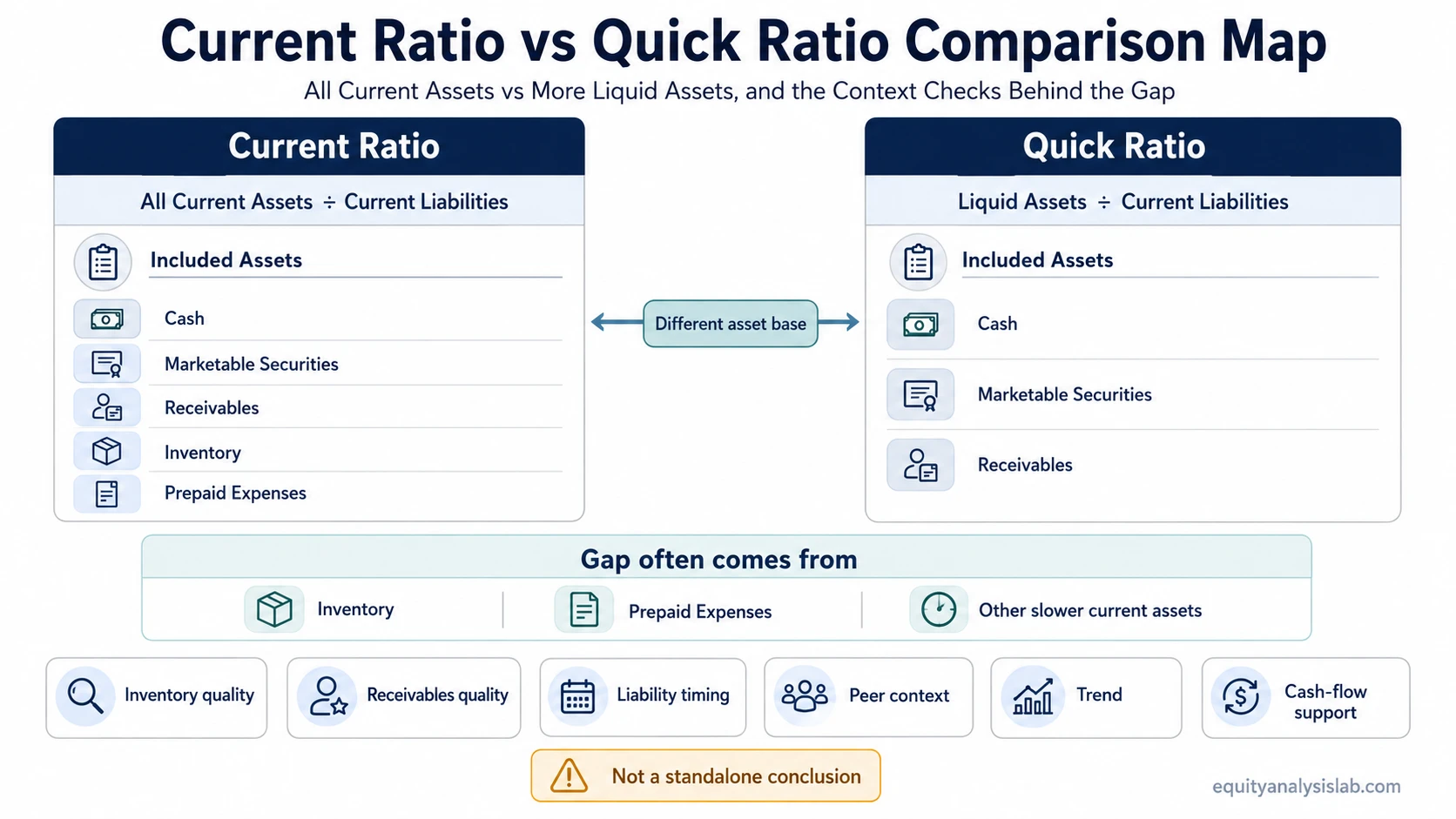

Current ratio compares all current assets with current liabilities, while quick ratio narrows the test to more liquid current assets such as cash, marketable securities, and receivables.

The difference matters because the current ratio can look stronger when a company holds large amounts of inventory or prepaid expenses. The quick ratio asks whether near-cash assets alone can cover short-term obligations. Neither ratio proves financial strength by itself, but the gap between them can show where a liquidity reading needs closer review.

Core distinction: current ratio is the wider liquidity test; quick ratio is the narrower liquidity test. The current ratio asks whether all current assets cover current liabilities. The quick ratio asks whether the more liquid portion of current assets can cover those liabilities without relying on inventory or other slower-to-convert assets.

Key Points

- Current ratio includes all current assets, so it is the wider short-term liquidity measure.

- Quick ratio excludes inventory and usually excludes prepaid expenses, so it is the more liquid-asset-focused measure.

- A large gap between the two ratios often points to inventory, prepaid expenses, or other current assets that may not convert into cash quickly.

- Neither ratio is a standalone investment conclusion, solvency guarantee, or proof of business quality.

