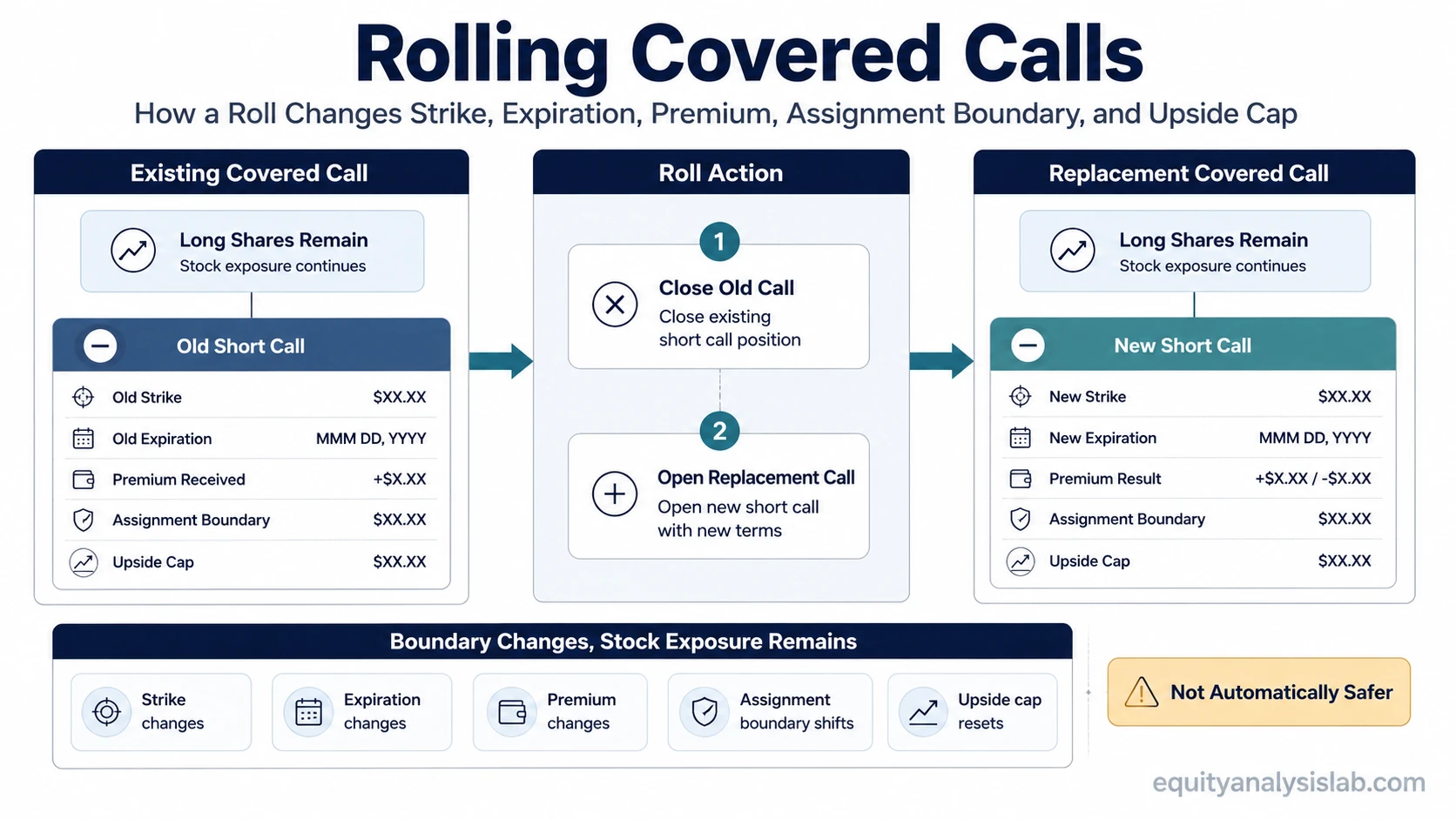

Rolling covered calls means closing an existing short covered call and opening a replacement call, usually with a different strike, expiration, or both. The roll changes the contract boundary, but it does not automatically remove assignment risk, improve the payoff, or make the position safer.

A covered-call roll is best understood as a reset of option terms attached to a stock position. The investor still owns the underlying shares, but the short-call obligation has been replaced with a new short call. That replacement call creates a new strike price, a new expiration date, a new premium result, and a new cap on possible stock upside.

Definition: Rolling a covered call is the process of buying back the current short call and selling another call against the same underlying shares, usually to change the strike, expiration, or both.

Key Points

- Rolling covered calls changes the short-call contract, not the fact that the stock position remains exposed to price movement.

- A higher strike, lower strike, or later expiration changes the assignment boundary and upside cap.

- A net credit can be useful information, but it is not a complete measure of whether the position improved.

- Repeated rolling can make the position harder to evaluate if call repurchase losses, longer exposure, and capped upside are ignored.

What Rolling Covered Calls Means

A covered call combines long shares with a short call option written against those shares. When that short call is rolled, the existing call is closed and a replacement call is opened. The new call may expire later, use a different strike price, or change both terms at the same time.

The covered-call part matters because the investor still owns the shares. The option adjustment is not separate from the stock position. If the replacement call remains open, the stock can still be assigned if the option is exercised, and the upside above the new short-call strike remains capped while the call is outstanding.

The same replacement-contract logic also appears in rolling an option, but the covered-call version is narrower because the replacement call is tied to share ownership, possible assignment, and the tradeoff between option premium and capped stock upside.

