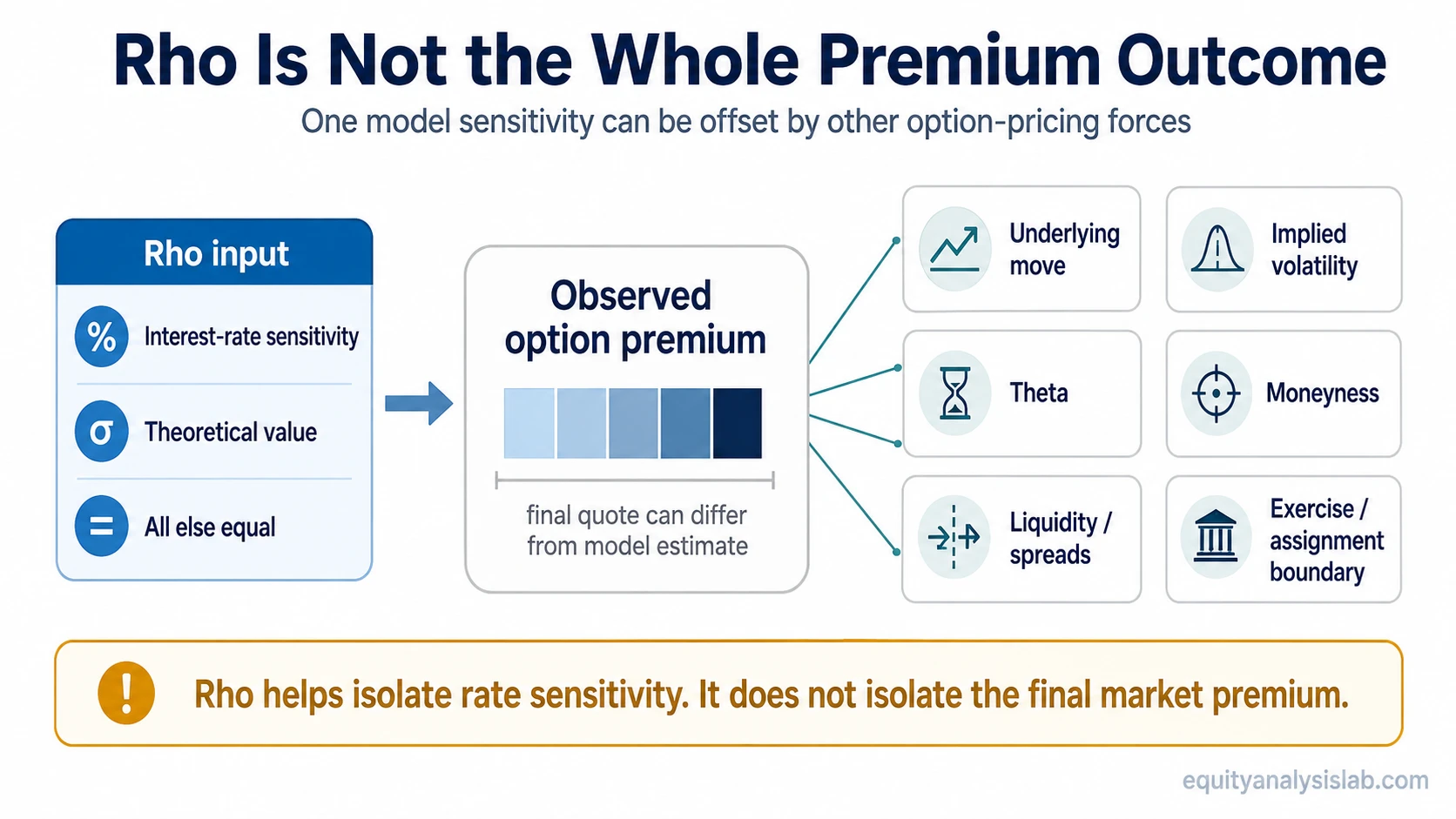

Rho does not show whether an option position will make money. It estimates how the theoretical value of an option may change if the risk-free interest rate changes, all else equal.

