A bull call spread is a two-leg options spread that buys a lower-strike call and sells a higher-strike call on the same underlying and the same expiration. It creates a net debit position where simplified maximum loss is generally the debit paid, maximum profit is capped by the strike width minus that debit, and breakeven is the lower strike plus the net debit.

The structure is a defined payoff boundary, not a recommendation to open an options position. The formulas below describe simplified expiration outcomes before commissions, fees, bid-ask spreads, early closing decisions, exercise, assignment, and liquidity effects.

Definition: In options terminology, a bull call spread is a vertical call debit spread. The lower-strike long call creates upside exposure, while the higher-strike short call reduces the net debit and caps additional value above the upper strike.

Key Points

- A bull call spread uses two call options on the same underlying and expiration.

- The lower-strike call is bought and the higher-strike call is sold.

- The position is normally opened for a net debit.

- Simplified maximum loss generally equals the net debit paid, before costs and execution effects.

- Simplified maximum profit equals the strike width minus the net debit, before costs.

- Breakeven at expiration is the lower strike plus the net debit.

- The payoff is easiest to read at expiration; before expiration, time value and implied volatility can change the spread value.

How the Two Call Legs Create the Spread

The lower-strike long call gives the spread its upside participation. If the underlying rises above that lower strike, the long call can gain intrinsic value. The higher-strike short call offsets part of the cost, but it also gives away additional upside above the higher strike.

This is why the structure is different from a standalone long call. A long call keeps unlimited theoretical upside before costs, while a bull call spread exchanges part of that upside for a lower initial net debit and a defined upper payoff boundary.

| Leg | Role in the spread | Effect on payoff |

|---|---|---|

| Buy lower-strike call | Creates upside exposure above the lower strike | Adds value as the underlying rises past the lower strike |

| Sell higher-strike call | Reduces the net debit | Caps additional upside above the higher strike |

| Net debit | Initial simplified cost of the spread | Sets the simplified maximum loss boundary before costs |

