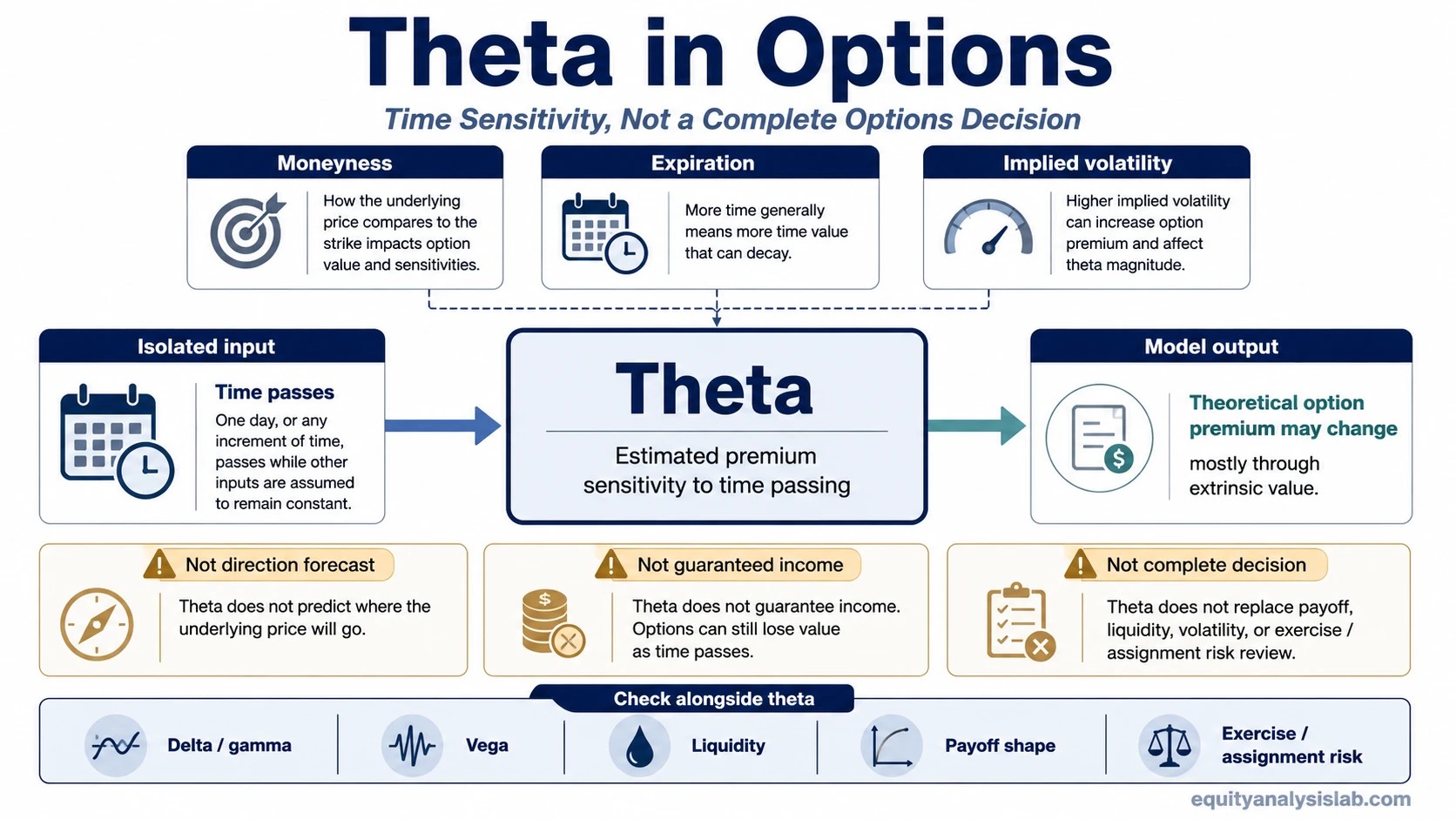

Theta in options is an options Greek that estimates how an option premium may change as time passes, assuming other pricing inputs remain constant.

Theta is a sensitivity measure, not a strategy, direction forecast, or guaranteed daily payout. It helps explain the time component of an option premium, but the actual premium can still change because of underlying price movement, implied volatility, moneyness, liquidity, and contract-specific risks.

Definition: Option theta measures the estimated change in an option’s theoretical premium from the passage of time, all else equal. For many long options, theta is shown as a negative number because time passing can reduce the option’s remaining time value. For some short or spread positions, theta exposure can appear positive, but that does not make it guaranteed income.