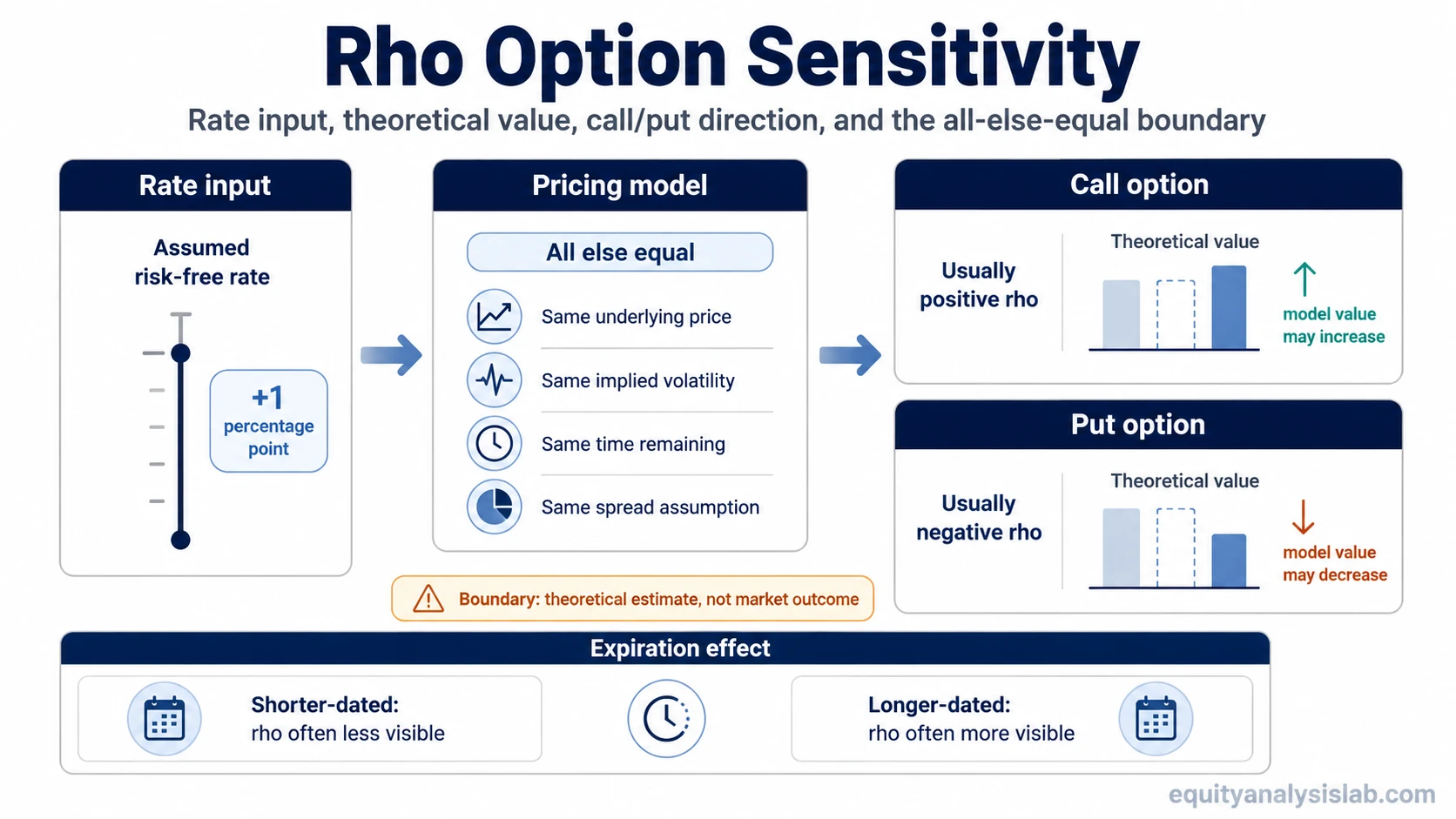

Rho is an options Greek that measures sensitivity to interest-rate changes. A rho value shows the estimated change in theoretical option premium for a 1 percentage-point change in the assumed risk-free rate, while other pricing inputs remain unchanged.

Call options usually have positive rho, while put options usually have negative rho. The effect is generally easier to notice in longer-dated options because interest-rate assumptions have more time to affect theoretical value.

Key points about rho

- Rho estimates theoretical option-value sensitivity to interest-rate changes.

- A 1 percentage-point rate-change convention is commonly used when reading rho.

- Calls generally have positive rho; puts generally have negative rho.

- Longer-dated options usually show more rho sensitivity than short-dated options.

- Rho does not describe payoff shape, forecast interest rates, or confirm a realized outcome.

What rho measures

Rho measures the interest-rate input inside theoretical option pricing. If a call has a rho of 0.25, a 1 percentage-point increase in the assumed risk-free rate would add about $0.25 to the theoretical option value, all else equal.

The all-else-equal condition is the boundary. The actual premium can move differently if the underlying price changes, implied volatility shifts, time value decays, or the quoted market spread changes at the same time.

Interest rates enter option pricing because the model treats money, time, and future exercise value as connected. The longer the time until expiration, the more room there is for the interest-rate assumption to affect the theoretical value of carrying or deferring exposure.

Rho belongs inside the broader theoretical pricing stack used by models such as the Black-Scholes model. It is one input sensitivity, not a complete description of option value.

How call rho and put rho differ

Call rho is usually positive because higher rates can increase the theoretical value of delaying the cash outlay needed to own the underlying asset. Put rho is usually negative because higher rates can reduce the present value of the put’s future exercise value in the model.

| Option type | Typical rho sign | Basic interpretation |

|---|---|---|

| Call option | Positive | Theoretical value may rise when the assumed risk-free rate rises, all else equal. |

| Put option | Negative | Theoretical value may fall when the assumed risk-free rate rises, all else equal. |

For short option positions, the exposure is inverted: a short call has the opposite rho exposure of a long call, and a short put has the opposite rho exposure of a long put.

