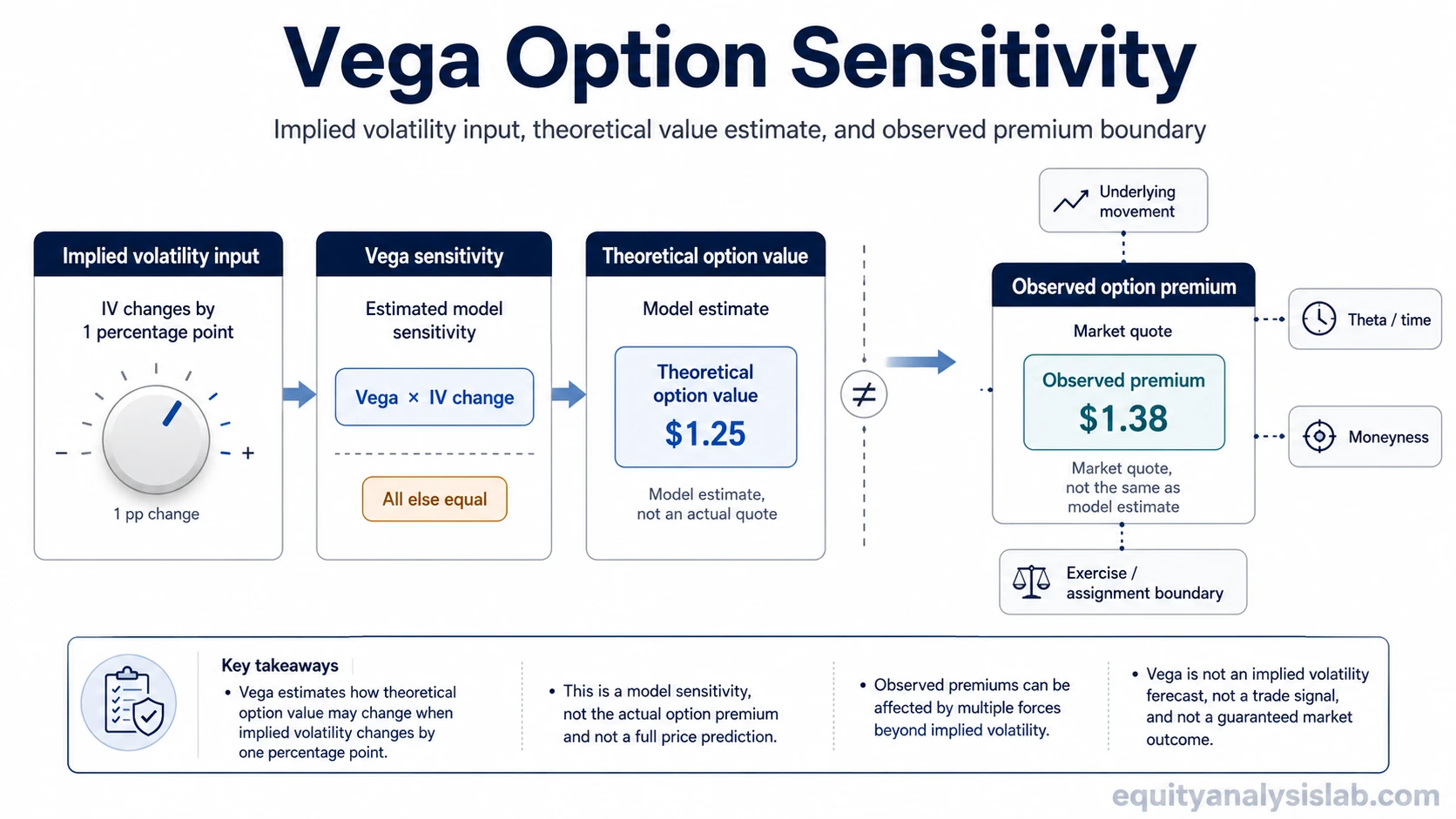

Vega is an option Greek that estimates how much an option’s theoretical value may change when implied volatility changes by one percentage point, while other pricing inputs stay unchanged. It measures sensitivity to implied volatility, not volatility itself and not a guaranteed change in the quoted option premium.

The useful boundary is simple: vega isolates one pricing input. The premium visible in the market can still move because of the underlying price, time decay, moneyness, bid-ask spreads, liquidity, and exercise or assignment conditions.

Vega definition

Definition: Vega measures an option’s sensitivity to implied volatility. If an option has a vega of 0.20, a one-percentage-point rise in implied volatility would add about 0.20 to the option’s theoretical value, all else equal. A one-percentage-point fall in implied volatility would subtract about 0.20, all else equal.

That estimate belongs inside an option-pricing model. The quoted market premium can differ from the model estimate because market makers, liquidity, spreads, and changing inputs can all affect the price available to a buyer or seller.

Key points about option vega

- Vega is tied to implied volatility, not to the option’s direction by itself.

- The standard reading is based on a one-percentage-point change in implied volatility.

- Higher vega means the theoretical option value is more sensitive to implied-volatility changes.

- Vega is usually larger when more extrinsic value remains in the contract.

- Vega does not predict the final premium outcome because other pricing forces can offset it.

How vega fits inside option pricing

Option premium is shaped by several inputs at the same time. The underlying price, strike price, time to expiration, implied volatility, interest-rate assumption, and dividend assumption can all affect theoretical value. Vega isolates the implied-volatility part of that pricing system.