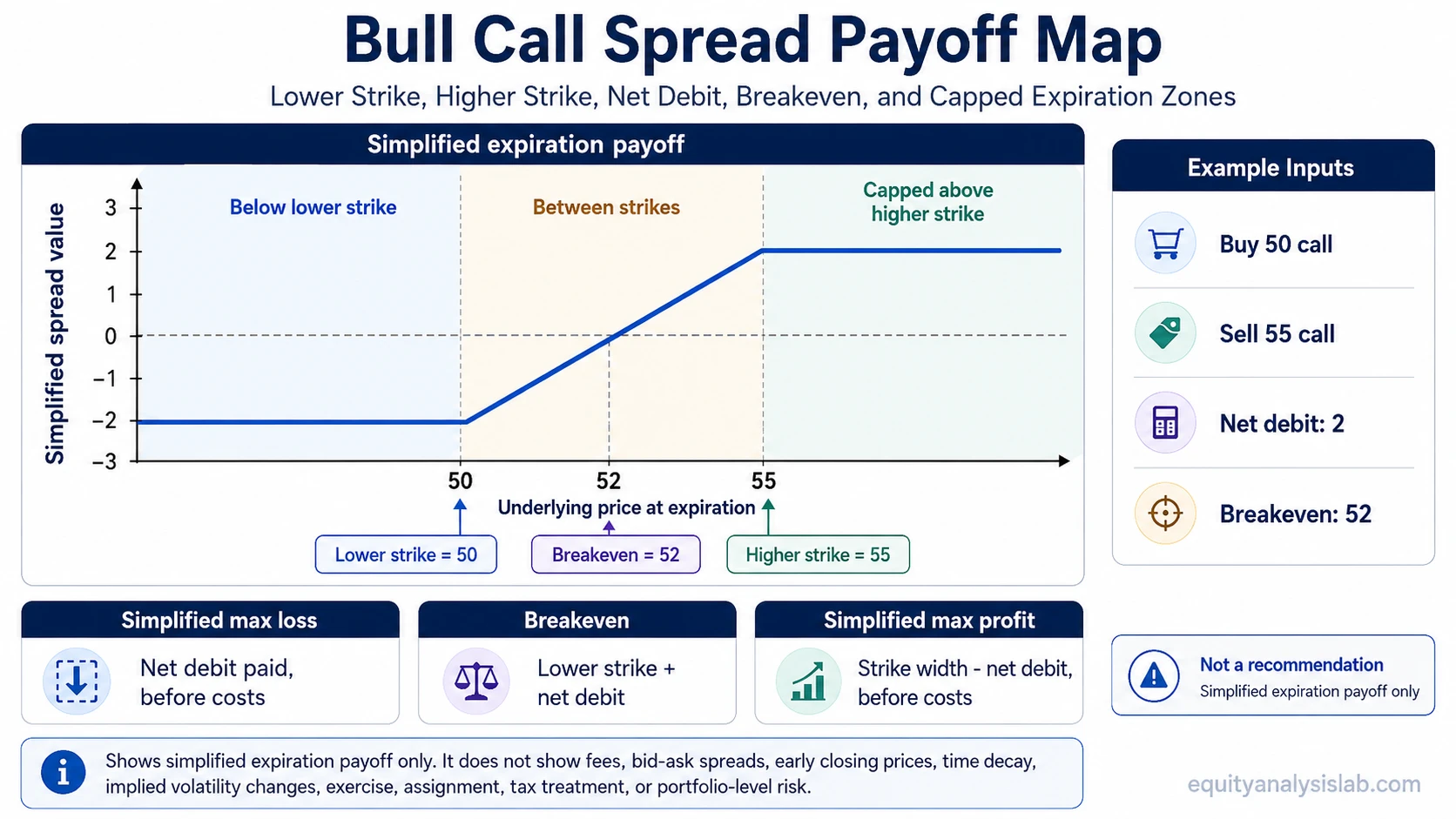

Bull Call Spread Payoff Zones at Expiration

The expiration payoff depends on where the underlying price finishes relative to the two strikes. The lower strike starts the spread’s intrinsic value, the higher strike caps that intrinsic value, and the net debit determines how much of the gross spread value remains as profit or loss.

| Underlying price at expiration | Long lower-strike call | Short higher-strike call | Simplified spread result |

|---|---|---|---|

| Below the lower strike | Expires out of the money | Expires out of the money | Spread value is generally zero; loss is generally the net debit paid, before costs. |

| Between the two strikes | Has intrinsic value | Usually expires out of the money | Spread value rises with the underlying, but the position may still be below or above breakeven depending on the debit. |

| Above the higher strike | Has intrinsic value | Offsets additional upside above the higher strike | Spread value is capped near the strike width; simplified maximum profit is strike width minus net debit, before costs. |

Maximum Profit, Maximum Loss, and Breakeven

The main formulas use the distance between the two strikes and the net debit paid for the spread. They are simplified expiration formulas and do not include commissions, fees, slippage, early closing prices, assignment effects, or changes in implied volatility before expiration.

| Measure | Simplified formula | What it means |

|---|---|---|

| Strike width | Higher strike – lower strike | The maximum intrinsic value the spread can have at expiration before subtracting the debit. |

| Maximum loss | Net debit paid | The simplified loss if both calls expire out of the money, before costs and execution effects. |

| Maximum profit | Strike width – net debit | The simplified capped profit if the underlying finishes at or above the higher strike, before costs. |

| Breakeven | Lower strike + net debit | The expiration price where the lower-strike call’s intrinsic value equals the debit paid. |

Formula note: These formulas describe a standard call debit spread at expiration. They do not describe whether the position is suitable, attractive, or correctly priced.

Example of a Bull Call Spread

Assume an underlying is analyzed using a lower strike of 50, a higher strike of 55, and a net debit of 2. The strike width is 5. The simplified maximum loss is 2, the simplified maximum profit is 3, and the breakeven is 52 before commissions and fees.

| Input or output | Value | Calculation |

|---|---|---|

| Lower strike | 50 | Long call strike |

| Higher strike | 55 | Short call strike |

| Net debit | 2 | Debit paid for the spread |

| Strike width | 5 | 55 – 50 |

| Simplified maximum loss | 2 | Net debit paid |

| Simplified maximum profit | 3 | 5 – 2 |

| Breakeven | 52 | 50 + 2 |

If the underlying finishes below 50 at expiration, both calls are generally out of the money and the simplified loss is the debit paid. If it finishes at 52, the lower-strike call has 2 of intrinsic value, matching the debit. If it finishes at or above 55, the spread’s intrinsic value is capped near 5, leaving 3 of simplified maximum profit before costs.