Current Ratio vs Quick Ratio: Core Difference

The current ratio and quick ratio both compare current resources with current liabilities, but they use different definitions of “available” resources. Current ratio treats the full current-asset base as available for short-term obligations. Quick ratio filters that base and focuses on assets that are usually closer to cash.

This is why the comparison matters for balance-sheet liquidity analysis. A company can show an acceptable current ratio while still depending heavily on inventory conversion, customer collections, or other timing assumptions. A quick-ratio reading is narrower, but it still needs review around receivables quality, liability timing, and the company’s industry.

| Comparison point | Current ratio | Quick ratio |

|---|---|---|

| Main purpose | Tests whether all current assets cover current liabilities. | Tests whether more liquid current assets cover current liabilities. |

| Asset base | Full current-asset base. | Filtered quick-asset base. |

| Main exclusion issue | Does not exclude inventory or prepaid expenses. | Usually excludes inventory and prepaid expenses. |

| Investor question answered | How much short-term asset coverage exists on the balance sheet? | How much near-cash coverage exists without relying on slower assets? |

| Where it can mislead | Can look strong if inventory is large but slow-moving. | Can look cleaner but still overstate liquidity if receivables are weak or liabilities are urgent. |

| Best comparison context | Broad working-capital coverage and peer comparison. | Asset liquidity, inventory risk, and cash-conversion review. |

Formula and Input Differences

The formula difference is simple, but the interpretation depends on what sits inside current assets. Current ratio uses the full current-asset total. Quick ratio removes assets that may not become usable cash quickly enough to meet near-term liabilities.

Current ratio formula: Current ratio = current assets / current liabilities.

Quick ratio formula: Quick ratio = (cash + marketable securities + accounts receivable) / current liabilities.

Alternative quick ratio formula: Quick ratio = (current assets – inventory – prepaid expenses) / current liabilities.

The current-ratio calculation includes cash, receivables, inventory, prepaid expenses, and other current assets. The quick ratio focuses on cash-like resources and receivables while excluding inventory and prepaid expenses from the liquidity test.

| Input | Included in current ratio? | Included in quick ratio? | Why it matters |

|---|---|---|---|

| Cash | Yes | Yes | Cash is already available for obligations. |

| Marketable securities | Yes | Usually yes | These may be convertible into cash, depending on marketability and valuation risk. |

| Accounts receivable | Yes | Usually yes | Receivables depend on customer collection quality and timing. |

| Inventory | Yes | No | Inventory may require time, discounts, or uncertain demand before becoming cash. |

| Prepaid expenses | Yes | Usually no | Prepaids may reduce future expense needs but usually do not pay current liabilities directly. |

| Current liabilities | Denominator | Denominator | The timing and composition of liabilities affect how demanding the liquidity test really is. |

Same Company, Different Liquidity Reading

A same-company example shows why current ratio vs quick ratio can produce different liquidity readings even when the denominator is identical. The difference usually comes from how much of the asset base depends on inventory or prepaid expenses.

Illustrative example only: The numbers below are hypothetical and do not represent a real company filing or investment conclusion.

| Balance-sheet item | Hypothetical amount | Included in current ratio? | Included in quick ratio? |

|---|---|---|---|

| Cash | $20 million | Yes | Yes |

| Marketable securities | $10 million | Yes | Yes |

| Accounts receivable | $30 million | Yes | Yes |

| Inventory | $60 million | Yes | No |

| Prepaid expenses | $10 million | Yes | No |

| Total current assets | $130 million | Yes | Filtered |

| Current liabilities | $80 million | Denominator | Denominator |

| Ratio | Calculation | Result | Interpretation boundary |

|---|---|---|---|

| Current ratio | $130 million / $80 million | 1.63 | The company has broad current-asset coverage, but much of it depends on inventory and prepaid expenses. |

| Quick ratio | ($20 million + $10 million + $30 million) / $80 million | 0.75 | The liquid-asset-focused test shows less near-cash coverage before relying on inventory conversion. |

This example does not mean the company is automatically weak or strong. It means the current-ratio reading depends more heavily on inventory and other slower assets, while the quick-ratio reading pressures the analyst to examine cash, receivables, and liability timing more closely.

Gap interpretation filter: if current ratio is much higher than quick ratio, examine inventory quality, prepaid expenses, receivables, and liability timing before treating the broader ratio as comfortable. If both ratios are weak, check operating cash flow, short-term debt, and near-term maturities. If both ratios are strong, still check whether the liquid assets are recurring, unrestricted, and available for normal obligations.

What the Gap Between the Ratios Can Show

The gap between current ratio and quick ratio is often more useful than either number alone. A small gap can mean most current assets are already liquid or receivable-based. A large gap can mean inventory, prepaid expenses, or other slower assets make up a large part of short-term coverage.

