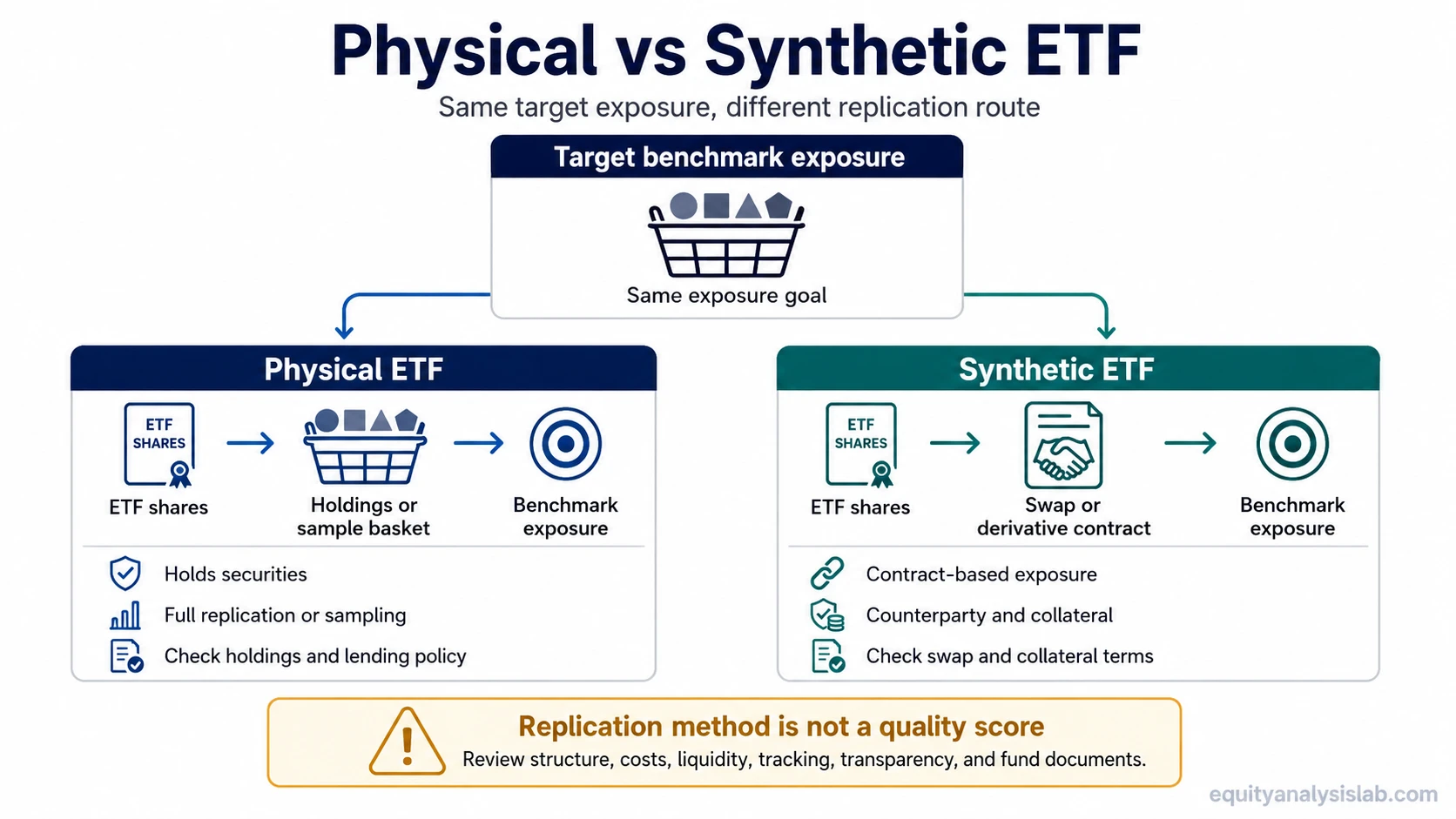

A physical ETF gets market exposure by holding the underlying securities directly or by holding a representative sample. A synthetic ETF gets similar economic exposure through swap or derivative contracts. The difference is the replication route, not an automatic quality score.

