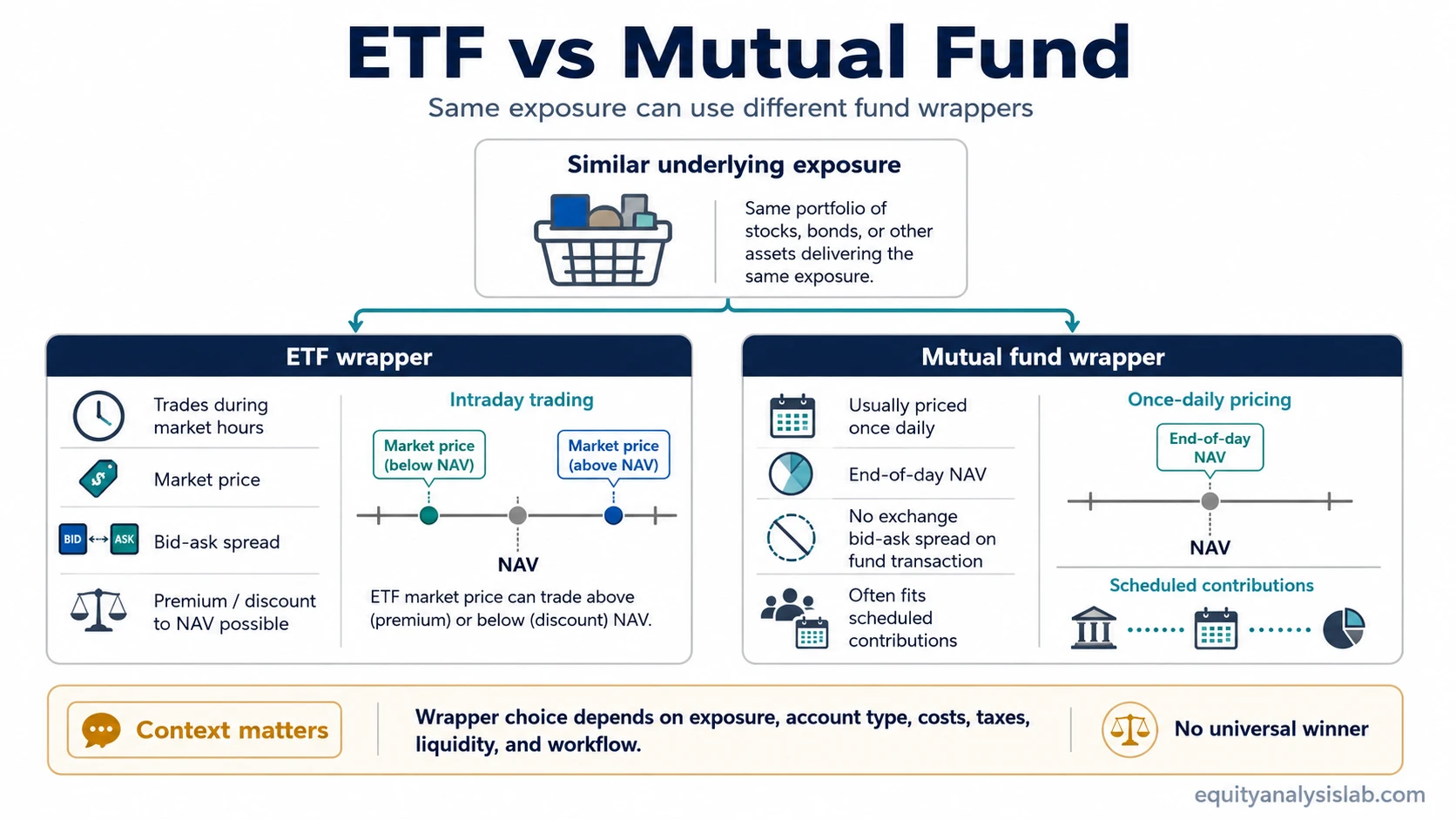

ETF vs mutual fund is a comparison between two fund wrappers that can hold similar portfolios but handle trading, pricing, taxes, liquidity, costs, and investor workflow differently. Neither wrapper is automatically better until the exposure, account type, and workflow are clear.

An ETF trades on an exchange during the day at a market price. A mutual fund usually transacts directly with the fund company once per trading day at net asset value, or NAV. That single difference changes how investors experience price, timing, spread cost, automation, and taxable-account mechanics.

One-line distinction: an ETF is an exchange-traded fund wrapper, while a mutual fund is usually a once-per-day NAV-priced fund wrapper. The comparison only becomes clean after the underlying exposure and investor use case are defined.