That gap is not automatically bad. A retailer, manufacturer, or distributor may naturally carry more inventory than a software company. The issue is whether inventory can be sold at reasonable margins, whether receivables can be collected on time, and whether liabilities come due before assets convert into cash.

| Observed pattern | Possible meaning | Context check before interpreting |

|---|---|---|

| Current ratio much higher than quick ratio | Large share of current assets may sit in inventory, prepaid expenses, or other slower assets. | Check inventory turnover, markdown risk, receivables quality, and liability timing. |

| Both ratios low | Short-term coverage may be thin even before applying stricter asset filters. | Check cash-flow generation, credit access, debt maturity, and working-capital pressure. |

| Both ratios high | Current assets may exceed short-term obligations under both definitions. | Check whether cash is unrestricted, receivables are collectible, and excess liquidity is productive. |

| Quick ratio improving while current ratio is flat | Asset mix may be shifting toward cash, securities, or receivables. | Check whether the improvement comes from real cash generation or temporary balance-sheet timing. |

| Current ratio improving while quick ratio is flat | More of the improvement may be tied to inventory or other non-quick assets. | Check whether inventory is saleable and whether gross margins are stable. |

When Current Ratio Is More Useful

Current ratio is more useful when the analyst wants a broad view of working-capital coverage. It captures the full current-asset base and can be helpful when inventory is a normal, recurring, and saleable part of the company’s operating cycle.

For inventory-heavy companies, current ratio can provide context that quick ratio intentionally removes. The reading still needs inventory quality checks. Slow-moving goods, obsolete products, seasonal builds, or margin pressure can make the current ratio look stronger than the real cash-conversion profile.

Best use: use current ratio when broad short-term asset coverage matters and inventory is a meaningful part of normal operations.

When Quick Ratio Is More Useful

Quick ratio is more useful when the analyst wants a stricter view of short-term liquidity. It removes inventory and usually removes prepaid expenses, so it focuses on cash, marketable securities, and receivables.

This can be especially useful when inventory is hard to value, slow to sell, or vulnerable to discounts. It can also help when current liabilities are urgent and the analyst wants to know whether near-cash assets alone provide enough coverage. Quick ratio is stricter, but it is not perfect because receivables still depend on customer payment behavior.

Best use: use quick ratio when the key question is whether liquid assets can cover current liabilities without relying on inventory conversion.

Common Mistakes When Comparing the Ratios

The most common mistake is treating one ratio as automatically better. Current ratio and quick ratio answer different versions of the same liquidity question. Their usefulness depends on asset quality, liability timing, sector norms, and trend.

Mistake 1: treating thresholds as universal. A ratio that looks comfortable in one industry may be normal, weak, or excessive in another. The comparison should be tied to peer groups, business model, and liability structure.

Mistake 2: ignoring receivables quality. Quick ratio is more selective than current ratio, but it still includes receivables. If collections are weak, the quick ratio can overstate usable liquidity.

Mistake 3: ignoring sector inventory structure. A lower quick ratio may be more important for companies with uncertain inventory demand than for companies where inventory turns quickly and predictably.

Mistake 4: treating either ratio as a stock-selection signal. Liquidity ratios help frame balance-sheet risk, but they do not estimate intrinsic value, predict returns, or prove that a company is attractive.

Mistake 5: declaring one ratio universally better. The quick ratio is stricter, not automatically superior. The current ratio can still be useful when inventory is a normal and reliable part of the operating cycle.

How to Interpret Both Ratios Together

Interpret current ratio and quick ratio together by starting with the formula gap, then checking the assets and liabilities behind the numbers. The comparison is strongest when it moves from calculation to context rather than stopping at a single ratio level.

- Start with the current ratio: identify total current-asset coverage compared with current liabilities.

- Move to the quick ratio: remove inventory and other less liquid assets to test near-cash coverage.

- Measure the gap: a wider gap points to greater reliance on inventory, prepaid expenses, or other excluded assets.

- Check receivables: confirm whether customer collections are timely and reliable.

- Check inventory: review turnover, seasonality, margin pressure, and obsolescence risk.

- Check liabilities: compare the maturity and urgency of obligations against the timing of asset conversion.

- Compare peers and trend: evaluate whether the ratios are improving, weakening, or simply reflecting the company’s sector structure.

Interpretation boundary: current ratio and quick ratio are liquidity tools. They do not replace analysis of cash-flow quality, debt maturity, profitability, competitive position, or valuation.

FAQ

What is the main difference between current ratio and quick ratio?

Current ratio includes all current assets, while quick ratio uses only the more liquid portion of current assets. Quick ratio usually excludes inventory and prepaid expenses.

Why is quick ratio usually stricter than current ratio?

Quick ratio is usually stricter because it removes assets that may take longer to convert into usable cash. This makes it more focused on cash, marketable securities, and receivables.

Can a company have a strong current ratio but weak quick ratio?

Yes. This can happen when a large share of current assets is tied up in inventory, prepaid expenses, or other assets excluded from the quick ratio.

Is current ratio or quick ratio better?

Neither ratio is universally better. Current ratio is broader, quick ratio is stricter, and both need peer, sector, trend, receivables, liability, and cash-flow context.