A concentrated stock portfolio construction framework helps organize intentional concentration before it turns into unmanaged exposure. The framework does not decide which stocks to own. It separates portfolio role, exposure weight, overlap, drawdown tolerance, and review discipline so the investor can understand how concentration changes risk and return.

A concentrated stock portfolio can be deliberate or accidental. It is deliberate when the investor understands why a small number of holdings, a large single position, or a top-weight cluster exists. It is accidental when the portfolio looks diversified by holding count but still depends on one company, one sector, one factor, one economic driver, or one thesis.

Key Points

- A concentrated stock portfolio is not automatically weak or automatically superior. Its quality depends on exposure design, thesis clarity, risk capacity, and review discipline.

- Holding count alone can be misleading. A portfolio with many holdings can still be concentrated if the positions share the same business driver, sector, factor, or economic sensitivity.

- Position weight matters because a large holding can dominate portfolio behavior even when the investor owns several smaller positions around it.

- Drawdown tolerance is part of the framework. Concentrated portfolios can be harder to hold through company-specific volatility, earnings surprises, valuation compression, or business-model disappointment.

- Review rules matter more than a fixed calendar. The framework should define what changes the original thesis, what changes exposure risk, and what requires reassessment.

What a Concentrated Stock Portfolio Framework Does

Framework definition: A concentrated stock portfolio construction framework is a process for deciding whether concentrated exposure is intentional, understandable, tolerable, and reviewable. It organizes the portfolio around role, weight, overlap, drawdown capacity, and monitoring rules instead of using a universal number of holdings as the only test.

The framework should not treat a concentrated position as automatically wrong. Concentration can reflect conviction, a specialized research process, a founder or employer holding, a legacy position, or a deliberate decision to hold fewer companies. The risk appears when the investor cannot explain what the position is supposed to do, how much portfolio behavior it controls, or which conditions would weaken the reason for keeping that exposure.

The useful question is not only “How many stocks are in the portfolio?” A better question is “What actually drives the portfolio if the largest positions move together?” That shift keeps the analysis focused on construction logic instead of turning concentration into a generic diversification question or a private-bank solution menu.

