Diversifying a stock portfolio means building exposure so that no single holding, sector, style, geography, or shared business driver controls the portfolio outcome. A portfolio can hold many stocks and still have weak diversification if the positions behave like one large bet.

A useful review looks beyond ticker count and checks whether weights, overlap, concentration, rebalancing rules, and review capacity work together.

Key Points

- Stock count is only the starting point. Exposure depends on position weights and shared drivers.

- Top-heavy portfolios can remain concentrated even when they contain many holdings.

- Sector, geography, style, factor, ETF, and business-model overlap can make separate holdings behave similarly.

- Rebalancing matters because portfolio weights drift as prices move.

- A portfolio is harder to diversify when it contains more positions than the investor can review with discipline.

What Diversification Means in a Stock Portfolio

In a stock portfolio, diversification is the design of exposure across companies, industries, business drivers, regions, and risk sources. It does not mean owning a random list of stocks. It means reducing the chance that one narrow source of risk dominates the whole portfolio.

A simple stock list can look diversified while still depending on the same earnings cycle, interest-rate sensitivity, commodity price, consumer trend, currency exposure, or technology theme. The goal is to understand what the holdings depend on, not only how many names are included.

Start With Portfolio Role and Asset Allocation Boundary

Before judging individual stocks, define the role of the stock portfolio inside the wider investment plan. A stock sleeve has a different job when it is the growth engine of a balanced portfolio than when it is only one part of a larger mix of cash, bonds, funds, or other assets.

This boundary is where asset allocation matters. It sets the broader exposure before individual stock selection begins. Without that boundary, a stock portfolio can become too aggressive or too narrow even when the individual holdings look reasonable on their own.

Check Position Weights Before Counting Holdings

Position weights show how much each holding can affect the portfolio. A 25-stock portfolio where the top three names represent half of the total value is not diversified in the same way as a 25-stock portfolio where exposure is more evenly distributed.

Good diversification starts with weighting discipline. The size of each position should reflect conviction, risk, uncertainty, and the investor’s ability to monitor the business. This is where position weight decisions become part of the diversification process, not a separate afterthought.

Find Concentration and Shared Exposure

Portfolio concentration can appear in more than one way. A portfolio may be concentrated because one holding is too large, but it may also be concentrated because many holdings depend on the same driver.

Shared exposure often hides behind different ticker symbols. Several companies may all depend on the same sector cycle, same input cost, same interest-rate environment, same customer group, same region, or same valuation factor. ETFs and individual stocks can also overlap if the fund already owns many of the same companies.

Use a Diversification Checklist

A diversification review should separate visible holdings from underlying exposure.

| Checklist item | What to check | Why it matters |

|---|---|---|

| Holding count | Number of individual stocks, funds, or ETFs | Shows breadth, but does not prove diversified exposure by itself. |

| Position weights | Largest holdings and top-5 or top-10 share of the portfolio | Shows whether a few positions dominate portfolio movement. |

| Sector exposure | Revenue and earnings dependence by industry group | Reduces the risk of one sector cycle controlling results. |

| Business drivers | Common dependence on rates, commodities, consumer spending, regulation, or technology demand | Finds hidden overlap that ticker count can miss. |

| Style and factor exposure | Growth, value, quality, small-cap, large-cap, momentum, or dividend tilt | Shows whether the portfolio is mainly one market style in disguise. |

| Geography and currency | Country exposure, revenue exposure, and currency sensitivity | Helps identify regional or currency concentration. |

| Fund and stock overlap | Stocks held directly and also inside ETFs or funds | Prevents accidental double exposure to the same companies. |

| Rebalancing rule | When and why weights are reviewed or trimmed back to range | Prevents successful positions from quietly becoming unintended bets. |

| Review capacity | Number of businesses the investor can actually follow | Prevents false comfort from owning more positions than can be monitored. |