Key Points About Theta

- Theta estimates how option premium may change as time passes, all else equal.

- Theta mainly relates to extrinsic value, also called time value, rather than intrinsic value.

- Theta is usually not linear; in many model readings, time sensitivity can become more pronounced as expiration approaches.

- Underlying movement, implied volatility, moneyness, liquidity, and exercise or assignment conditions can change the result.

- Theta alone is not a complete options decision.

How Theta Works in Option Pricing

Theta is one input in the option-pricing framework. It isolates the effect of time passing while holding other variables steady, including the underlying price, volatility assumption, interest-rate input, and strike relationship. That isolation is useful for analysis, but it is also the reason theta should not be read as a guaranteed real-world result.

In a pricing model, the Black-Scholes model is one common reference point for understanding how time, volatility, strike price, and underlying price interact. Theta is derived from that kind of model logic, so it reflects theoretical sensitivity rather than a separate market forecast.

The practical reading is simple: theta answers one narrow question. If time passes and the other pricing inputs do not change, how much might the option’s theoretical value change?

Theta, Time Decay, and Extrinsic Value

Time decay is the process. Theta is the measurement used to estimate that process inside the option premium.

An option premium can contain intrinsic value and extrinsic value. Intrinsic value reflects the amount by which an option is in the money. Extrinsic value reflects the remaining time, volatility assumption, and uncertainty around what can still happen before expiration. Theta is most closely connected to this extrinsic portion because time passing reduces the amount of uncertainty left in the contract.

This distinction matters because theta should not be treated as a standalone explanation for every premium change. If an option gains value because the underlying moves favorably or implied volatility rises, that change can offset the pressure from theta. If volatility falls or the underlying moves against the option, premium can decline faster than the theta figure alone would suggest.

A Simple Theta Example

Suppose an option is quoted with a theta of -0.05. In a simplified reading, that may indicate a theoretical premium decline of about five cents over the model’s time unit if the underlying price, implied volatility, rates, and other inputs remain unchanged.

The time unit and display convention can vary by model, data provider, and platform, so the theta value should be read with the quote source’s convention in mind.

That does not mean the option must lose exactly five cents in the next session. If the underlying price moves sharply, if implied volatility changes, or if spreads widen, the observed premium can move differently from the isolated theta estimate.

The example separates a model sensitivity from a realized premium path. Theta describes decay pressure under controlled assumptions. The market does not keep every assumption fixed.

Why Theta Is Not Guaranteed Daily Income or Loss

A common mistake is to treat theta as a fixed amount that must be earned or lost each day. That is too mechanical. Theta can change as expiration approaches, as the option moves in or out of the money, and as implied volatility changes.

Positive theta does not guarantee profit for an option seller or spread holder. Negative theta does not guarantee loss for an option buyer. The option’s total premium still reacts to price movement, volatility, and the changing sensitivity of the position. Delta exposure can offset or dominate theta when the underlying moves enough.

The safer interpretation is that theta describes time pressure. It does not describe the whole position.

Why Theta Can Change Near Expiration

Theta is often more sensitive as expiration gets closer, especially for options near the money. This is a common theoretical pattern, not a universal rule that applies identically to every strike, expiration, volatility regime, or contract.

Near-the-money options can still shift between having meaningful intrinsic value and expiring with no intrinsic value, so the remaining extrinsic value can decay more quickly as the deadline approaches. Deep in-the-money options may have more intrinsic value and less extrinsic value as a share of total premium. Far out-of-the-money options may have limited remaining premium if the market assigns a low probability of finishing in the money.

This is why theta should be read with moneyness, time to expiration, and volatility context. The same theta number can carry different meaning depending on where the option sits relative to the strike and how much time remains.

What Changes Theta Interpretation

Theta becomes more useful when the reader also checks which variables can offset it. A position can appear to have favorable theta but still be exposed to adverse price movement, volatility changes, liquidity costs, or exercise and assignment conditions.

| Condition | How it affects theta interpretation | Why theta alone is incomplete |

|---|---|---|

| Underlying price movement | Price movement can increase or reduce the option premium faster than time decay alone. | The position’s price sensitivity may dominate the isolated theta estimate. |

| Implied volatility change | Rising or falling implied volatility can change extrinsic value. | Vega exposure can offset or amplify the visible effect of theta. |

| Moneyness | At-the-money, in-the-money, and out-of-the-money options can show different theta behavior. | The same time passage does not affect every strike in the same way. |

| Expiration | Theta can become more sensitive as expiration approaches in many model readings. | Decay pressure is not always linear across the life of the contract. |

| Liquidity and spreads | Wide bid-ask spreads can make the observed premium harder to interpret. | The model value may not match the executable market price. |

| Exercise or assignment conditions | Contract mechanics can matter, especially near expiration or around dividend-sensitive situations. | The Greek does not replace contract-risk review. |

Positive Theta and Negative Theta

Negative theta usually means the position is exposed to time decay in a way that can reduce theoretical value as time passes, all else equal. Long single options often show this kind of theta because the holder owns time value that can decay.