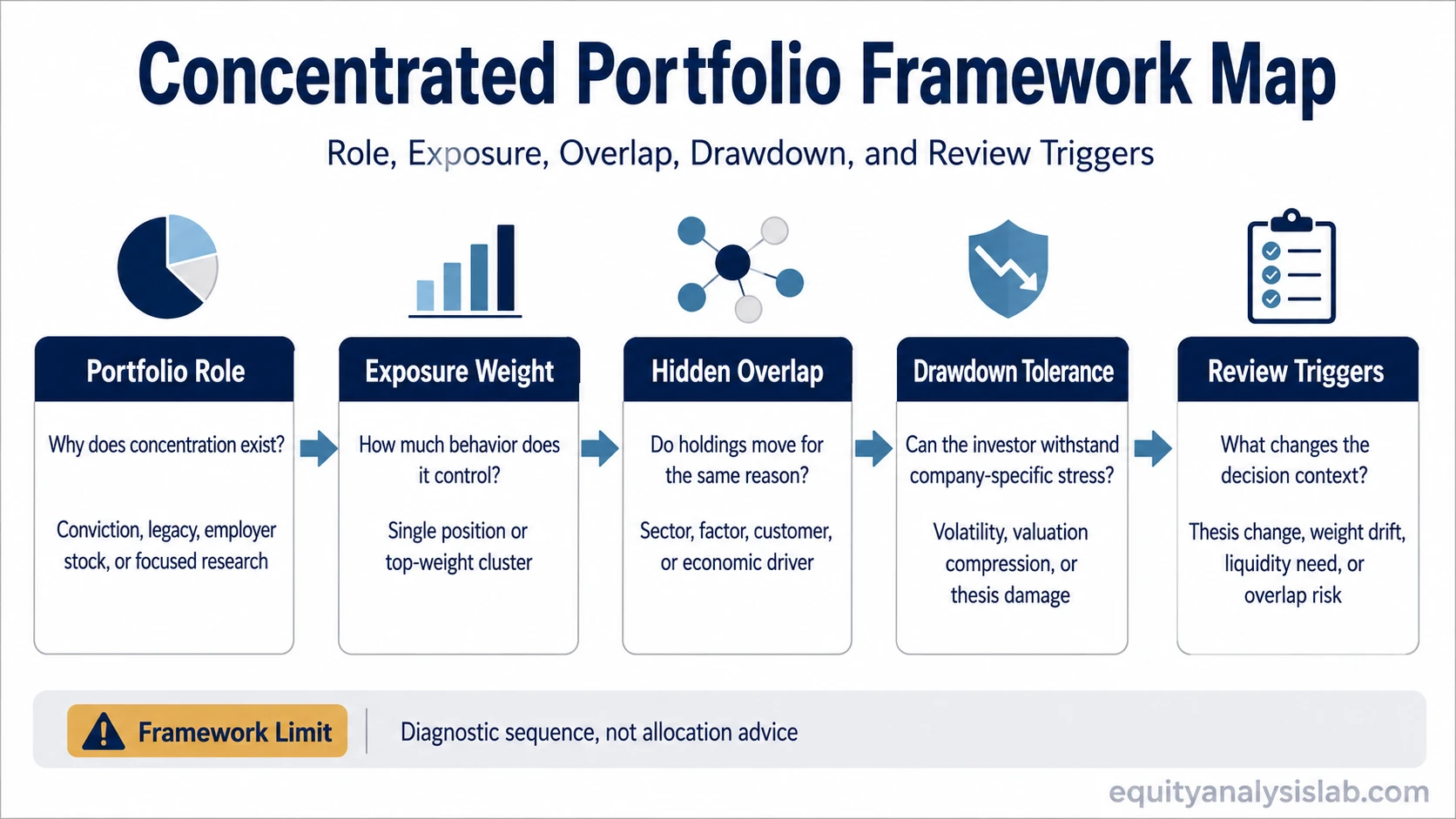

The Framework Sequence

A concentrated portfolio becomes easier to evaluate when the construction sequence starts with role and ends with review discipline. The sequence below is not an allocation model. It is a diagnostic order for understanding whether concentration is intentional and controlled.

| Step | Framework question | What the answer should clarify |

|---|---|---|

| 1. Portfolio role | Why does this concentrated exposure exist? | Whether the portfolio is built around conviction, legacy exposure, income needs, employer stock, tax constraints, or a focused research process. |

| 2. Concentration exposure | Which holdings control the largest share of portfolio behavior? | The largest position weight, top-five weight, top-ten weight, and whether one company dominates outcomes. |

| 3. Overlap map | Do the holdings depend on the same drivers? | Sector overlap, factor exposure, business-model similarity, geographic concentration, customer overlap, or common economic sensitivity. |

| 4. Position weight logic | Is each position weight consistent with its role and uncertainty? | Whether the largest holdings reflect research depth, risk capacity, liquidity needs, and thesis durability rather than drift or neglect. |

| 5. Drawdown tolerance | Could the investor stay rational if the largest exposures declined sharply? | Whether company-specific volatility, valuation compression, or business disappointment would force an unplanned decision. |

| 6. Review discipline | What would trigger a reassessment? | The thesis, weight, overlap, liquidity need, risk capacity, or portfolio role that would require review. |

Observable Checklist for Concentrated Portfolio Construction

The checklist should focus on observable inputs rather than product solutions. It helps identify whether the portfolio is intentionally focused or unintentionally dependent on a narrow risk source.

| Input to check | Why it matters | Common weak spot |

|---|---|---|

| Number of holdings | Shows the visible portfolio structure. | Assuming more holdings always mean better diversification. |

| Largest position weight | Shows how much one company can influence total portfolio behavior. | Letting a winner become dominant without a fresh role review. |

| Top-five or top-ten weight | Shows whether the portfolio is driven by a small cluster. | Ignoring that several large holdings may rise and fall together. |

| Sector and industry exposure | Shows whether the portfolio depends on one part of the market. | Counting different tickers as separate risks when they share the same cycle. |

| Business-driver overlap | Shows whether revenue, margins, valuation, or demand depend on similar forces. | Missing hidden overlap across companies that appear unrelated by name. |

| Time horizon | Shows whether the investor can wait through volatility and thesis development. | Holding concentrated exposure with a time horizon too short for the thesis. |

| Liquidity needs | Shows whether the portfolio may need cash before the thesis has time to work. | Confusing long-term conviction with near-term liquidity flexibility. |

| Drawdown tolerance | Shows whether the investor can tolerate company-specific and cluster-level declines. | Underestimating how hard concentrated drawdowns are to hold through. |

| Review trigger | Shows what would cause a reassessment before emotion takes over. | Reviewing only after a large price move instead of after a thesis change. |

False Diversification and Hidden Overlap

A portfolio can look diversified while still behaving like a concentrated portfolio. A common scenario is a portfolio with 12 holdings where the investor owns companies across different ticker symbols, but roughly 60% of the portfolio depends on the same sector, the same demand cycle, or the same valuation factor. The holding count looks broad. The underlying driver is narrow.

