Options Greeks are measures that estimate how an option’s premium may respond to changes in the underlying price, time, implied volatility, and interest rates.

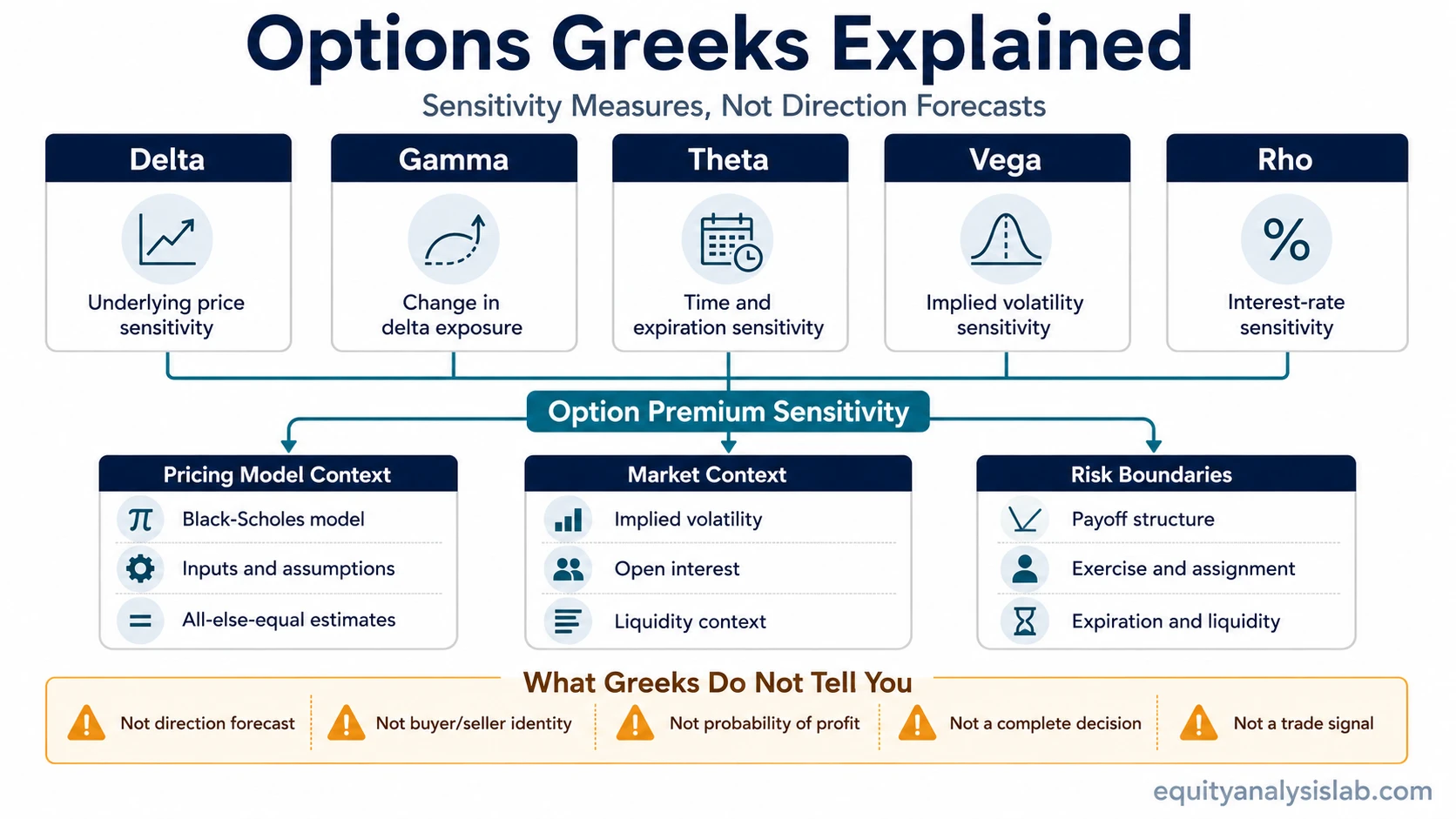

Delta, gamma, theta, vega, and rho separate different sources of option sensitivity. They can help an investor understand why an option premium changes, but they do not forecast market direction, identify buyer or seller intent, or replace payoff, liquidity, expiration, and assignment risk analysis.

Key Points

- Options Greeks estimate sensitivity inside option pricing, not market direction.

- Delta, gamma, theta, vega, and rho separate price, exposure-change, time, volatility, and rate sensitivity.

- Greek values should be read with payoff, expiration, liquidity, implied volatility, exercise, and assignment risk.