Key Points

- ETFs and mutual funds can hold similar baskets of stocks, bonds, or other assets.

- ETFs trade intraday at market prices, while mutual funds usually price once per day at NAV.

- ETF investors may face bid-ask spreads and market-price premiums or discounts; mutual fund investors usually transact at NAV.

- Tax efficiency, fees, minimums, fractional access, and recurring-investment features depend on fund structure, account type, and platform rules.

- A fair comparison starts with similar exposure; comparing different portfolios can confuse wrapper mechanics with investment strategy.

ETF vs Mutual Fund: Core Difference

The core difference is not the investment idea itself. The same broad market exposure can often be packaged inside either wrapper. The wrapper affects how the investor buys, sells, receives pricing, handles tax events, and fits the fund into an account workflow.

An ETF behaves more like an exchange-listed security from the investor’s point of view. The investor places an order during market hours and receives an execution at a market price that may be slightly above or below the fund’s NAV. A mutual fund behaves more like a pooled fund transaction. The investor submits an order, and the final price is usually determined after the market close from the fund’s NAV calculation.

Important boundary: ETF vs mutual fund is a wrapper comparison, not a quality ranking. A weak portfolio does not become stronger because it sits inside an ETF, and a strong portfolio does not become weaker because it sits inside a mutual fund.

ETF vs Mutual Fund Comparison Table

| Comparison point | ETF | Mutual fund | Why it matters |

|---|---|---|---|

| Trading method | Trades on an exchange during market hours. | Usually bought or redeemed directly with the fund company or through a platform. | ETF orders can be timed intraday; mutual fund orders usually settle from end-of-day pricing. |

| Pricing | Trades at a market price that can move during the day. | Usually priced once per day at NAV after the market close. | The ETF investor sees real-time market pricing, while the mutual fund investor usually receives the next calculated NAV. |

| NAV relationship | Market price can trade near, above, or below NAV. | Transactions usually occur at NAV. | ETF premiums and discounts create an extra comparison point that mutual fund investors usually do not face in the same way. |

| Bid-ask spread | May involve a bid-ask spread when buying or selling. | Usually no exchange bid-ask spread on the fund transaction itself. | The spread can act like an additional transaction cost for ETF investors, especially in less liquid conditions. |

| Expense ratio | Can be low, especially for broad index ETFs, but varies by fund. | Can be low or high depending on share class, strategy, and provider. | The wrapper does not guarantee a lower expense ratio; the actual fund terms matter. |

| Other costs | May include spreads, brokerage commissions where applicable, and premium/discount effects. | May include expense ratios, loads, redemption fees, or platform-specific fees where applicable. | Cost comparison should include both ongoing fund costs and transaction frictions. |

| Tax mechanics | Often has structural tools that can reduce capital-gain distributions, but exceptions exist. | May distribute capital gains when the fund realizes gains internally. | Tax comparison is contextual and depends on account type, fund strategy, turnover, and jurisdiction. |

| Minimum investment | Often accessible through share-based or fractional-share purchases, depending on the platform. | May have minimum initial investments, though some platforms and share classes reduce the barrier. | Access depends on the fund and platform rather than the wrapper alone. |

| Recurring investment | May support automated investing if the platform offers fractional or scheduled ETF purchases. | Often supports dollar-based recurring investment workflows. | The easier workflow depends on account setup and platform features. |

| Transparency | Many ETFs disclose holdings frequently, often daily, though structure varies. | Holdings disclosure may be less frequent depending on fund rules and reporting cycle. | Transparency can affect how easily an investor checks exposure and overlap. |

| Investor workflow | Useful when intraday tradability, exchange access, and price control matter. | Useful when NAV-based dealing, automatic contributions, and simple dollar-based workflows matter. | The better fit depends on account need, not on a universal wrapper ranking. |

Same Portfolio, Different Wrapper

A clean ETF vs mutual fund comparison starts with similar exposure. Consider two funds designed to track a similar broad stock index. One is packaged as an ETF, and the other is packaged as a mutual fund. The underlying portfolio goal may be similar, but the operating experience is different.

Same-exposure example: the ETF version can be bought during the trading day at the exchange price. The mutual fund version usually receives the end-of-day NAV. The ETF may involve a bid-ask spread and a small premium or discount to NAV. The mutual fund may fit more naturally into an automatic monthly contribution plan. The portfolio exposure may be similar, while the trading, pricing, tax, and workflow mechanics differ.

This distinction prevents a common mistake. If one investor compares a broad stock ETF with a bond mutual fund, the result does not isolate ETF vs mutual fund mechanics. It mixes wrapper differences with asset-class differences, duration risk, income profile, and portfolio objective.