What Changes When a Covered Call Is Rolled

A roll changes the active option contract. It does not rewrite the original stock purchase, remove price risk from the shares, or guarantee that the new option position is better. The main question is which boundary moved and what new exposure was accepted in exchange.

| Contract element | What changes after a roll | Why it matters |

|---|---|---|

| Strike price | The replacement call may use a higher, lower, or similar strike. | The strike sets the new upside cap and assignment boundary. |

| Expiration | The replacement call often expires later than the original call. | More time can extend uncertainty and keep the stock capped for longer. |

| Premium | The roll may create a net credit or net debit after closing one call and opening another. | Cash flow does not by itself prove that risk improved. |

| Assignment risk | The risk may shift rather than disappear. | Moneyness, time remaining, extrinsic value, and expiration timing all affect the boundary. |

| Upside cap | The cap moves to the new short-call strike. | The stock may still be limited above that strike while the call remains open. |

| Volatility and extrinsic value | The roll price can change when option pricing inputs change. | A stable stock price does not guarantee stable roll economics. |

| Liquidity and friction | Bid-ask spread and execution costs may affect the result. | Quoted roll examples can look cleaner than the actual net economics. |

Assignment Risk and Expiration Boundaries

Rolling covered calls often becomes a visible question when the short call is near the strike, in the money, close to expiration, or connected to a stock that moved faster than expected. At that point, the investor may be comparing assignment, closing the call, or replacing it with another call.

The roll can move the assignment boundary, but it cannot make assignment risk vanish. A later expiration can give the position more time, while a higher strike can raise the upside cap. The tradeoff is that the investor now has a different call obligation instead of no obligation.

Near expiration, a stock trading close to the strike can also create uncertainty around final moneyness and possible assignment. That near-strike uncertainty is part of pin risk, especially when a small price move can change whether the call finishes in or out of the money.

Rolling Up, Rolling Down, and Rolling Out

Rolling language describes how the replacement contract differs from the original short call. These labels describe mechanics only. They do not say whether a roll is favorable, unfavorable, necessary, or appropriate.

| Roll type | Contract change | Main interpretation issue |

|---|---|---|

| Rolling up | The replacement call uses a higher strike. | The upside cap may move higher, but premium received may be lower than for a closer strike. |

| Rolling down | The replacement call uses a lower strike. | Premium may increase, but the stock can become capped at a lower level. |

| Rolling out | The replacement call uses a later expiration. | Time exposure extends, and the stock may remain capped for longer. |

| Rolling up and out | The replacement call uses a higher strike and later expiration. | The cap may rise, but the position accepts a longer option obligation. |

The same label can describe very different risk profiles. A roll up and out with meaningful extrinsic value left in the old call is not the same as a roll near expiration with little time value remaining. The label is a starting point, not the full analysis.

Why Premium Is Not the Full Risk Measure

Premium is one part of a covered-call roll, but it is not the whole position. A roll can generate a net credit and still leave the investor with a capped stock position, a later expiration, a new assignment boundary, and possible losses from buying back the original call.

A net credit can also mask the cost of time. If the new call expires much later, the investor may receive more premium because the new option contains more time value. That does not automatically mean the risk is lower. It may simply mean the investor accepted a longer period in which the stock remains subject to a short-call cap.

Limitation: A roll should not be judged only by whether it creates a credit or debit. The replacement strike, expiration, assignment boundary, capped upside, volatility sensitivity, and transaction friction all change the economic picture.

When Rolling Can Make the Position Harder to Interpret

Repeated rolling can make a covered-call position harder to evaluate because the visible premium received on the newest call may not show the full path of prior adjustments. The investor may have bought back earlier calls at losses, extended the short-call obligation several times, or kept the stock capped through multiple expiration cycles.

Example: Assume an investor owns shares and sold a covered call that later moves in the money. The investor buys back that call at a loss and sells a later-expiring call for a higher premium. The new transaction may show a net credit, but the position now has a later expiration, a new strike, and a longer period of capped upside. If the stock keeps rising, the replacement call may again become difficult to close without paying more than expected.

The issue is not that rolling is always wrong. The issue is that each roll changes the measurement point. Looking only at the latest premium can hide whether the position is improving, deferring assignment, extending exposure, or gradually converting stock upside into a series of option adjustments.

Rolling Covered Calls vs Rolling an Option

Rolling an option is a broad concept that can apply to calls, puts, long options, short options, spreads, and other option structures. Rolling covered calls is narrower because the short call is connected to shares the investor already owns.

That share ownership changes the interpretation. The investor is not only changing an option contract. The investor is also changing how much stock upside remains available, whether assignment is still possible, and how long the stock stays linked to a short-call obligation.

Related Option Position Risks

Three boundaries matter most when reading a covered-call roll. The first is the old short-call strike, where the original assignment question may have appeared. The second is the replacement strike, which becomes the new upside cap. The third is the new expiration date, which determines how long the replacement obligation remains active.

Tax treatment, account rules, early exercise practices, and broker-specific handling can affect real outcomes, but those details require account-specific review. For risk interpretation, the useful focus is the contract boundary: what was closed, what was opened, and which risks shifted rather than disappeared.

FAQ

Does rolling a covered call avoid assignment?

Rolling can move the assignment boundary by closing one short call and opening another, but it does not guarantee that assignment risk is gone. The replacement call can still be assigned if its terms and market conditions make exercise relevant.

Is a net credit always good when rolling a covered call?

No. A net credit is only one part of the roll. The new strike, later expiration, capped upside, assignment boundary, volatility sensitivity, and execution friction can all change the position’s risk profile.

What is the difference between rolling up and rolling out?

Rolling up changes the short call to a higher strike. Rolling out changes the short call to a later expiration. A roll can also do both at the same time by using a higher strike and a later expiration.