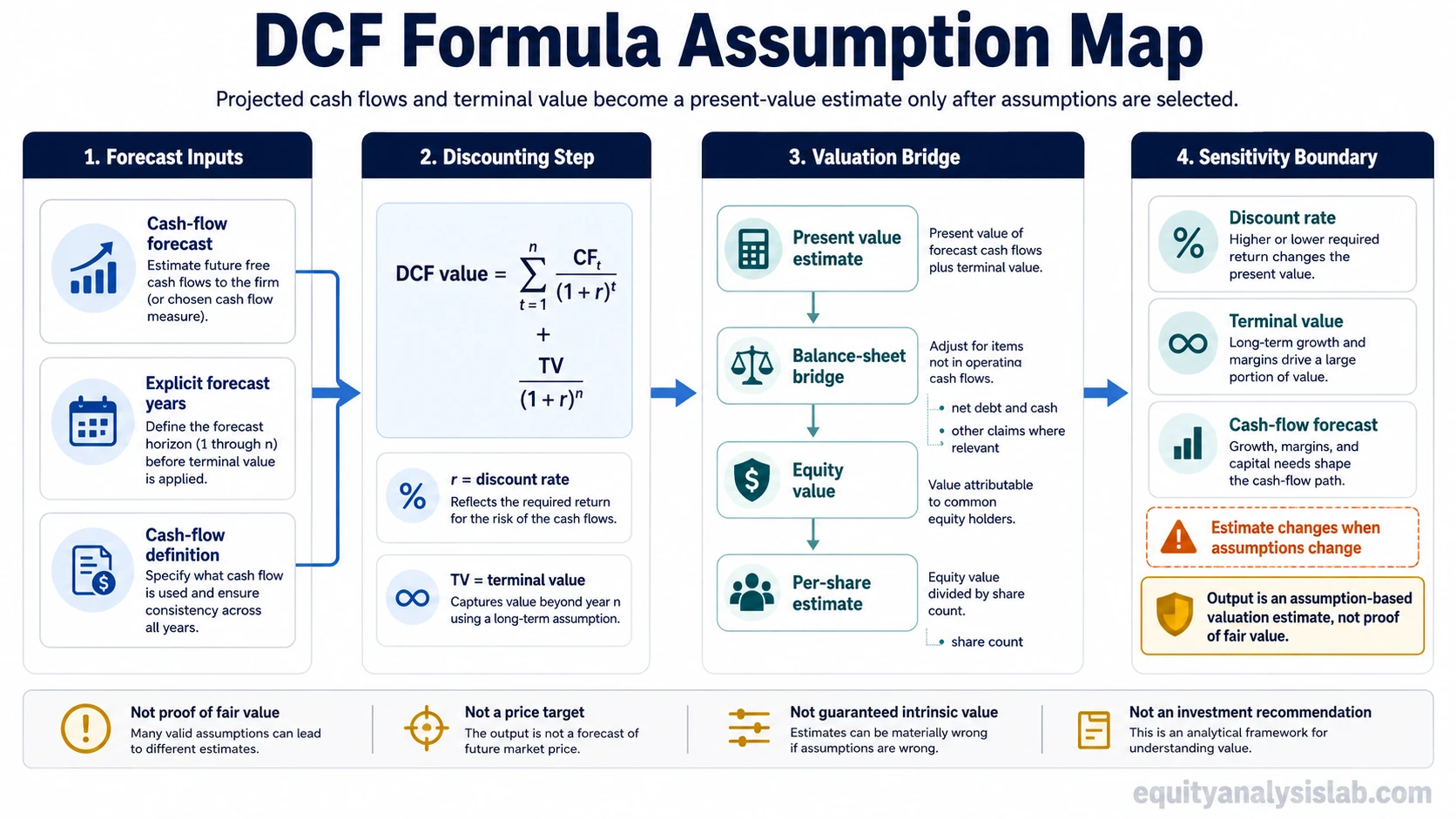

The DCF formula converts projected future cash flows and terminal value into a present-value estimate using a discount rate. The formula can produce a clean number, but that number is only as useful as the assumptions behind it.

DCF formula: estimated value equals the present value of projected cash flows plus the present value of terminal value.

Basic notation: DCF value = Σ CFt / (1 + r)t + TV / (1 + r)n

In the formula, CFt is the projected cash flow in each period, r is the discount rate, t is the period number, TV is terminal value, and n is the final forecast period. The formula translates selected cash-flow and return assumptions into a present-value estimate.

Key points about the DCF formula

- The formula discounts projected cash flows back to present value.

- The discount rate controls how heavily future cash flows are reduced for risk and time.

- Terminal value can carry a large share of the output, especially when the explicit forecast period is short.

- Net debt, cash, and share count can change the bridge from enterprise value to equity value per share.

- A precise formula output is still an estimate, not a final investment conclusion.

What the DCF formula calculates

The DCF formula calculates the present value of future cash flows. It starts with projected cash flows, discounts each period back to today, adds a discounted terminal value, and then applies any required bridge from enterprise value to equity value.

A DCF result is only as useful as the cash-flow assumptions behind it. Strong formatting, detailed decimals, or a long forecast model cannot fix weak cash-flow estimates, a mismatched discount rate, or an unsupported terminal value assumption.