That distinction matters because two ETFs can target the same benchmark while giving investors different things to check. One fund may show a list of owned shares and sampling choices. Another may show swap counterparties, collateral rules, and derivative exposure. The better question is not “which label is better?” but “what structure does this fund actually use, and what risks or trade-offs come with it?”

Key Points

- A physical ETF usually owns the index securities directly, either through full replication or representative sampling.

- A synthetic ETF uses swap or derivative economics to receive the return of the target exposure.

- Physical replication can still involve sampling, securities lending, and tracking gaps, so it is not automatically risk-free.

- Synthetic replication adds counterparty and collateral questions, but it is not automatically inferior.

- Fund documents should show whether the exposure is holdings-based, swap-based, or mixed before cost, liquidity, and tracking comparisons are made.

Physical vs synthetic ETF: the core difference

The core difference between a physical and synthetic ETF is how the fund delivers exposure. Physical replication is holdings-based. Synthetic replication is contract-based.

Simple distinction: A physical ETF tries to track its benchmark by owning the assets, while a synthetic ETF tries to track its benchmark by using a swap or derivative contract that delivers the benchmark return.

The investor still owns shares of the ETF. What changes is the mechanism inside the fund. In a physical structure, the fund’s exposure mainly comes from the securities it holds. In a synthetic structure, the exposure depends on the swap arrangement, collateral framework, and counterparty setup described in the fund documents.

This distinction sits inside the broader ETF structure. It does not replace checks on cost, index methodology, liquidity, distribution policy, or investor suitability.

How physical ETF replication works

A physical ETF normally holds the securities in the index it aims to track. A fund tracking a broad equity index may own the index constituents directly, or it may hold a representative sample if full replication would be costly, difficult, or inefficient.

Full replication means the fund attempts to hold each benchmark constituent in roughly the same weight as the index. Sampling means the fund holds a subset designed to behave like the index. Sampling can reduce operational complexity, but it also makes the tracking result dependent on how well the sample mirrors the benchmark.

Physical replication is often easier to understand because the holdings list can show what the fund owns. That does not mean every physical ETF is simple. A physical ETF may use sampling, may lend securities, may hold cash or derivatives for portfolio management, and may still show a difference between the index return and the fund return.

Physical does not mean perfect replication. The holdings list, sampling method, securities lending policy, expense ratio, and historical tracking record still matter.

How synthetic ETF replication works

A synthetic ETF uses a swap or derivative contract to receive the return of the target index or exposure. Instead of relying mainly on owned constituents to match the benchmark, the fund receives benchmark economics through a contractual arrangement with one or more counterparties.

The fund may also hold a collateral basket or substitute basket. That basket may not look identical to the target index, because its role is tied to the swap and collateral framework rather than simple direct ownership of every benchmark constituent.

The main synthetic ETF questions are different from the main physical ETF questions. Investors need to understand who the counterparty is, how collateral is managed, how frequently exposure is reset, what happens if a counterparty fails to perform, and how the swap cost affects fund returns.

Terms such as funded swap or unfunded swap may appear in fund documents, but the practical task is to understand the counterparty, collateral, exposure limits, and cost disclosure.

Synthetic does not mean “bad.” It means the exposure route depends more on contract design, counterparty arrangements, collateral rules, and fund-document disclosure.

