Delta estimates an option’s current price sensitivity to a $1 move in the underlying security, all else equal. Gamma estimates how much that delta may change as the underlying moves.

The practical difference is that delta answers “how sensitive is the option right now?” while gamma answers “how quickly can that sensitivity change?” That distinction matters because an option can start with a moderate delta and become more or less sensitive as price, time to expiration, volatility assumptions, and moneyness change.

Key Points

- Delta is a current sensitivity estimate, not a guaranteed option price change.

- Gamma measures the rate of change in delta, not a separate direction forecast.

- Both readings are model-based estimates that assume other inputs remain unchanged.

- Gamma can matter more when an option is near the strike, especially as expiration gets closer.

- Delta should not be treated as a fixed probability or as stock ownership.

Delta vs Gamma Options: The Core Difference

In options, delta describes the approximate current change in an option’s theoretical price for a $1 move in the underlying security, assuming other pricing inputs stay the same. A call option with a 0.50 delta is commonly read as about $0.50 of theoretical sensitivity for a $1 upward move in the underlying, before considering changing inputs and market execution.

Gamma describes how much delta may change after the underlying security moves. If delta is the current sensitivity reading, gamma is the sensitivity of that sensitivity. It does not say the option should rise or fall on its own. It shows how unstable or responsive the delta reading may become as conditions change.

Delta vs Gamma Comparison Table

| Comparison point | Delta | Gamma |

|---|---|---|

| Main question answered | How sensitive is the option price right now? | How much can that sensitivity change? |

| Basic interpretation | Approximate option price change for a $1 underlying move, all else equal. | Approximate change in delta after the underlying moves. |

| What it measures | Current directional sensitivity. | Rate of change in directional sensitivity. |

| Common confusion | Misread as a guaranteed price change or fixed probability. | Misread as a separate bullish or bearish forecast. |

| Where it often becomes more noticeable | Across different strikes and moneyness levels. | Near the strike, especially when expiration is close. |

| What it does not show | Final profit, loss, probability, or suitability. | Direction, trade quality, or whether high sensitivity is good or bad. |