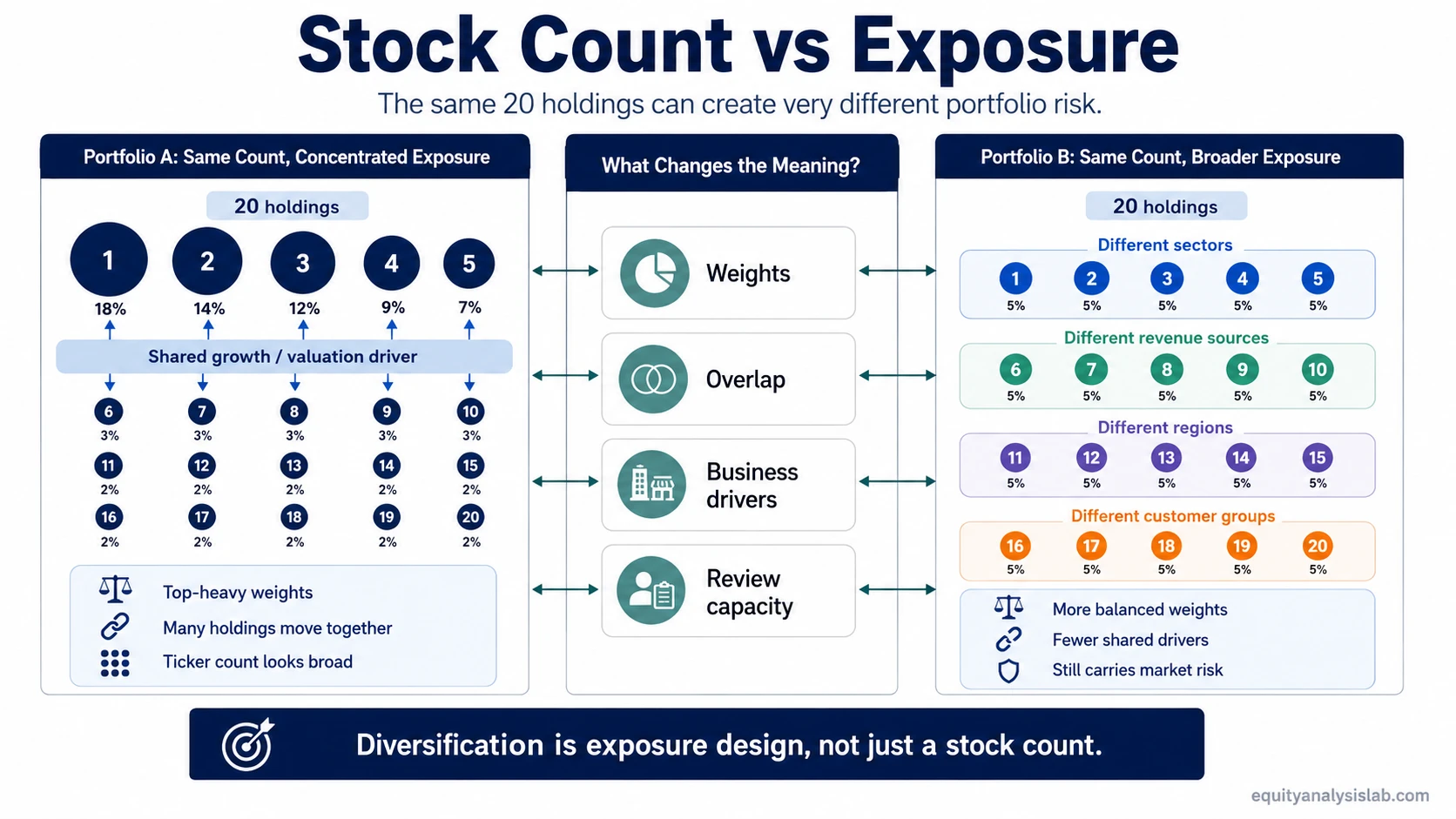

Why Stock Count Can Create False Diversification

Two portfolios can each hold 20 stocks and still carry very different risk.

Portfolio A has 20 holdings, but the top five positions make up most of the value. Many of the smaller positions are also technology-related businesses that depend on the same growth expectations and valuation environment. The account looks broad by ticker count, but the real exposure is top-heavy and driver-heavy.

Portfolio B also has 20 holdings, but position sizes are more balanced. The businesses depend on different revenue sources, sectors, regions, customer groups, and economic drivers. The account still carries stock-market risk, but fewer outcomes depend on one narrow exposure.

The difference is not the number 20. The difference is how the holdings behave together when conditions change.

Maintain Diversification With Rebalancing and Review Capacity

Diversification changes after the portfolio is built. Winners grow, laggards shrink, new information appears, and correlations can rise during market stress. A portfolio that started with balanced exposure can become concentrated if weights are never reviewed.

Rebalancing does not have to mean constant trading. It means having a rule for when drift becomes large enough to review. That rule can be based on position size, sector weight, risk budget, tax considerations, or the investor’s written process.

Review capacity is part of the same discipline. A portfolio with too many individual companies can become difficult to follow. When the investor cannot track earnings quality, balance-sheet risk, business-model changes, or valuation context across all holdings, the portfolio may become diversified on paper but weak in practice.

When Diversification Breaks Down

Diversification is a risk-control framework, not a guarantee against loss. It can weaken under several conditions:

- Top positions grow so large that they dominate portfolio movement.

- Different holdings depend on the same sector, factor, geography, or business driver.

- ETF holdings overlap with individual stocks already owned directly.

- Rebalancing rules are unclear, ignored, or applied only after large drift has already occurred.

- The portfolio contains more businesses than the investor can review properly.

- Market-wide stress causes correlations to rise across stocks that usually behave differently.

- Liquidity needs force selling at the wrong time, even if the long-term portfolio design looks reasonable.

The goal is not to avoid every decline. The goal is to avoid unnecessary dependence on one narrow outcome.