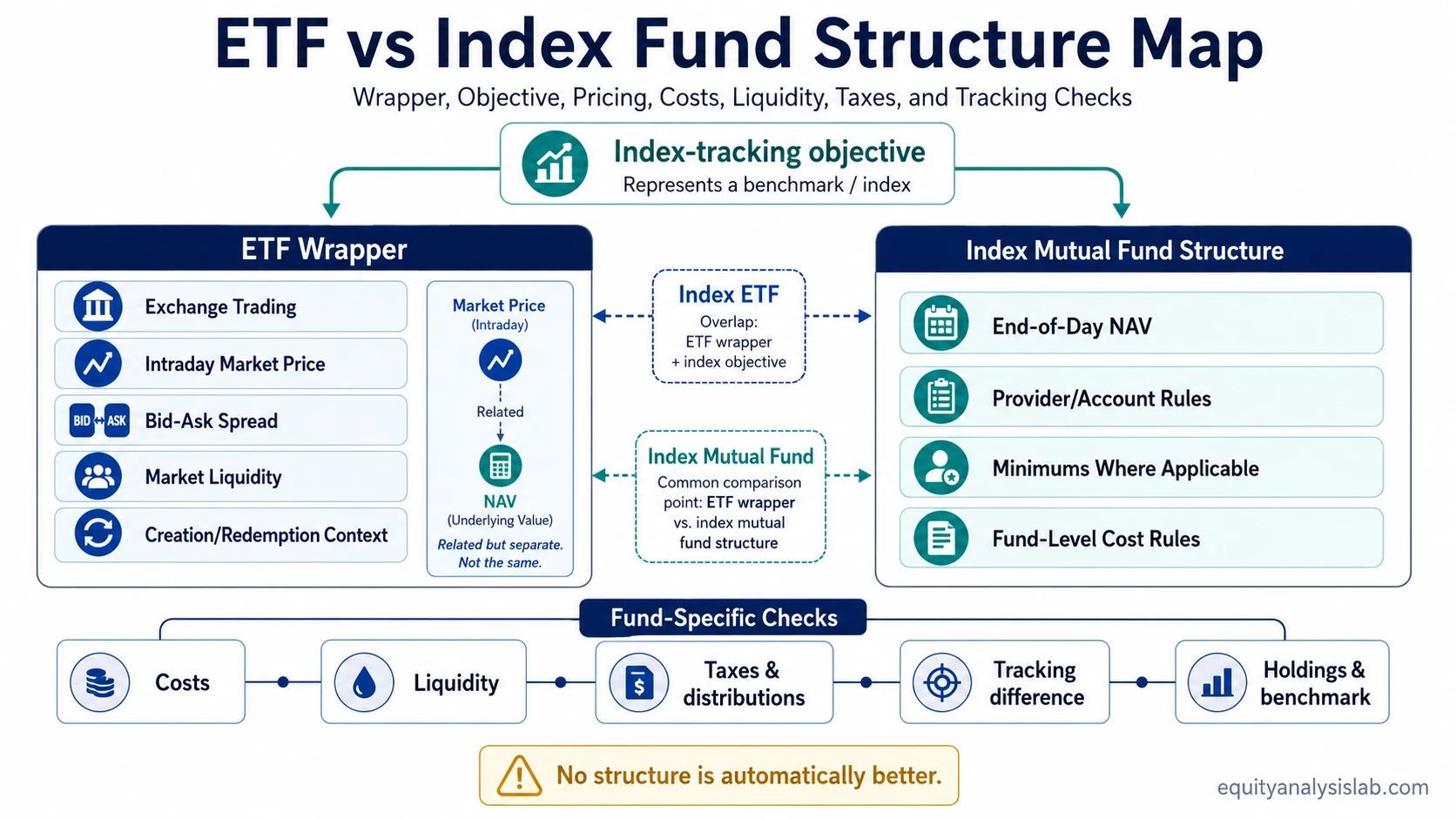

An ETF is a fund wrapper that trades on an exchange, while an index fund is an index-tracking fund category or objective. That means ETF vs index fund is not always a clean opposite: an index fund can be structured as an ETF or as an index mutual fund.