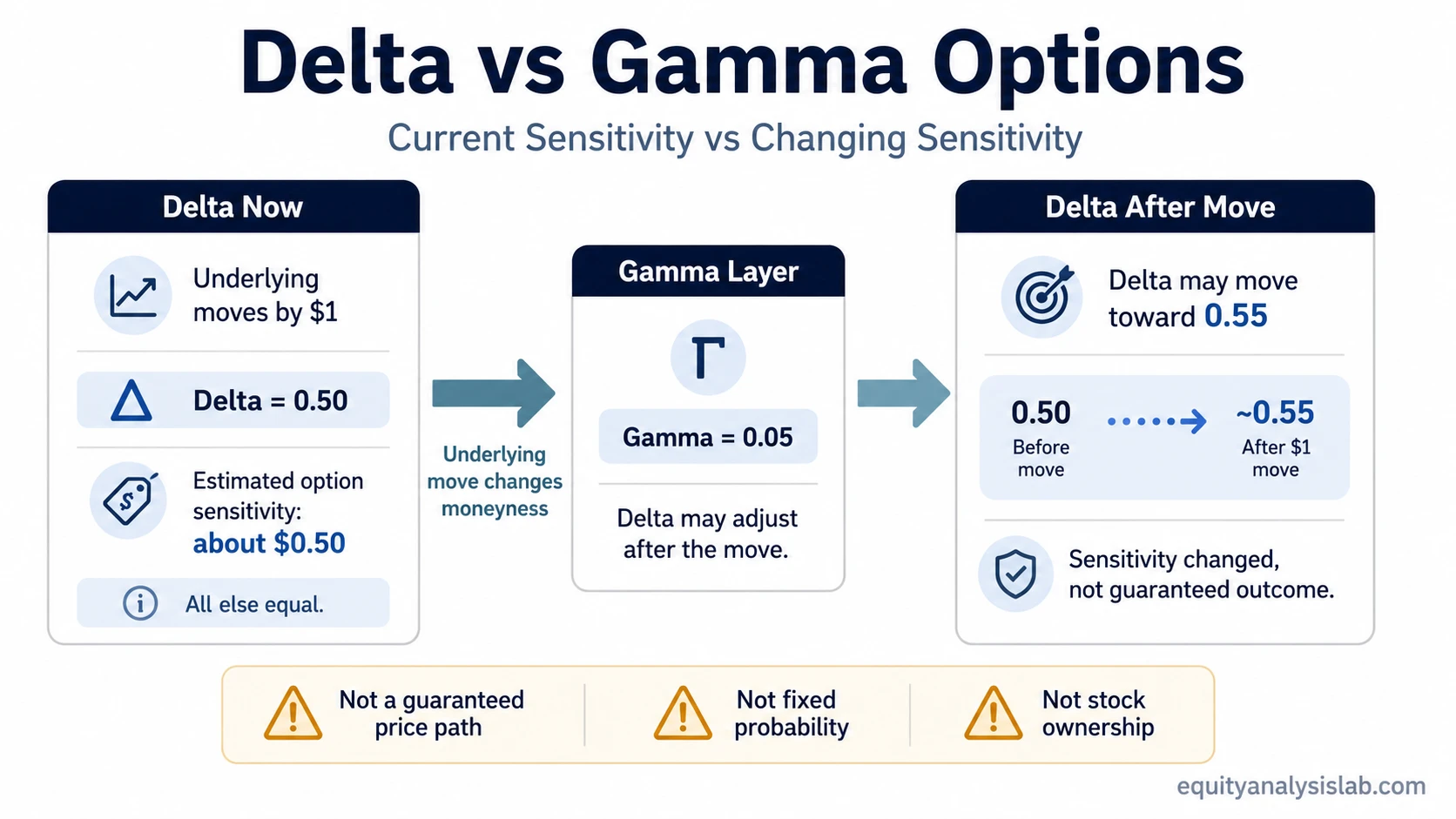

Same Option, Different Greek Readings

Assume a simplified option has a delta of 0.50 and a gamma of 0.05. If the underlying security rises by $1, the delta reading suggests about $0.50 of theoretical option price sensitivity, all else equal.

The gamma reading adds a second layer. After that $1 move, gamma suggests the option’s delta may move from about 0.50 toward about 0.55, depending on the model and other inputs. The first number describes the current sensitivity. The second number describes how that sensitivity may change after movement in the underlying.

Simplified example: Delta estimates the option’s sensitivity for the next $1 underlying move. Gamma estimates how different the next delta reading may become after that move. This is a model-based illustration, not a guaranteed price path and not a trade instruction.

Why Gamma Can Make Delta Less Stable

Delta is not fixed. It changes as the underlying price changes, as the option moves closer to or farther from the strike, as time passes, and as pricing assumptions shift. Gamma helps explain why the same option can have one sensitivity profile now and a different one later.

This can be especially noticeable near the strike price. A near-the-money option can move between lower and higher delta readings more quickly than a deep in-the-money or far out-of-the-money option. As expiration gets closer, that change can become sharper because small moves around the strike can have a larger effect on whether the option finishes in or out of the money.

Important limitation: Higher gamma does not automatically make an option better or worse. It means delta can change more quickly. Whether that matters depends on the contract, the underlying movement, time remaining, implied volatility assumptions, liquidity, and the investor’s risk context.

Common Delta and Gamma Confusion Traps

| Confusion trap | Cleaner interpretation |

|---|---|

| “Delta is the option’s guaranteed price change.” | Delta is an estimate under an all-else-equal assumption. Real option prices can move differently as volatility, spreads, and time value change. |

| “Delta is the exact probability of expiring in the money.” | Delta is sometimes used as a rough proxy, but it is not a fixed or complete probability measure. |

| “Gamma predicts direction.” | Gamma does not forecast whether the underlying will rise or fall. It measures how quickly delta can change if the underlying moves. |

| “A low delta option stays low sensitivity.” | Delta can increase or decrease as price, moneyness, time, and volatility assumptions change. |

| “Delta and gamma are strategy signals.” | They are sensitivity measures. They do not decide entry, exit, position size, suitability, or expected outcome. |

What Delta and Gamma Do Not Tell You

Delta and gamma do not show the full option value story. They do not capture every effect from time decay, implied volatility, bid-ask spreads, liquidity, contract mechanics, or changes in the broader pricing environment.

They also do not replace contract mechanics. Strike price, expiration date, premium, moneyness, and whether the contract is a call or put still shape the option’s payoff boundary. Delta and gamma describe sensitivity inside that pricing context; they do not convert the option into direct stock ownership.

Boundary note: Delta and gamma can help explain how an option’s theoretical price sensitivity may behave, but they do not determine whether a contract is appropriate, attractive, or likely to produce a specific result.

When to Look at Each Greek

Delta is most useful when the immediate question is current exposure. It helps compare how much one option’s theoretical price may respond to a small move in the underlying relative to another option, assuming other inputs do not change.

Gamma is most useful when the next question is stability. It helps show whether the current delta reading may remain relatively steady or change quickly as the underlying moves. For near-the-money options and contracts close to expiration, ignoring gamma can make delta look more stable than it really is.

Related Concepts

Delta is the standalone sensitivity measure for an option’s estimated response to an underlying price move. Gamma is the related measure that describes how that delta estimate can change as the underlying moves.

FAQ

What is the difference between delta and gamma in options?

Delta estimates an option’s current price sensitivity to a $1 move in the underlying security, all else equal. Gamma estimates how much delta may change after the underlying moves.

Does gamma change delta?

Gamma measures the rate of change in delta. If the underlying moves, gamma helps estimate how much the option’s delta reading may shift, depending on the model and other pricing inputs.

Is delta the same as probability?

No. Delta is sometimes used as a rough probability proxy, but it is not an exact or fixed probability of expiring in the money. It is primarily a sensitivity measure.

Is high gamma good or bad?

High gamma is not automatically good or bad. It means delta can change more quickly, which can make the option’s sensitivity less stable as the underlying moves.