DCF formula components

The formula has four core moving parts. Each part controls a different source of valuation sensitivity.

| Formula component | What it means | Why it changes the result |

|---|---|---|

| CFt | Projected cash flow in each forecast period | Higher or lower cash-flow estimates directly change the present-value base. |

| r | Discount rate | A higher rate reduces the present value of future cash flows; a lower rate increases it. |

| t or n | Forecast period number | Cash flows further in the future are discounted more heavily. |

| TV | Terminal value | The value assigned after the explicit forecast period can dominate the final estimate. |

How each DCF input changes the valuation estimate

The most useful way to read a DCF formula is as an assumption stack. Each input answers a different question, and each weak input can make the final estimate less reliable.

| Input | What it controls | Common mistake | Deeper concept |

|---|---|---|---|

| Cash-flow forecast | The base value being discounted | Forecasting growth from narrative strength instead of cash generation quality | Free cash flow quality and forecast durability |

| Discount rate | The required return used to discount future cash flows | Using a rate that does not match the risk, cash-flow type, or valuation basis | Required return, WACC, and cost of equity selection |

| Terminal value | The value assigned beyond the explicit forecast period | Letting most of the valuation depend on an unsupported long-term assumption | Perpetuity growth and exit multiple assumptions |

| Balance sheet bridge | The move from enterprise value to equity value | Ignoring net debt, excess cash, minority interest, or other bridge items | Enterprise value versus equity value |

| Share count | The per-share translation of total equity value | Using basic shares when dilution or buybacks may change ownership claims | Diluted shares, dilution, and buyback effects |

The formula can look objective because the math is structured. The sensitivity comes from the assumptions chosen before the math begins.

Why the DCF formula can look precise but still be fragile

A DCF estimate can change sharply when a small number of assumptions move. The discount rate affects every future cash flow. Terminal value can represent a large part of the total. Cash-flow forecasts can be too optimistic if margins, reinvestment needs, working capital, or competitive pressure are underestimated.

Misuse boundary: the DCF formula is a valuation translation tool, not proof of intrinsic value. It can support analysis, but it does not create a guaranteed return, a price target, or a buy/sell decision by itself.

| Fragility point | What can go wrong | Safer interpretation |

|---|---|---|

| Cash-flow forecast | Projected cash flow assumes a business quality that the company may not deliver. | Treat forecast cash flow as a scenario, not a fact. |

| Discount rate | The rate is too low for the risk profile or does not match the cash-flow definition. | Check whether the rate matches FCFF, FCFE, WACC, or cost of equity logic. |

| Terminal value | The final estimate depends more on the terminal assumption than on the explicit forecast. | Separate the value created during the forecast from the value implied after it. |

| Balance sheet bridge | Enterprise value is confused with equity value. | Adjust for net debt, cash, and other bridge items before reading equity value. |

| Share count | The per-share value ignores dilution or future share-count changes. | Use the share base that matches the ownership claim being valued. |

DCF formula example with hypothetical numbers

Assume a company is expected to generate 100, 110, and 120 in annual cash flow over three forecast years. Assume a terminal value of 1,400 at the end of year three and a 10% discount rate.

Illustrative calculation:

- Year 1 present value: 100 / 1.10 = 90.9

- Year 2 present value: 110 / 1.102 = 90.9

- Year 3 present value: 120 / 1.103 = 90.2

- Terminal value present value: 1,400 / 1.103 = 1,051.8

- Estimated DCF value before balance-sheet adjustments: 1,323.8

The example is deliberately simple. The formula does not decide which assumption is correct. It reveals how much the estimate depends on those assumptions.

| Same cash-flow assumptions | Discount rate | Estimated value before balance-sheet adjustments |

|---|---|---|

| 100, 110, 120, and terminal value of 1,400 | 10% | 1,323.8 |

| 100, 110, 120, and terminal value of 1,400 | 11% | 1,290.8 |

In this simplified case, a one-percentage-point increase in the discount rate lowers the estimate by about 33.0 before any balance-sheet bridge or share-count adjustment. A lower terminal value would create a separate change in the output.

DCF formula vs the full discounted cash flow method

The formula is only one part of discounted cash flow analysis. The full method includes cash-flow definition, forecast structure, reinvestment assumptions, discount-rate selection, terminal-value method, balance-sheet adjustments, and per-share interpretation.

The formula answers a narrower question: what present-value estimate follows from this specific set of assumptions? The broader valuation work asks whether those assumptions are reasonable for the business being analyzed.

DCF formula limitations and common mistakes

- Treating the output as true value: a DCF result is an estimate built from assumptions, not a verified market truth.

- Mismatching cash flows and discount rates: FCFF usually needs an enterprise-value discounting framework, while FCFE usually needs an equity-value framework.

- Ignoring terminal-value dominance: a model can appear detailed while most of the output comes from one terminal assumption.

- Skipping the balance-sheet bridge: enterprise value and equity value are not the same when debt, cash, and other claims matter.

- Ignoring share count: per-share value depends on the ownership base used in the calculation.

Related valuation methods

DCF estimates value from projected cash flows and a required return. Comparable company analysis uses market multiples from peer companies to frame relative valuation.

The dividend discount model values equity from expected dividends rather than broader free cash flow.

Use the method that matches the question: DCF is most useful when cash-flow assumptions can be estimated with enough discipline. Relative valuation is often better for market-implied comparisons. Dividend discounting is narrower and works best when dividends are central to the equity story.

FAQ

What is the biggest risk in using the DCF formula?

The biggest risk is treating the formula output as more reliable than the assumptions behind it. Cash-flow forecasts, discount rate, terminal value, balance-sheet adjustments, and share count can all change the estimate.

Why does the discount rate matter in a DCF formula?

The discount rate determines how much future cash flows are reduced for time and risk. A higher discount rate lowers the present value of future cash flows, while a lower discount rate raises it.

Can the DCF formula prove fair value?

No. The formula converts assumptions into an estimate. It does not prove fair value or replace judgment about cash-flow quality, risk, terminal value, balance-sheet adjustments, and share count.