The useful comparison starts with two questions. First, what exposure is the fund designed to track? Second, what wrapper and trading structure delivers that exposure? The first question is about the index, holdings, or strategy. The second question is about how the fund is bought, sold, priced, taxed, and accessed.

Key Points

- An ETF describes the wrapper and exchange-traded structure.

- An index fund describes the objective of tracking an index.

- An index fund may exist as an ETF or as an index mutual fund.

- Cost, liquidity, taxes, distributions, tracking, and minimums depend on fund-level mechanics, not the label alone.

- The more precise comparison is often ETF wrapper versus index mutual fund structure, not ETF versus index exposure.

What Is the Difference Between an ETF and an Index Fund?

ETF: a fund wrapper that trades on an exchange during market hours. Its market price can move throughout the day, and trading may involve bid-ask spreads, order execution, and market liquidity.

Index fund: an index-tracking fund category or objective designed to follow a benchmark index. That index-tracking exposure can be delivered through different wrappers, including an ETF wrapper or an index mutual fund structure.

The confusion comes from comparing two labels that describe different layers. ETF describes how the fund is packaged and traded. Index fund describes what the fund is trying to follow. An index ETF combines both ideas: it is an ETF wrapper designed to track an index.

When investors say “ETF vs index fund,” they often mean “ETF vs index mutual fund.” That narrower comparison is about trading mechanics, pricing, conditional tax and distribution treatment, minimum investment rules, and how costs appear. It should not become a claim that one structure is always cheaper, more liquid, more diversified, or more suitable.

ETF vs Index Fund Comparison Table

| Criteria | ETF | Index Fund | What to Check |

|---|---|---|---|

| Core label | Wrapper and trading structure | Index-tracking objective or category | Check whether the comparison is really against an index mutual fund. |

| Trading mechanism | Trades on an exchange during market hours | May be an ETF or a mutual fund depending on structure | Separate exchange trading from index exposure. |

| Pricing | Has a market price that can change intraday | Index mutual funds generally transact at end-of-day NAV | Compare market price, NAV timing, and any premium or discount context. |

| Cost layers | May include expense ratio plus trading costs such as spreads or commissions where applicable | May include expense ratio, account rules, transaction fees, or minimums depending on provider | Do not treat expense ratio as the full cost picture. |

| Liquidity | Depends on visible market depth, bid-ask spread, trading volume, and underlying holdings | Depends on fund rules and redemption mechanics, especially for mutual fund structures | ETF liquidity mechanics matter when the ETF is bought or sold on exchange. |

| Minimum investment | Often depends on share price, fractional-share access, and brokerage rules | Index mutual funds may have minimum investment requirements or share-class rules | Check current platform and provider terms rather than assuming universal access. |

| Taxes and distributions | Tax treatment can depend on structure, creation/redemption mechanics, jurisdiction, account type, and distribution policy | Tax treatment can depend on fund turnover, distributions, share class, jurisdiction, and account type | Do not assume a universal tax advantage from the label alone. |

| Holdings and benchmark | Can track an index, follow an active strategy, or hold a different basket depending on mandate | Tracks a stated index, but fund rules and replication method still matter | Compare the benchmark, holdings, replication method, and tracking behavior. |

| Tracking difference | Can be affected by fees, trading, replication, cash drag, securities lending, and fund operations | Can be affected by fees, cash flows, sampling, distributions, and fund operations | Index tracking does not guarantee identical investor return to the benchmark. |

Same Benchmark, Different Wrapper Mechanics

Consider a generic broad-market index exposure available through two fund structures. One structure is an ETF that trades on an exchange during the day. The other is an index mutual fund that transacts through the fund company at end-of-day NAV.

The exposure label may look similar because both funds are designed around the same benchmark. The investor-facing mechanics still differ. The ETF may require attention to bid-ask spread, intraday market price, order type, and visible liquidity. The index mutual fund may require attention to minimum investment rules, transaction timing, share-class rules, and end-of-day pricing.

The benchmark answers the exposure question. The wrapper answers the access and trading-structure question. A clean comparison needs both layers before drawing conclusions about cost, liquidity, tracking, tax treatment, account constraints, platform rules, or fund-rule fit.