Physical vs synthetic ETF comparison table

The comparison is most useful when it focuses on structure rather than preference. A physical ETF and a synthetic ETF can both be designed to track the same benchmark, but the due-diligence questions are different.

| Criterion | Physical ETF | Synthetic ETF |

|---|---|---|

| Exposure route | Gets exposure mainly through owned securities. | Gets exposure mainly through swap or derivative economics. |

| What the fund holds | Usually index constituents, a representative sample, cash, and sometimes supporting instruments. | May hold collateral or substitute assets while the swap delivers the target return. |

| Counterparty risk | Usually lower direct swap-counterparty exposure, though securities lending can add counterparty considerations. | More central because swap counterparties are part of the exposure mechanism. |

| Transparency | Often easier to inspect through holdings disclosure, though sampling can still require review. | Requires review of swap counterparties, collateral policy, exposure limits, and disclosure quality. |

| Tracking behavior | Can be affected by sampling, trading costs, cash drag, fees, index changes, and securities lending. | Can be affected by swap terms, collateral arrangements, reset mechanics, fees, and counterparty pricing. |

| Costs | Expense ratio matters, along with trading, rebalancing, and securities-lending effects. | Expense ratio matters, and swap spreads or derivative costs can also affect outcomes. |

| Liquidity | Depends on ETF trading conditions, underlying market liquidity, fund size, and market-maker activity. | Depends on ETF trading conditions plus the structure and market access behind the swap exposure. |

| Tax and distributions | Treatment can depend on fund domicile, asset class, investor jurisdiction, and distribution policy. | Treatment can also depend on fund domicile, swap structure, investor jurisdiction, and distribution policy. |

| Main document checks | Holdings list, sampling policy, securities lending policy, fees, and tracking history. | Swap disclosure, counterparty list, collateral policy, fees, tracking history, and risk disclosures. |

The tracking section of a fund review should separate tracking error from tracking difference. A low tracking gap can be useful, but it should not be read in isolation from structure, cost, transparency, and risk controls.

Same-index example: same target exposure, different route

Example scenario: Two ETFs both target the same broad equity index. ETF A uses physical replication and holds most or all of the index constituents. ETF B uses synthetic replication and receives the index return through a swap arrangement.

On the surface, both funds may appear to offer the same benchmark exposure. The difference appears when an investor checks how the exposure is produced. ETF A raises questions about holdings, sampling, rebalancing costs, securities lending, and whether the owned basket closely matches the index. ETF B raises questions about swap counterparties, collateral quality, reset mechanics, swap cost, and disclosure.

The same benchmark label does not make the two structures identical. It only tells the investor what return stream the fund is trying to follow. The replication method explains how the fund attempts to deliver that exposure.

What to check in fund documents

The fund label is only the starting point. The factsheet, prospectus, KID or KIID, holdings list, and risk disclosures usually provide the evidence needed to confirm whether the ETF uses physical replication, synthetic replication, or a blend of techniques.

| Document check | Why it matters | What to look for |

|---|---|---|

| Replication method | Confirms whether exposure is holdings-based, swap-based, or mixed. | Terms such as full replication, optimized sampling, representative sampling, synthetic replication, swap-based, or unfunded/funded swap. |

| Holdings or substitute basket | Shows whether the fund owns benchmark constituents or a different collateral/substitute basket. | Constituent list, sector weights, cash positions, derivatives, or collateral basket disclosure. |

| Counterparty disclosure | Especially important for synthetic replication. | Counterparty names, exposure limits, collateralization rules, and risk controls. |

| Collateral policy | Shows what supports the swap exposure if the structure uses collateral. | Eligible collateral, haircut rules, diversification limits, valuation frequency, and custody language. |

| Securities lending policy | Can affect physical ETF risk and return characteristics. | Whether lending is allowed, who receives lending revenue, indemnification terms, and counterparty controls. |

| Expense ratio and swap costs | Costs affect the investor’s realized return relative to the benchmark. | TER or OCF, swap fee language, transaction costs, and any stated additional cost components. |

| Tracking history | Shows how closely the ETF has followed the benchmark after costs and structure effects. | Tracking difference, tracking error, performance against index, and periods of stress or market disruption. |

| Liquidity disclosure | Helps separate fund trading liquidity from underlying exposure mechanics. | ETF volume, bid-ask spread context, assets under management, market-maker support, and creation/redemption process. |

When physical replication can be useful

Physical replication can be useful when investors want a clearer connection between the fund and the underlying securities. A visible holdings list can make it easier to inspect sector exposure, country exposure, issuer concentration, sampling choices, and cash positions.

