Open interest in options is the number of contracts that remain open for a specific option after opening trades, closing trades, exercise, assignment, and expiration effects are reflected. Volume counts trading activity during a period, while open interest shows how much contract exposure remains after clearing. Open interest can help investors read participation and liquidity context, but it does not forecast price direction, identify who is buying or selling, or create a trade decision by itself.

Definition: Open interest in options is the number of outstanding contracts that have not been closed, exercised, assigned, or expired. It is read at the individual contract level, usually by underlying asset, call or put, strike price, and expiration date.

Key Points

- Open interest options count contracts that remain open, not every trade that has ever occurred.

- Volume measures transactions during a period, while open interest reflects remaining contracts after clearing.

- Open interest should be read by contract, strike, expiration, and call or put side.

- Higher open interest can suggest more participation or better liquidity context, but it does not predict direction.

- Open interest does not reveal buyer identity, seller identity, institutional intent, or profitability by itself.

What Open Interest Means in Options

Open interest is contract-state data. It shows how many contracts remain open for a specific option after the market has processed opening and closing activity. A call option and a put option on the same underlying do not share one open-interest number; each contract has its own count based on strike, expiration, and option type.

That makes open interest different from a broad stock-level signal. A stock may have many option contracts across different expirations and strikes, and each contract can show a different level of participation. Reading one open-interest number without checking the contract details can create a misleading impression of where activity is concentrated.

Open interest is also not a pricing model input by itself. Pricing models such as the Black-Scholes model focus on variables such as underlying price, strike price, time to expiration, volatility, interest rates, and dividends. Open interest instead helps describe participation and remaining contract exposure around a specific option.

How Open Interest Changes

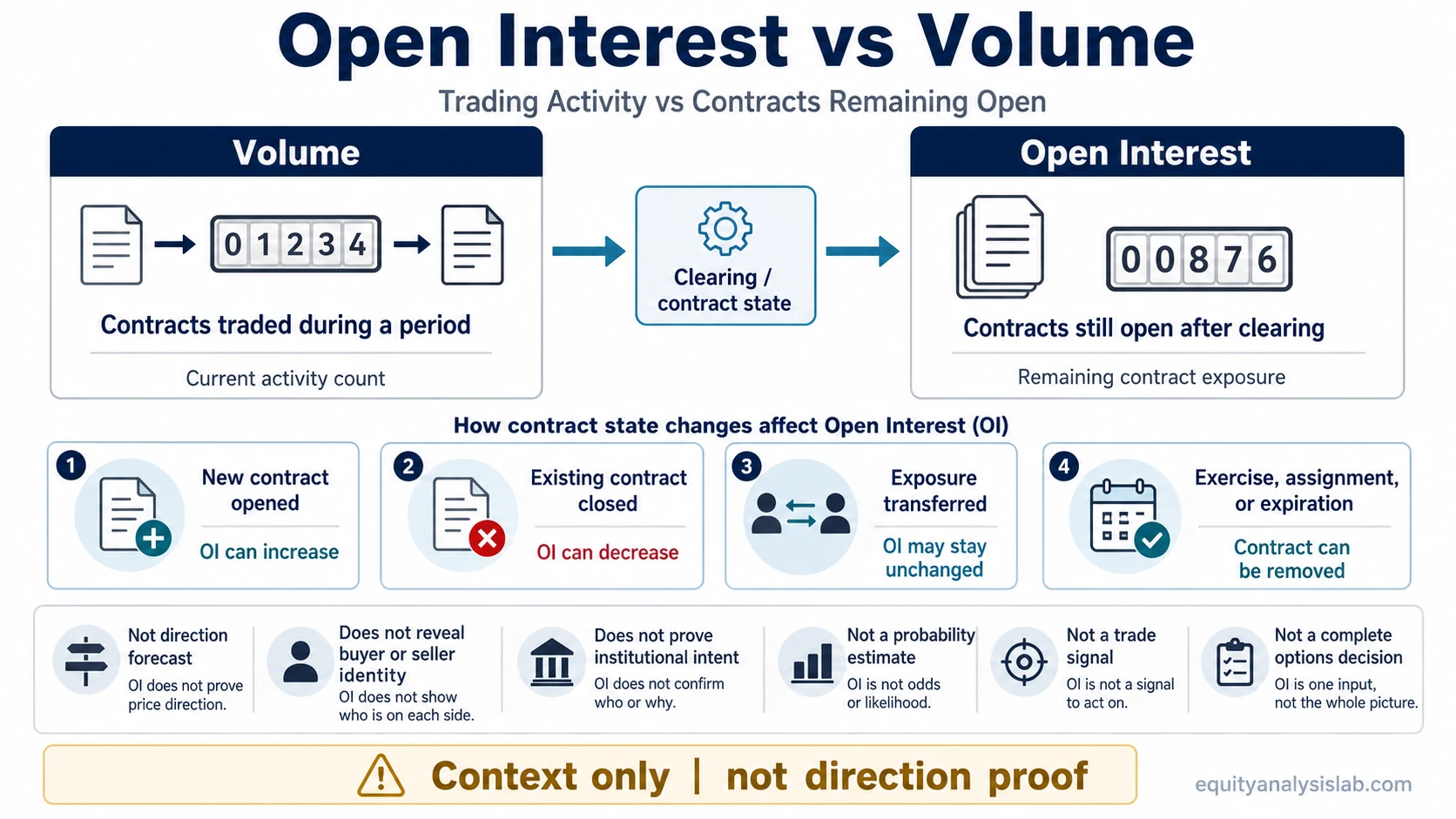

Open interest changes when option contracts are created, closed, exercised, assigned, or expire. The key distinction is whether the trade leaves a new contract open after clearing or simply transfers an existing contract from one participant to another.