The Common Confusion: ETF, Index Fund, and Mutual Fund

Common mistake: treating ETF, index fund, and mutual fund as three mutually exclusive categories. They do not describe the same classification layer.

An ETF can be index-tracking or actively managed. A mutual fund can be index-tracking or actively managed. An index fund can be delivered through either an ETF wrapper or a mutual fund structure. The labels overlap because “ETF” describes the wrapper, while “index fund” describes the objective.

This distinction matters because an investor can compare two funds with similar index exposure and still face different trading rules, cost layers, tax and distribution mechanics, liquidity conditions, and platform constraints. The wrapper can change the experience of owning the exposure even when the benchmark appears similar.

Costs, Liquidity, Taxes, and Tracking Checks

ETF vs index fund comparisons often become too simple when they reduce the decision to a single label. A lower expense ratio does not automatically mean lower total cost. A fund that tracks an index is not automatically diversified enough for a specific portfolio. An exchange-traded wrapper does not guarantee tight spreads, deep liquidity, or permanent alignment between market price and NAV.

| Check | Why the Label Alone Is Not Enough |

|---|---|

| Expense ratio | It is only one cost layer. Trading costs, spreads, transaction fees, platform rules, and tax effects can also matter. |

| Bid-ask spread | ETF investors may pay an implicit trading cost when buying at the ask and selling at the bid. |

| Market price vs NAV | An ETF’s exchange price and underlying NAV are related, but they are not the same measure. |

| Tax treatment | Tax outcome depends on account type, jurisdiction, fund structure, turnover, distributions, and investor circumstances. |

| Tracking difference | Fees, replication, cash drag, sampling, distributions, and operational details can create a gap versus the benchmark. |

| Holdings and exposure | Two funds can reference similar index language while still differing in holdings, weights, sampling, currency exposure, or distribution policy. |

A Two-Question Frame for Comparing Funds

Question 1: What exposure is the fund designed to track?

This is the index, asset class, sector, strategy, geography, or factor exposure. It answers what the fund is trying to represent.

Question 2: What wrapper and trading structure delivers that exposure?

This is the ETF, mutual fund, or other structure used to access the exposure. It answers how the fund is bought, sold, priced, distributed, and operated.

The two questions should stay separate. A fund can have attractive exposure but inconvenient access mechanics. A fund can have convenient trading access but weak tracking, wide spreads, higher total ownership costs, or unsuitable exposure. The comparison becomes clearer when the exposure decision and wrapper decision are not collapsed into one label.

Limitations Before Comparing ETF and Index Fund Labels

An ETF label does not prove low cost, tax efficiency, liquidity, diversification, quality, or suitability. An index fund label does not prove low cost, diversification, tracking quality, or suitability. Each fund needs fund-level review.

Use the comparison as a structure check, not as a ranking system. The correct next step is to inspect the actual fund’s benchmark, holdings, replication method, expense ratio, spread, trading volume, distribution policy, tax context, tracking record, provider rules, and account constraints. Without fund-specific documents and current trading data, broad claims about one structure being better are not evidence-based.

FAQ

Is an ETF the same as an index fund?

No. An ETF is a wrapper that trades on an exchange. An index fund is a fund designed to track an index. Some index funds are ETFs, while others are index mutual funds.

Can an index fund be an ETF?

Yes. An index ETF is an ETF wrapper designed to track an index. The fund has both an index-tracking objective and exchange-traded ETF mechanics.

Why do people compare ETFs with index funds?

Many comparisons use “index fund” as shorthand for index mutual fund. The real distinction is often between exchange-traded ETF access and mutual fund access at end-of-day NAV.

Are ETFs always cheaper than index funds?

No. Cost depends on the specific fund. Expense ratio, bid-ask spread, transaction fees, platform rules, taxes, and tracking difference can all affect the total cost picture.

Do ETFs always have better liquidity?

No. ETF liquidity depends on market depth, bid-ask spread, trading volume, underlying holdings, and market conditions. The ETF label alone does not guarantee strong liquidity.