Where the Comparison Often Goes Wrong

The comparison becomes misleading when the investor treats the wrapper as the whole decision. Fund quality still depends on exposure, index or active strategy, holdings, fees, turnover, tax context, risk profile, and how the fund fits the account.

Common mistake: comparing an ETF with one portfolio objective against a mutual fund with a different objective and then concluding that the wrapper caused the difference. A wrapper comparison should hold exposure as constant as possible before judging pricing, liquidity, costs, and tax mechanics.

A second mistake is treating intraday trading as automatically useful. Intraday access can matter for some investors, but it also introduces execution choices, spreads, order type considerations, and premium-discount awareness. For a long-term automatic investor, the ability to trade throughout the day may not be the most important feature.

Costs, Liquidity, and Tax Mechanics

Cost comparison should include more than the headline expense ratio. ETFs can have low expense ratios, but investors may also face bid-ask spreads and market-price execution. Mutual funds can also have low expense ratios, but some share classes or platforms may add loads, redemption fees, or other costs. The correct comparison is fund-specific.

ETF liquidity matters because the exchange price depends on trading conditions, market depth, spreads, and the relationship between the ETF shares and the underlying portfolio. A liquid ETF can still have wider spreads during stressed markets or when underlying holdings are less liquid.

ETF tax efficiency is often discussed because many ETFs use in-kind creation and redemption mechanics that can reduce taxable capital-gain distributions. That is a tendency, not a guarantee. Fund turnover, structure, holdings, account type, jurisdiction, and investor behavior can all change the tax result.

Limitation: tax and liquidity advantages are contextual. An ETF wrapper can improve certain mechanics, but it does not remove fund-level risk, market risk, tracking differences, tax complexity, or execution friction.

When an ETF or Mutual Fund May Fit Better

Neither wrapper is universally better. The more useful question is which wrapper fits the account workflow after the desired exposure has already been chosen.

| Account need | Wrapper that may fit the workflow | Reason to check |

|---|---|---|

| Intraday trading access | ETF | ETFs trade on exchanges during market hours, allowing market, limit, and other order workflows where available. |

| End-of-day NAV-based dealing | Mutual fund | Mutual funds usually transact at the fund’s calculated NAV after the market close. |

| Automatic dollar-based contributions | Often mutual fund, platform-dependent for ETFs | Many mutual fund workflows support scheduled investments; ETF automation depends on fractional and recurring order support. |

| Tax-sensitive taxable account analysis | Often ETF, but not automatically | ETF structure may reduce capital-gain distributions, but the actual tax result depends on the fund and investor context. |

| Simple exposure comparison | Either wrapper | If holdings, strategy, and costs are similar, the wrapper mainly changes operating mechanics. |

| Account or retirement-plan constraints | Depends on plan menu and platform | Some accounts provide only certain fund types, share classes, or purchase options. |

The practical sequence is exposure first, wrapper second. After the investor knows what portfolio exposure is needed, ETF vs mutual fund becomes a narrower decision about trading method, cost structure, tax mechanics, transparency, and workflow fit.

Related Concepts

ETF structure, trading liquidity, and tax mechanics each affect the wrapper comparison in different ways. ETF vs mutual fund is most useful after the fund’s holdings, strategy, costs, and role in a portfolio are analyzed separately.

- ETF explains the exchange-traded fund wrapper in more detail.

- ETF liquidity explains spreads, trading depth, and execution conditions.

- ETF tax efficiency explains the tax-mechanics discussion more directly.

FAQ

Is an ETF better than a mutual fund?

No wrapper is universally better. An ETF may fit investors who value exchange trading, intraday pricing, and certain tax mechanics, while a mutual fund may fit investors who prefer NAV-based dealing and automatic contribution workflows.

Can an ETF and mutual fund hold the same investments?

Yes. An ETF and a mutual fund can hold similar underlying exposure, such as a broad index portfolio. The wrapper changes trading, pricing, tax, liquidity, and operational mechanics, not automatically the investment quality.

Why can ETF market price differ from NAV?

An ETF trades on an exchange, so its market price is set by buyers and sellers during the day. That price can be slightly above or below the fund’s NAV, especially when spreads widen or underlying holdings are harder to price.

Are ETFs always more tax-efficient than mutual funds?

No. ETFs are often more tax-efficient because of structural creation and redemption mechanics, but exceptions exist. Fund turnover, account type, jurisdiction, holdings, and investor behavior can all affect the tax result.

Which is easier for recurring investments?

Mutual funds often support automatic dollar-based contributions, while ETF automation depends on whether the platform supports fractional shares and recurring purchases. The easier workflow is platform-specific.