The Black-Scholes model is one common way to understand why Greeks are model sensitivities rather than standalone forecasts. Vega does not say where implied volatility will go. It estimates how much theoretical value would change if implied volatility moved while the rest of the model inputs were held constant.

Simple vega calculation

Suppose an option is quoted with a theoretical value of 3.00 and a vega of 0.25. If implied volatility rises from 30% to 31%, the model estimate would move to about 3.25, assuming the underlying price, time, rates, dividends, and other inputs do not change.

If implied volatility falls from 30% to 29%, the same vega estimate would move the theoretical value toward 2.75, again under the all-else-equal assumption.

The calculation is useful because it shows the sensitivity. It is incomplete because real option quotes rarely change with only one input moving. The underlying may move at the same time, time may pass, and the bid-ask spread may change.

Vega, implied volatility, and option premium are different

Vega is often confused with implied volatility because the two terms appear together. Implied volatility is the pricing input. Vega is the sensitivity to that input. Option premium is the market price or quote that reflects implied volatility along with other contract and market conditions.

| Term | What it means | Common mistake |

|---|---|---|

| Implied volatility | A market-implied volatility input embedded in option pricing. | Treating it as a guarantee of future realized volatility. |

| Vega | The estimated change in theoretical option value for a one-percentage-point implied-volatility move. | Treating it as the premium change that must appear in the market quote. |

| Theoretical value | A model output based on pricing assumptions. | Reading it as the exact price a trader can transact at. |

| Observed premium | The actual option quote or transaction price available in the market. | Ignoring spreads, liquidity, and changing inputs around the quote. |

Why vega changes with time and moneyness

Vega is not fixed across every option. It changes as the contract moves through time, as the underlying price changes, and as the strike sits closer to or farther from the underlying price.

Options with more time until expiration often carry more sensitivity to implied volatility because there is more uncertainty left in the contract. As expiration approaches, less time remains for volatility assumptions to affect theoretical value, although near-expiration behavior can still become complex when the option is close to the strike.

Moneyness also matters. Options near the money often have more vega than contracts that are far in the money or far out of the money because a change in implied volatility has more room to affect the probability-weighted value of the contract. Deep in-the-money options may behave more like the underlying, while far out-of-the-money options may have low absolute premium even when percentage changes look large.

Long vega and short vega

A position is often described as long vega when it tends to benefit in theoretical value from rising implied volatility, all else equal. Long calls and long puts usually carry positive vega because higher implied volatility can increase the value of optionality.

A position is often described as short vega when it tends to lose theoretical value from rising implied volatility, all else equal. Short option exposure usually carries negative vega because higher implied volatility can make the obligation more expensive to close or mark.

Those labels describe sensitivity, not suitability. They do not say whether a position is attractive, safe, or profitable. They only describe how the position is exposed to an implied-volatility input.

What vega does not predict

Vega does not predict where implied volatility will move. It also does not guarantee that the option premium will rise or fall by the exact vega amount. The estimate assumes other inputs stay unchanged, while real quotes often change across multiple dimensions at once.

- Underlying movement: a stock move can change premium through delta exposure even if implied volatility moves in the expected direction.

- Time decay: theta can pressure extrinsic value as time passes, which may offset part of a favorable vega effect.

- Moneyness: a contract moving closer to or farther from the strike can change vega itself.

- Liquidity and spreads: a theoretical value change may not be fully available at the bid or ask.

- Exercise or assignment boundaries: American-style options and short-option positions can carry contract risks that a simple vega reading does not show.

Common vega mistakes

Reading high vega as automatically good: High vega means higher sensitivity to implied volatility. It can help or hurt depending on position direction, implied-volatility movement, and the rest of the option structure.

Confusing vega with volatility: Implied volatility is the input. Vega is the sensitivity to that input. Historical volatility and realized volatility are separate concepts.

Ignoring the market quote: A model may estimate a clean value change, but the actual premium can be shaped by the bid, ask, liquidity, and execution conditions.

Vega beside delta and gamma

Vega measures implied-volatility sensitivity. Option delta measures sensitivity to the underlying price. The distinction matters because an option can gain from one force while losing from another.

Gamma adds another layer by showing how delta changes as the underlying moves. Gamma risk becomes especially important when small underlying moves can quickly change directional exposure. Vega does not replace that risk; it only describes a different pricing dimension.

Related option-pricing concepts

Vega becomes easier to interpret when it is kept separate from nearby Greeks and volatility terms.

- How gamma changes delta explains why directional exposure can accelerate as the underlying moves.

- Theta explains time-related pressure on option value as expiration approaches.

- Rho explains sensitivity to interest-rate assumptions.

- Implied volatility explains the volatility assumption that vega responds to.

- IV crush explains how implied volatility can fall after an expected event and change option premium.

- Volatility smile explains why implied volatility can vary across strikes and expirations.

FAQ

Is vega the same as implied volatility?

No. Implied volatility is a pricing input. Vega is the estimated sensitivity of an option’s theoretical value to a one-percentage-point change in that input.

Do calls and puts both have vega?

Yes. Calls and puts can both have vega because both can be affected by changes in implied volatility. Long calls and long puts generally have positive vega, while short option exposure generally has negative vega.

Does vega predict the actual option premium?

No. Vega estimates one all-else-equal model sensitivity. The actual premium can also change because of the underlying price, time decay, moneyness, liquidity, spreads, and contract-specific conditions.