A long straddle is not profitable simply because the underlying moves. The move has to overcome the combined option premium by expiration, and before expiration the position package can gain or lose value as time, implied volatility, and option pricing change.

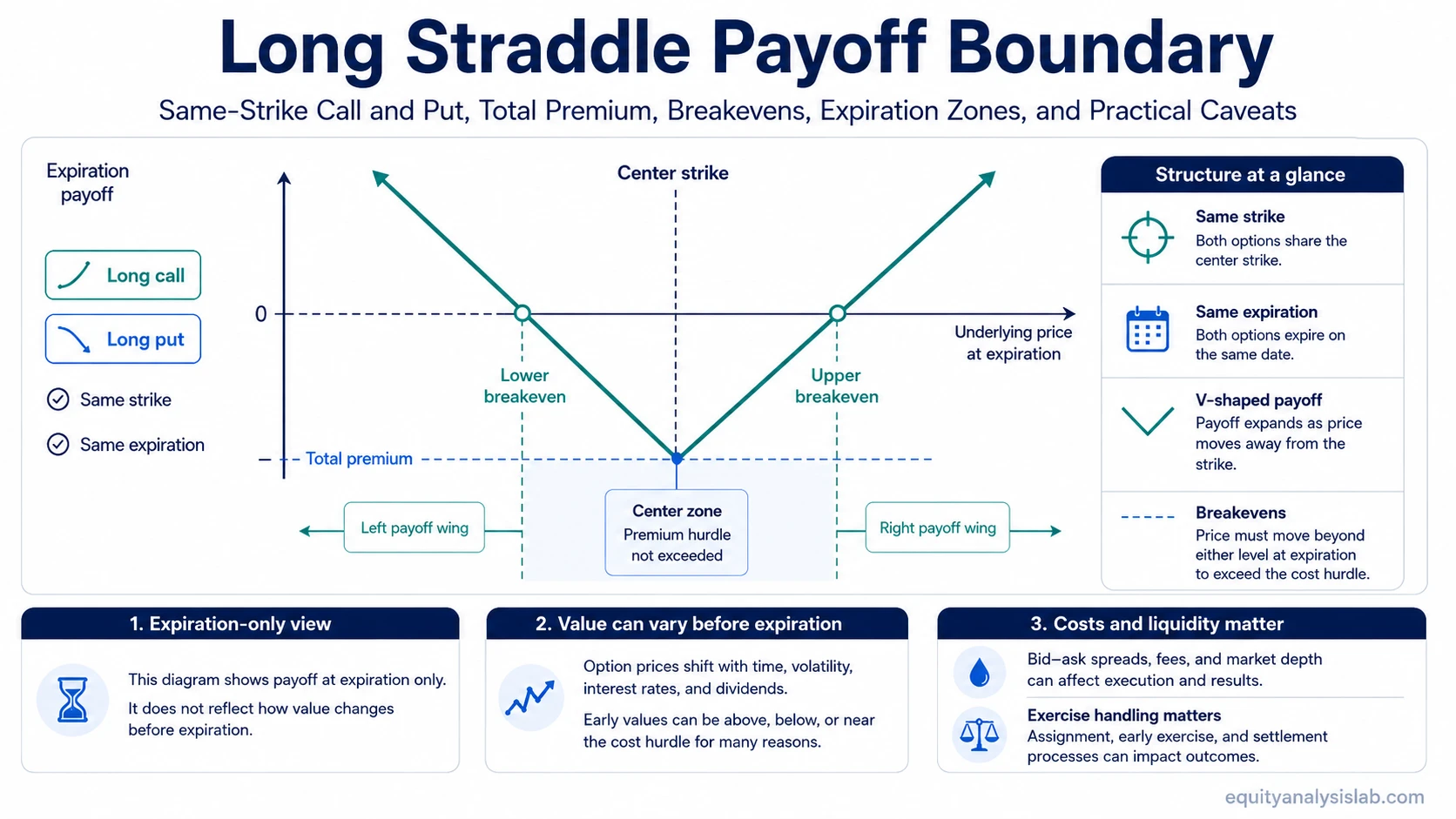

A long straddle combines a long call and a long put on the same underlying asset, with the same strike price and the same expiration date. The call benefits from upside movement, the put benefits from downside movement, and the total premium paid becomes the cost hurdle.

Definition: A long straddle is an options structure built by buying one call option and one put option with the same strike price and expiration. It has a net debit because both options are purchased.

Key Points

- A long straddle uses a long call and a long put at the same strike and expiration.

- The combined premium creates the breakeven hurdle.

- Maximum loss is generally limited to the total premium paid plus applicable costs if the underlying is near the strike at expiration.

- The upper breakeven is the strike plus total premium; the lower breakeven is the strike minus total premium.

- Before expiration, value can change because of time decay, implied volatility, liquidity, and option sensitivity.

- The concept defines payoff mechanics, not a decision rule.

What a Long Straddle Contains

The core anatomy is simple: one purchased call, one purchased put, one shared strike, and one shared expiration. The two options create exposure on both sides of the strike, but both legs cost premium. That cost is why a small move can still be insufficient.

| Component | Role in a Long Straddle |

|---|---|

| Long call | Creates upside exposure above the strike price. |

| Long put | Creates downside exposure below the strike price. |

| Same strike | Centers both options on one price level. |

| Same expiration | Makes the expiration payoff boundary easier to map. |

| Total premium | Defines the net debit, maximum loss boundary, and breakeven distance. |

The structure is different from a directional debit spread because both sides are purchased around the same strike. A bull call spread has a directional upside spread profile.