This is where spread across holdings needs to be tested by exposure, not only by the number of companies. If several positions depend on the same interest-rate environment, commodity cycle, advertising market, consumer spending trend, or software spending cycle, the portfolio may react as one cluster during stress.

Scenario logic: An investor owns 12 stocks. No single holding looks extreme at first glance, but five of the largest positions depend on similar growth expectations and similar valuation multiples. If those expectations reset at the same time, the portfolio may experience concentrated drawdown even though it does not look concentrated by ticker count alone.

The purpose of the overlap map is not to eliminate every shared driver. Some overlap may be intentional. The practical issue is whether the investor can identify the shared driver before it becomes the source of an unexpected portfolio shock.

How Position Weight and Drawdown Tolerance Interact

Position weight is the bridge between thesis quality and portfolio risk. A strong company thesis can still create a fragile portfolio if the position becomes too large for the investor’s financial needs, emotional tolerance, or review process. A weaker thesis can create even more risk if it receives a large weight because of price drift rather than deliberate construction.

The framework should connect how much portfolio weight each holding carries with the uncertainty around the thesis. A position with durable cash flow, clear balance-sheet strength, and a long review horizon may be easier to justify than a position whose value depends on a narrow forecast, a single product cycle, or a fragile valuation multiple. That does not make the larger position safe. It only clarifies which assumptions support the exposure.

Drawdown tolerance should be assessed before stress arrives. Concentrated portfolios often feel manageable when the largest holdings are rising. The test is whether the investor has already defined what would count as normal volatility, what would count as thesis damage, and what would count as portfolio-level exposure becoming too dominant.

Review and Rebalancing Discipline

Review discipline is not the same as prescribing a fixed rebalancing cadence. A concentrated stock portfolio may need review when the exposure changes, when the thesis changes, when the investor’s liquidity needs change, or when hidden overlap becomes more important than expected.

A useful review rule identifies the condition that matters. For example, a review may be triggered if the largest position crosses a portfolio-weight boundary set by the investor’s own policy, if the original business thesis weakens, if several holdings become more correlated than expected, or if a personal liquidity need shortens the time horizon. The rule is about disciplined reassessment, not automatic action.

This separates construction review from tax planning, hedging, covered-call strategies, exchange funds, or advisor-specific implementation. Those may be relevant in some real situations, but they are not the core role of this framework.

When the Framework Weakens

The framework weakens when the investor cannot define the portfolio role of the concentrated exposure. If the holding exists only because it has gone up, was inherited, came from employer stock, or has become emotionally difficult to reduce, the portfolio may be concentrated without a clear construction reason.

The framework weakens when position weights are undefined. Without a weight policy or review boundary, concentration can grow silently until one holding or one cluster controls portfolio behavior.

The framework weakens when overlap is not mapped. Different stocks can still depend on the same economic, sector, factor, or valuation driver.

The framework weakens when drawdown capacity is assumed but not tested. Concentrated exposure can create company-specific losses that feel very different from broad market volatility.

The framework weakens when review triggers are vague. If the investor does not know what would change the thesis, the position role, or the acceptable exposure, decisions may become reactive after volatility has already arrived.

Where to Go Deeper

After the framework is clear, the next step is to separate the component concepts. Concentration explains the exposure itself. Risk and return explains the trade-off. Diversification explains whether exposure is actually spread. Position sizing explains how portfolio weights turn a thesis into portfolio impact.

- Use concentration to understand what concentrated exposure means before applying the framework.

- Use risk and return to frame why higher concentration can change both upside participation and downside exposure.

- Use diversification to evaluate whether holdings actually spread exposure or merely add more ticker symbols.

- Use position sizing to understand how portfolio weights translate a thesis into portfolio impact.

FAQ

What is a concentrated stock portfolio?

A concentrated stock portfolio is a portfolio where a small number of stocks, one large position, or a narrow group of related holdings drives a meaningful share of total portfolio behavior. The concentration may be intentional or accidental.

Is a concentrated stock portfolio always risky?

It always changes the risk profile, but the quality of that risk depends on position weights, business-driver overlap, drawdown capacity, time horizon, and the investor’s ability to review the thesis without reacting emotionally to volatility.

Can a portfolio with many stocks still be concentrated?

Yes. A portfolio can hold many stocks and still be concentrated if the largest holdings depend on the same sector, factor, business model, geography, customer base, or economic condition.

Does this framework give a maximum position size?

No. The framework does not give a universal maximum position size or personal allocation rule. It helps identify the inputs an investor would need to evaluate before deciding whether concentrated exposure is intentional and tolerable.