Physical structures may also be easier to explain to investors who want to understand what the fund owns. That simplicity can be valuable, but it should not be overstated. A physical ETF still needs review if it samples the benchmark, uses securities lending, trades in less liquid markets, or tracks an index with difficult-to-access constituents.

For broad, liquid equity indices, physical replication is often straightforward. For less liquid, international, fixed income, commodity-linked, or complex exposures, the implementation details matter more than the label.

When synthetic replication can be useful

Synthetic replication can be useful when direct ownership is difficult, expensive, restricted, or inefficient. Some exposures are hard to access through direct holdings, and a swap-based structure may deliver closer benchmark economics or lower implementation friction in certain cases.

The trade-off is that the investor must review a different set of risks. Instead of focusing only on constituent ownership, the review shifts toward counterparty exposure, collateral quality, swap cost, legal structure, and disclosure quality.

A synthetic ETF should not be rejected only because it is synthetic. It should be reviewed through the structure actually used by the fund. The important question is whether the fund documents make the exposure route, collateral framework, and counterparty risk understandable.

Common mistakes when comparing physical and synthetic ETFs

| Mistake | Why it is incomplete | Better check |

|---|---|---|

| Assuming physical is always safer | Physical ETFs can still involve sampling, securities lending, liquidity issues, and tracking gaps. | Review holdings, lending policy, liquidity, cost, and tracking record. |

| Assuming synthetic is always worse | Synthetic structures can be useful for difficult exposures, but they require counterparty and collateral review. | Read swap, collateral, exposure-limit, and counterparty disclosures. |

| Comparing only expense ratios | The headline fee may not capture trading costs, swap costs, lending revenue, tax effects, or tracking difference. | Compare total implementation quality, not only the stated annual charge. |

| Ignoring liquidity context | ETF trading conditions and underlying exposure access can affect execution and pricing. | Review spread, volume, fund size, market-maker support, and underlying market conditions. |

| Reading the benchmark name as the whole story | Two ETFs can target the same index while using very different mechanics. | Confirm the replication method, holdings or collateral, and risk disclosures. |

How replication method fits into the full ETF review

Replication method is one part of ETF due diligence. It should be reviewed alongside benchmark design, fund domicile, fees, liquidity, tax and distribution treatment, tracking record, issuer process, and the investor’s own constraints.

The broader review also depends on how the ETF trades relative to its portfolio value. The gap between ETF NAV and market price can matter during stressed conditions, thin trading, or when the underlying market is closed.

ETF trading also differs from traditional fund dealing. Understanding the difference between ETFs and mutual funds can help investors separate replication method from wrapper mechanics, intraday trading, and end-of-day NAV dealing.

Bottom line: Physical and synthetic replication are different implementation routes. Neither label is a complete risk assessment, quality score, or return forecast by itself.

FAQ

Do physical ETFs actually hold the assets?

Usually, yes. A physical ETF normally holds the underlying securities directly or through a representative sample. The holdings list and replication policy show how complete that exposure is.

Are synthetic ETFs riskier than physical ETFs?

Not automatically. Synthetic ETFs add counterparty, collateral, and swap-structure questions, while physical ETFs can still have sampling, securities lending, liquidity, and tracking issues. The risk comparison should be fund-specific.

How can I tell whether an ETF is physical or synthetic?

Check the factsheet, prospectus, KID or KIID, holdings disclosure, and risk section. Look for terms such as physical replication, optimized sampling, synthetic replication, swap-based exposure, collateral, and counterparty.

Is tracking difference more important than replication method?

Tracking difference is important, but it is not the only criterion. It should be reviewed alongside exposure route, costs, liquidity, counterparty setup, collateral, transparency, and tax or distribution notes.

Can two ETFs track the same index but use different replication methods?

Yes. Two ETFs can target the same benchmark while one holds the index securities and the other receives the benchmark return through a swap. The target exposure may be similar, but the implementation checks differ.