and liquidity conditions change.

Key limitation: the expiration payoff boundary is not the full risk model. A credit spread can lose value before expiration even when the final expiration outcome has not been reached, and the short leg can create assignment or exercise complications depending on the contract and market conditions.

Implied volatility can change the market value of both legs. Time decay can affect the short and long option differently as expiration approaches. The Greeks can also shift as the underlying price moves closer to or farther from the short strike.

Liquidity matters because bid-ask spreads can affect the practical value of entering, marking, or closing the spread. A narrow theoretical payoff boundary may still be difficult to realize if the options are thinly traded or the market is moving quickly.

Credit Spread vs Debit Spread

A credit spread starts with a net credit. A debit spread starts with a net debit because the purchased option costs more than the option sold. That premium-flow difference changes how the spread is usually described, but both structures still require attention to strike width, expiration, volatility, liquidity, and contract behavior.

Credit spreads and debit spreads should not be treated as simple opposites in every practical sense. A bull call spread structure, for example, is usually a debit-call spread rather than a credit spread, so its premium flow and payoff boundary are organized differently.

A bear put spread is another debit-spread contrast. It can help separate directional spread structure from the credit-spread category without shifting the main concept away from net credit mechanics.

Common Mistakes When Reading a Credit Spread

Treating the net credit as guaranteed income. The upfront credit is only the initial premium difference. The final result depends on price, expiration, contract behavior, costs, and market conditions outside the simplified payoff math.

Reading the payoff chart as the whole risk model. The chart usually shows expiration outcomes. It does not fully show before-expiration volatility changes, liquidity, changing Greeks, or assignment and exercise issues.

Confusing options credit spreads with bond credit spreads. Bond credit spreads describe credit-risk compensation in debt markets. Options credit spreads describe a multi-leg options structure with a net credit premium flow.

FAQ

What is a credit spread in options?

A credit spread in options is a spread where the option sold receives more premium than the option bought, creating a net credit. It usually uses the same underlying, same expiration, same option type, and different strike prices.

Is a credit spread the same as a debit spread?

No. A credit spread starts with net premium received, while a debit spread starts with net premium paid. Both can have defined expiration boundaries, but the premium flow and payoff logic are different.

Can a credit spread lose more than the credit received?

Yes. In simplified expiration terms, the potential loss is usually related to the strike width minus the net credit, before costs and practical complications. Assignment, exercise, liquidity, and contract-specific behavior still need separate review.

Why can a credit spread change value before expiration?

The spread’s market value can change because the underlying price moves, implied volatility changes, time decay affects each leg differently, and bid-ask spreads affect the quoted value.

Can the short leg of a credit spread be assigned?

Yes. The short option can create assignment or exercise risk depending on the option type, moneyness, expiration timing, and contract terms. A simplified payoff diagram does not remove that practical risk.