A bear put spread has a directional downside spread profile, so it does not create the same two-sided same-strike payoff shape.

Long Straddle Payoff and Breakevens

The expiration payoff depends on how far the underlying finishes from the strike compared with the total premium paid. If the underlying finishes close to the strike, both options may have little or no intrinsic value at expiration. If the underlying finishes far enough above or below the strike, one option can gain enough intrinsic value to offset the premium cost.

| Payoff Item | Formula or Boundary | Meaning |

|---|---|---|

| Total premium | Call premium + put premium | The net debit paid for the structure before commissions or fees. |

| Upper breakeven | Strike price + total premium | The upside expiration level where intrinsic value offsets the premium. |

| Lower breakeven | Strike price – total premium | The downside expiration level where intrinsic value offsets the premium. |

| Maximum loss boundary | Total premium paid, plus applicable costs | Generally occurs if the underlying finishes at or near the strike at expiration. |

| Upside boundary | Theoretically open-ended above the upper breakeven | The call can keep gaining intrinsic value as the underlying rises. |

| Downside boundary | Limited by the underlying not falling below zero | The put can gain intrinsic value as the underlying falls, but downside is not unlimited. |

Payoff diagram caveat: A standard long straddle payoff diagram usually shows the expiration boundary. It does not fully describe pre-expiration value, where time remaining, implied volatility, interest rates, dividends, liquidity, and option Greeks can change the mark-to-market value.

Simple Long Straddle Example

Consider a same-strike call and put with a 100 strike. The call costs 4, the put costs 3, and the total premium is 7 before commissions or fees. The lower breakeven is 93, calculated as 100 minus 7. The upper breakeven is 107, calculated as 100 plus 7.

| Expiration Zone | Expiration Payoff Boundary Before Costs Beyond Premium | Interpretation |

|---|---|---|

| Below 93 | The put has enough intrinsic value to exceed the total premium. | The downside move has passed the lower breakeven. |

| Between 93 and 107 | The structure has not exceeded the total premium hurdle by expiration. | The underlying moved, but not far enough to pass either expiration breakeven. |

| Above 107 | The call has enough intrinsic value to exceed the total premium. | The upside move has passed the upper breakeven. |

The example is only an expiration payoff illustration. Earlier valuation can be different if implied volatility rises or falls, time passes, or bid-ask spreads widen.

Why a Long Straddle Can Still Lose After a Move

Common misunderstanding: A long straddle does not only need movement. It needs enough movement relative to the premium paid, and the timing of that movement matters.

A move can be real but still too small to cover the combined premium by expiration. The market may also price an expected move into the options beforehand, making the premium hurdle larger. If the later realized move is smaller than the premium implied, the expiration payoff can remain unfavorable even though the underlying did not stay flat.

Implied volatility adds another layer before expiration. Rising implied volatility can increase option values, while falling implied volatility can reduce them. Around scheduled events, options can lose implied volatility after the event even when the underlying moves. The payoff formula is still useful, but the expiration diagram is only one view of the position package.

Risk boundary: Defined maximum loss does not mean low risk. The full debit can still be lost if the underlying finishes near the strike at expiration, and liquidity, spread width, commissions, fees, exercise decisions, automatic exercise, and expiration handling can affect practical outcomes.

Long Straddle vs Long Strangle

A long straddle uses the same strike for the call and put. A long strangle uses different strikes, usually one call strike above the current price and one put strike below it. That different-strike construction often changes the premium cost, breakeven distance, and payoff shape.

Core distinction: A long straddle centers both long options on one strike, while a different-strike volatility structure separates the call and put strikes.

| Feature | Long Straddle | Long Strangle |

|---|---|---|

| Strike setup | Same strike for call and put | Different call and put strikes |

| Premium profile | Often higher because both options are closer to the center strike | Often lower if both options are farther out of the money |

| Breakeven distance | Driven by one strike plus or minus total premium | Driven by each separate strike plus or minus total premium |

| Main confusion | Movement is needed, but premium still sets the hurdle | More movement may be needed because the strikes are separated |

Risks and Limitations Before Expiration

A long straddle has a clean expiration diagram, but option value before expiration is less static. Several variables can change valuation before either breakeven is reached.

| Variable | Why It Matters |

|---|---|

| Time decay | Both options are long premium positions, so time value can erode as expiration approaches. |

| Implied volatility | A fall in implied volatility can reduce option value even when the underlying moves. |

| Premium level | A high combined premium increases the distance to expiration breakeven levels. |

| Liquidity and spreads | Wide bid-ask spreads can affect transaction prices, liquidation value, and valuation marks. |

| Exercise and expiration handling | Long options can be exercised or automatically exercised under standard expiration procedures, and any resulting underlying position must be understood before expiration. |

| Costs | Commissions, fees, and contract multipliers can change the effective risk and breakeven calculation. |

A long straddle is best read as a defined-premium payoff package with two breakevens and moving pre-expiration value drivers. It does not remove the need to understand price path, option pricing, liquidity, and expiration mechanics.

FAQ

What is a long straddle in options?

A long straddle is an options structure made by buying one call and one put on the same underlying asset, with the same strike price and expiration date.

How do you calculate long straddle breakevens?

The upper breakeven is the strike price plus the total premium paid. The lower breakeven is the strike price minus the total premium paid.

What is the maximum loss on a long straddle?

The maximum loss is generally the total premium paid plus applicable costs, usually if the underlying finishes at or near the strike price at expiration.

Why can a long straddle lose money even if the underlying moves?

The move may be too small to overcome the combined premium, or pre-expiration value may be affected by time decay, implied volatility changes, liquidity, and option pricing.