Why Upside Is Capped

The upside cap comes from the higher-strike short call. Once the underlying rises above that strike, gains on the lower-strike long call are increasingly offset by losses on the short call. The spread can still reach its simplified maximum profit, but it no longer participates in additional upside beyond the higher strike in the same way a standalone long call would.

This cap is not a flaw by itself; it is part of the structure. The tradeoff is that the short call reduces the debit paid, while also limiting the spread’s maximum expiration value.

Time Decay and Implied Volatility Before Expiration

Before expiration, a bull call spread does not move only according to the expiration payoff formula. Time value, implied volatility, the distance between the underlying price and each strike, and bid-ask spreads can all affect the market value of the spread.

Time decay can affect the long call and the short call differently depending on where the underlying is relative to the strikes. Implied volatility changes can also affect both legs, especially when expiration is not close. This is why the expiration payoff chart is a simplified map rather than a full valuation model.

Exercise, Assignment, Liquidity, and Fees

A bull call spread uses a short call, so assignment and exercise mechanics can matter. Early assignment risk is usually more relevant around dividends, hard-to-borrow situations, or when a short option is deep in the money, but exact risk depends on the contract, underlying, expiration, and account context.

Execution quality also matters. A theoretical debit may differ from the price available in the market because of bid-ask spreads and liquidity. Commissions, fees, and taxes can further change the realized result. The simplified payoff formulas should therefore be read as educational expiration mechanics, not as a complete position-management model.

Limitation: The spread defines a payoff boundary, but it does not remove all operational risk. Exercise timing, assignment, liquidity, and transaction costs can change the practical outcome.

Bull Call Spread vs Nearby Spread Structures

A bull call spread is one member of a broader group of option spread structures. It is bullish in the sense that its simplified expiration payoff improves as the underlying rises toward and above the higher strike, but it is still capped and debit-based.

| Structure | Basic construction | Primary difference |

|---|---|---|

| Bull call spread | Buy lower-strike call and sell higher-strike call | Debit-based bullish call spread with capped upside. |

| Bull put spread | Sell higher-strike put and buy lower-strike put | Credit-based bullish put spread with different assignment and premium mechanics. |

| Bear put spread | Buy higher-strike put and sell lower-strike put | Debit-based bearish put spread where value generally improves as the underlying declines toward the lower strike. |

| Butterfly spread | Combines multiple strikes around a middle strike | Uses a more centered payoff structure rather than a simple two-strike bullish boundary. |

What a Bull Call Spread Payoff Chart Does Not Show

A payoff chart is useful because it makes the lower strike, higher strike, debit, breakeven, maximum loss, and maximum profit visible in one structure. It is still incomplete. It usually shows simplified expiration values, not the changing market value of the spread during the life of the options.

The chart also does not answer whether the underlying, expiration, strikes, debit, volatility level, liquidity, or account constraints make sense for any specific investor. Those questions require separate analysis and should not be inferred from the payoff shape alone.

FAQ

What is a bull call spread?

A bull call spread is a two-leg call debit spread that buys a lower-strike call and sells a higher-strike call on the same underlying and expiration. The structure creates capped upside, a defined simplified loss boundary, and a breakeven based on the lower strike plus the net debit.

What is the maximum profit on a bull call spread?

The simplified maximum profit is the strike width minus the net debit paid, before commissions, fees, and execution effects. It is usually reached at expiration when the underlying finishes at or above the higher strike.

What is the maximum loss on a bull call spread?

The simplified maximum loss is generally the net debit paid, before commissions, fees, and execution effects. This occurs at expiration if both calls expire out of the money.

How do you calculate breakeven on a bull call spread?

The simplified breakeven at expiration is the lower strike plus the net debit paid. For example, with a 50 lower strike and a 2 net debit, the breakeven is 52 before costs.

Is a bull call spread the same as a long call?

No. A long call uses one call option and keeps theoretical upside uncapped before costs. A bull call spread sells a higher-strike call against the long call, which reduces the net debit but caps upside above the higher strike.