- A broad Greeks overview helps identify which sensitivity measure deserves closer study when one risk question becomes central.

What Are Options Greeks?

Options Greeks are model-based sensitivity measures. Each Greek isolates one input or relationship inside an option-pricing framework, usually under an all-else-equal assumption. That means a Greek can describe how a theoretical option value may react to one changing input, while real quoted premiums can still move differently when several inputs change at the same time.

Definition: Options Greeks are sensitivity estimates used to interpret option premium risk across price movement, time decay, volatility changes, interest-rate changes, and changes in delta exposure.

The useful starting point is not “which Greek is best.” The better question is what kind of risk the Greek is helping you check. Delta relates to underlying price sensitivity, gamma relates to how delta can change, theta relates to time sensitivity, vega relates to implied volatility sensitivity, and rho relates to interest-rate sensitivity.

The Main Options Greeks at a Glance

The main Greeks are easiest to read as a map of risk questions. They do not give a complete decision by themselves, but they help separate why an option’s premium may be sensitive to price, time, volatility, or rate assumptions.

| Greek or concept | Main question it helps answer | Boundary |

|---|---|---|

| Option delta | How sensitive is the option premium to a change in the underlying price? | Delta is not a guaranteed probability and not a direction forecast. |

| Gamma | How quickly can delta change as the underlying price changes? | Gamma risk can become more noticeable near the strike or near expiration. |

| Theta decay | How much does time sensitivity matter as expiration approaches? | Theta is not a guaranteed daily payout or a complete income estimate. |

| Volatility sensitivity | How sensitive is the premium to changes in implied volatility? | Vega does not tell whether the underlying will move in the expected direction. |

| Rho | How sensitive is the premium to interest-rate assumptions? | Rho is part of the Greek set, but it may be less central than price, time, and volatility sensitivity for many short-dated equity options. |

| Implied volatility assumption | What volatility assumption is embedded in the current option premium? | Implied volatility is not historical volatility and not a probability-of-profit figure. |

| Open interest | How much contract interest remains open after clearing? | Open interest is context, not proof of buyer identity, seller identity, or institutional intent. |

| Black-Scholes model | What model context can support theoretical option value and Greek estimates? | Model output is assumption-based and does not guarantee quoted premium behavior. |

How Greeks Relate to Option Premium

An option premium reflects several moving parts at once. The underlying price, strike price, time to expiration, implied volatility, interest-rate assumptions, expected dividends where relevant, bid-ask spread, and contract liquidity can all affect how the premium is quoted or interpreted.

Greeks try to isolate sensitivity to selected inputs. That isolation is useful, but it is also the source of a common mistake. A Greek value is usually read under an all-else-equal assumption, while real option markets rarely hold every other input still.

Simplified example: If an option has a delta near 0.50, an all-else-equal $1 move in the underlying may be associated with about a $0.50 change in theoretical option value. The actual premium can differ because implied volatility, time decay, spread, liquidity, and other inputs can change at the same time.

This is why Greeks are better treated as sensitivity estimates than as promises. They can clarify which input matters most, but they do not remove the need to check the full contract, payoff profile, expiration date, and market context.

What Each Greek Helps You Check

Delta translates underlying price movement into option-premium sensitivity. A higher absolute delta generally means the option’s theoretical value is more sensitive to a price change in the underlying. That does not mean high delta is automatically better, safer, or more suitable.

Gamma shows how quickly delta itself can change. This matters because an option’s exposure is not fixed. Near expiration or near a strike price, delta can shift quickly, so the option can behave differently from what a static delta reading suggested earlier.

Theta describes time sensitivity. It is often discussed as time decay, but reading it as guaranteed daily income is unsafe. Time decay can interact with implied volatility changes, underlying price movement, spread, and the remaining path to expiration.

Vega estimates sensitivity to changes in implied volatility. It is especially useful when an option premium appears expensive or cheap because volatility assumptions have changed. Vega does not say whether the underlying will rise or fall, and it does not turn implied volatility into a standalone trade signal.

Rho measures sensitivity to interest-rate assumptions. It belongs in the full Greek set, but for many equity-option discussions the immediate reading often centers first on price movement, gamma behavior, time decay, and implied volatility.