Positive theta usually means the position may benefit from time passing under the model assumptions. Some short option positions and certain spreads can show positive theta exposure. That still does not remove directional risk, volatility risk, liquidity risk, or assignment risk.

The important point is exposure, not judgment. Positive theta is not automatically good, and negative theta is not automatically bad. The position must still be evaluated through payoff shape, volatility assumptions, liquidity, and the underlying scenario.

Theta Compared With Other Greeks

Theta measures sensitivity to time. Other Greeks isolate different sources of option-premium sensitivity.

Delta focuses on the relationship between option value and the underlying price. Gamma explains how that directional exposure can change as the underlying moves, so gamma risk becomes relevant when a position can change exposure quickly.

Vega focuses on implied volatility sensitivity. This matters because the market can reprice uncertainty even while time is passing. A negative-theta option can still rise if implied volatility or underlying movement increases the premium enough. A positive-theta position can still lose if volatility or price movement works against the structure.

A separate gamma reading is useful when the question shifts from time decay to how quickly price sensitivity itself can change around the strike.

What Theta Tells You and What It Does Not Tell You

| Theta can help estimate | Theta does not tell you | What to check next |

|---|---|---|

| How time passing may affect theoretical premium, all else equal. | Whether the option position will be profitable. | Payoff shape, premium paid or received, and scenario risk. |

| How much time-value pressure may exist in the position. | Whether the underlying will rise, fall, or stay in a range. | Underlying thesis, volatility context, and price sensitivity. |

| Whether time decay is a meaningful part of the option’s risk profile. | Whether positive theta is safe income. | Volatility risk, directional exposure, and assignment conditions. |

| How expiration may influence the option’s premium sensitivity. | Whether decay will occur smoothly each day. | Moneyness, expiration proximity, and implied volatility shifts. |

| How one Greek fits into a broader options analysis process. | Whether the option is a complete or suitable decision. | Liquidity, spreads, contract mechanics, and portfolio-level risk. |

Common Mistakes When Reading Theta

Mistake 1: Reading theta as a fixed daily cash flow. Theta is a model-based estimate, not a guaranteed amount that must appear in the account each day.

Mistake 2: Ignoring volatility. Implied volatility can change the extrinsic value of an option and make the observed premium move differently from the theta estimate.

Mistake 3: Treating theta as a strategy. Theta is a Greek. It can support analysis, but it does not replace payoff analysis, position sizing, liquidity review, or contract-risk review.

Mistake 4: Separating the option from the underlying. The underlying scenario still matters because the option’s premium is derived from the asset, index, or instrument beneath the contract.

How to Use Theta Safely in Analysis

The safest use of theta is as one diagnostic input. It helps identify how much time pressure is embedded in the position and whether expiration timing is likely to matter. It should be read alongside the underlying scenario, moneyness, implied volatility, liquidity, and payoff structure.

For an investor learning options mechanics, the main boundary is clear: theta helps explain premium sensitivity, not investment merit. A position can have attractive time-decay characteristics and still be unsuitable if the payoff, volatility exposure, liquidity, or assignment risk is poorly understood.

Limitation: Theta becomes most interpretable when other inputs are stable. Real option premiums rarely move with only time changing, so the observed result can differ from the model estimate.

FAQ

What does theta mean in options?

Theta means the estimated change in an option’s theoretical premium from the passage of time, assuming other pricing inputs stay constant. It is a sensitivity measure, not a prediction of the option’s full price path.

Does theta mean an option loses money every day?

No. A negative theta figure can show time-decay pressure, but the option premium can still rise if underlying movement or implied volatility offsets that pressure.

Is positive theta guaranteed income?

No. Positive theta can mean the position may benefit from time passing under model assumptions, but price movement, volatility changes, liquidity, and assignment risk can still create losses.

How is theta different from time decay?

Time decay is the process of time value declining as expiration approaches. Theta is the Greek used to estimate that time-related premium sensitivity under a pricing model.