The sign matters, but it does not override the rest of the option. A put can still rise while rates rise if the underlying price falls enough, and a call can still fall while rates rise if volatility drops or time decay dominates the premium change.

Why expiration changes rho sensitivity

Rho is usually more visible in longer-dated options because the interest-rate assumption affects the model over a longer period. Short-dated equity options often have much smaller rho exposure because there is less time for the rate input to matter.

Longer expiration does not make an option safer or more profitable. It can make rho easier to observe, while also leaving more room for theta, implied volatility, moneyness, liquidity, and spread changes to affect the premium.

How moneyness changes rho

Moneyness affects how much the model value depends on the future exercise relationship between the option strike and the underlying price. In-the-money options often show more visible rho than far out-of-the-money options because the exercise value is more relevant to the model.

The same rho value can mean different things depending on strike, underlying price, expiration, and contract type. A rho reading is most useful when it is compared with the rest of the option’s risk profile, not read as a standalone signal.

Simple rho example

For example, a call option with rho of 0.25 would be expected to gain about $0.25 in theoretical value if the assumed risk-free rate increased by 1 percentage point, all else equal.

That does not mean the option premium must rise by $0.25 in the market. If the underlying stock falls, implied volatility drops, time decay accelerates, or the bid-ask spread widens, the observed option price can move differently from the rho estimate.

What changes rho interpretation?

| Observable | Why it changes rho sensitivity | What it does not prove |

|---|---|---|

| Expiration length | Longer-dated options usually give the interest-rate input more time to affect theoretical value. | It does not prove the option has lower risk or a better outcome. |

| Call vs put | Calls usually carry positive rho, while puts usually carry negative rho. | It does not prove the premium will rise or fall in the quoted market. |

| Moneyness | Options with more meaningful exercise value can show rho more clearly than far out-of-the-money contracts. | It does not prove the strike is attractive or unattractive. |

| Underlying price level | Changes in the underlying can alter the option’s moneyness and make other Greeks more important. | It does not turn rho into an underlying-price sensitivity measure. |

| Rate move size | Rho is commonly read against a 1 percentage-point rate change, so smaller rate changes imply smaller theoretical effects. | It does not forecast the direction or timing of interest rates. |

| Implied volatility and theta | Volatility changes and time decay can offset or overwhelm the estimated rho effect. | It does not isolate the final premium outcome. |

| Liquidity and spreads | Wide spreads can make the observed tradable price differ from the theoretical value. | It does not prove the model estimate can be captured in execution. |

Common mistakes with rho

Mistake 1: Treating rho as payoff shape. Rho is a model sensitivity, not an expiration payoff diagram. Payoff depends on the underlying price relative to the strike at expiration, while rho estimates how the theoretical premium may respond to a rate input.

Mistake 2: Treating rho as a rate forecast. A positive or negative rho value does not predict where rates will go. It only estimates how the option model would respond if the assumed rate changed.

Mistake 3: Treating rho as a trade signal. Rho does not make an option attractive by itself. Underlying movement, volatility, theta, moneyness, spreads, and exercise or assignment conditions can matter more than the interest-rate sensitivity.

Rho compared with other option Greeks

Delta estimates sensitivity to the underlying price, while rho estimates sensitivity to the interest-rate input. A rate-sensitive option can still be dominated by underlying-price movement if delta exposure is large.

Gamma estimates how delta changes after the underlying moves. That makes gamma a different risk layer from rho, especially near the strike or close to expiration.

Gamma risk can become more important when small underlying moves quickly change directional exposure. Rho remains focused on the rate assumption inside the pricing model.

Theta, vega, implied volatility, liquidity, and spreads can all change the observed option premium. Rho is useful when the interest-rate input is relevant, but it should not be read as the whole option-risk picture.

Where rho is most useful

Rho is most useful when the option has enough time to expiration for interest-rate assumptions to matter. Longer-dated equity options and contracts with meaningful exercise value usually make rho easier to observe than very short-dated, far out-of-the-money options.

For many short-dated equity options, rho is often less influential than underlying-price movement, time decay, and implied-volatility changes. The practical use is interpretation: rho helps separate interest-rate sensitivity from other forces that may be moving the option premium.

FAQ

What does rho mean in options?

Rho means the estimated change in theoretical option value for a 1 percentage-point change in the assumed risk-free interest rate, all else equal.

Why is rho often smaller than other Greeks?

Rho is often less visible in short-dated equity options because interest-rate changes may have less time to affect theoretical value. Underlying-price movement, time decay, and implied volatility can have a larger effect on observed premium.

Does rho affect calls and puts differently?

Yes. Calls usually have positive rho, while puts usually have negative rho. The actual premium can still move differently when other pricing inputs change at the same time.