Common Mistakes When Reading Options Greeks

A beginner mistake is to treat Greeks as if they choose the option contract for you. They do not. Greeks describe sensitivity, while the decision still depends on payoff, risk, expiration, liquidity, implied volatility, position context, and whether the contract terms match the investor’s actual objective.

| Mistake | Why it is incomplete | Better reading |

|---|---|---|

| Using delta as a direction forecast | Delta estimates price sensitivity, not where the underlying will move next. | Read delta as exposure to underlying price movement. |

| Assuming high delta is automatically better | Higher sensitivity can also mean a different payoff and risk profile. | Compare delta with cost, payoff, expiration, and max-risk structure. |

| Treating theta as guaranteed income | Theta is theoretical time sensitivity, not a guaranteed cash-flow stream. | Check time decay alongside volatility, spread, and assignment risk. |

| Reading vega as a volatility trade signal | Vega shows sensitivity to implied volatility changes, not whether volatility should rise or fall. | Separate volatility exposure from trade selection. |

| Ignoring gamma near expiration | Delta can change quickly when price is near the strike and time is short. | Check how stable or unstable exposure may become before expiration. |

| Using open interest as proof of institutional intent | Open interest does not identify who opened contracts or why. | Use it only as contract-state and liquidity context. |

| Letting Greeks replace payoff review | Greek values do not show every possible loss, exercise, or assignment condition. | Read Greeks together with payoff, max risk, liquidity, expiration, and contract terms. |

Greeks, Payoff Risk, and Assignment Boundaries

Greek sensitivity is only one layer of option analysis. The payoff diagram, maximum risk, expiration date, moneyness, liquidity, spread, exercise style, and assignment conditions can matter as much as the Greek values themselves.

Risk boundary: Greeks can estimate sensitivity, but they do not define every outcome of the contract. An option can have clear delta, theta, vega, or gamma readings while still carrying payoff risk, liquidity risk, early-exercise considerations, or assignment risk depending on the contract and position structure.

Assignment and exercise risk should not be treated as an afterthought. The practical exposure of an option position can depend on whether the option is in the money, how close expiration is, whether dividends or exercise incentives are relevant, and whether the account can handle the resulting obligation if assignment occurs.

Liquidity also changes the usefulness of Greek interpretation. A theoretical value may look precise, but wide spreads or thin trading can make the observed premium less clean than the model output suggests.

Which Options Concept to Study Next

A broad Greek overview is useful for orientation, but a single risk question usually needs a more focused concept. Use the table below to match the question with the sensitivity measure or contract metric that best addresses it.

| If the question is… | Use this concept next | Why it matters |

|---|---|---|

| How much does the option respond to the underlying price? | Delta | Price sensitivity is usually the first exposure layer to understand. |

| How quickly can that exposure change? | Gamma | Changing delta can make exposure less stable than it first appears. |

| How much does time decay affect the premium? | Theta | Expiration can change the premium even without a favorable underlying move. |

| How much does implied volatility affect the premium? | Vega | Volatility assumptions can expand or compress premium independently of direction. |

| How much do interest-rate assumptions matter? | Rho | Rate sensitivity completes the standard Greek set and can matter more in selected contexts. |

| Why does the market price imply a certain volatility assumption? | Implied volatility | IV helps connect option premium to the market’s embedded volatility assumption. |

| How much contract interest remains open? | Open interest | Contract-state context can help evaluate participation and liquidity without implying direction. |

| What assumptions sit behind theoretical option value? | Black-Scholes model | Model context explains why Greek values are estimates rather than guarantees. |

FAQ

What are options Greeks?

Options Greeks are model-based sensitivity measures that estimate how an option’s premium may respond to changes in the underlying price, time, implied volatility, and interest-rate assumptions.

Which option Greek is most important?

There is no single best Greek in every situation. Delta, gamma, theta, vega, and rho answer different risk questions, so the most useful Greek depends on which input is driving the option premium and which risk needs to be understood.

Is delta the same as probability?

No. Delta can sometimes be used as a rough proxy in simplified discussions, but it is not a guaranteed probability and should not be treated as a forecast of where the underlying will finish.

Does theta mean guaranteed daily income?

No. Theta is a theoretical estimate of time sensitivity. It does not guarantee daily income because option premium can also change because of underlying price movement, implied volatility, liquidity, and spread changes.

What does vega measure?

Vega measures how sensitive an option’s theoretical value is to changes in implied volatility. It does not predict whether implied volatility will rise or fall.

Why can Greeks change before expiration?

Greeks can change because the underlying price, time to expiration, implied volatility, rates, and moneyness can change. Gamma is especially important because it describes how delta itself can shift as the underlying price moves.

Do Greeks replace payoff or assignment risk analysis?

No. Greeks help explain sensitivity, but payoff structure, maximum risk, liquidity, expiration, exercise terms, and assignment risk still need to be reviewed separately.