| Contract activity | What happens to open interest | Why it happens |

|---|---|---|

| Opening buyer and opening seller create a new contract | Open interest increases | A new contract remains open after the trade is cleared. |

| Closing buyer and closing seller close an existing contract | Open interest decreases | An existing open contract is removed. |

| One participant opens while another closes | Open interest may stay unchanged | The contract exposure can transfer rather than create a new outstanding contract. |

| Exercise, assignment, or expiration removes the contract | Open interest decreases or goes to zero | The contract no longer remains open after the event is processed. |

Open interest is generally not the same as a live intraday activity count. Option volume can update during the trading session as transactions occur, while open interest is typically updated after clearing activity is processed. That timing difference is one reason volume and open interest can tell different stories.

Open Interest vs Volume

Open interest and volume are often shown near each other in an options chain, but they answer different questions. Volume asks how much trading occurred during a period. Open interest asks how many contracts remain open after the clearing process reflects what stayed open, what closed, and what expired or was exercised.

| Measure | What it counts | When it is useful | Main limitation |

|---|---|---|---|

| Open interest | Outstanding contracts that remain open for a specific option | Reading contract participation, liquidity context, and exposure that remains after clearing | Does not show direction, buyer identity, seller identity, or trade intent |

| Volume | Contracts traded during a period, often the current session | Reading current transaction activity and whether a contract is actively trading today | Does not prove that new open exposure remained after the activity |

| Contract state | The relationship between new positions, closed positions, transfers, exercise, assignment, and expiration | Understanding why open interest rose, fell, or stayed stable after active trading | Requires later open-interest data and cannot be fully inferred from volume alone |

Illustrative scenario: A contract can trade heavily during the session, but the next open-interest update may rise only slightly if much of that activity involved closing positions or offsetting exposure. The high volume showed activity, but the later open-interest number showed how much exposure actually remained open.

How to Read Open Interest in an Options Chain

An options-chain open-interest number is most useful when it is tied to the exact contract being reviewed. A large number beside one strike and expiration does not automatically describe the entire underlying asset. It describes outstanding contracts for that specific option.

| Options-chain field | Why it matters for open interest | Common reading error |

|---|---|---|

| Underlying | Identifies the asset linked to the option contract | Treating option open interest as a broad signal for the stock without checking contract details |

| Call or put | Separates the option type being measured | Assuming call open interest and put open interest carry the same interpretation |

| Strike price | Shows the price level attached to the contract | Reading a large strike-level number as support or resistance without additional evidence |

| Expiration date | Shows when the contract life ends | Ignoring that near-term and long-dated contracts can reflect different participation |

| Open interest | Shows how many contracts remain open after clearing effects | Treating it as real-time activity |

| Volume | Shows transaction activity during the measured period | Assuming volume automatically becomes new open interest |

Open interest can sit beside sensitivity measures, but it does not replace them. A contract with high open interest still has its own option delta, time decay, volatility exposure, and expiration risk.

What High Open Interest Can Suggest

High open interest can suggest that a contract has meaningful participation relative to nearby contracts. In some cases, higher open interest may be associated with better liquidity conditions because more participants may be active around that strike and expiration. That is a context clue, not a guarantee of tight spreads, easy execution, or favorable pricing.

High open interest can also show where contracts are concentrated across the option chain. Concentration near a strike or expiration may be relevant when investors are studying contract exposure, expiration effects, or changing sensitivity near expiration. That adjacent risk belongs closer to changing exposure near expiration than to open interest alone.

Careful interpretation: Higher open interest can show participation, but it does not tell whether the open contracts were created by bullish buyers, bearish sellers, hedgers, market makers, institutions, or retail traders. The number shows contracts that remain open, not the motive behind them.

What Open Interest Cannot Prove

Open interest does not prove direction. A large open-interest number can exist in calls or puts for many reasons, including hedging, speculation, income strategies, spreads, market-making activity, or position transfer. The number alone does not say that the underlying price should rise or fall.

Open interest does not identify who is buying or selling. The same open-interest number does not reveal whether the remaining exposure belongs to institutions, retail traders, hedgers, or liquidity providers.

Open interest does not guarantee liquidity. Higher open interest can be a useful liquidity clue, but actual fill quality also depends on bid-ask spreads, market conditions, contract demand, and execution environment.

Open interest is not a complete option decision. It can support contract analysis, but it does not replace pricing, volatility, risk exposure, expiration, position size, or portfolio context.

Expiration, Exercise, Assignment, and Contract Closure

Open interest falls when contracts stop remaining open. That can happen through closing trades, exercise, assignment, or expiration. This is why an open-interest number should be read as a current contract-state measure, not as a permanent record of past demand.

Expiration is especially important because contracts disappear when they reach the end of their life. A strike with high open interest before expiration can look very different after contracts expire, are exercised, are assigned, or are closed before the final clearing process.

When open interest is studied near expiration, it can be useful to separate the contract count from the option’s sensitivity profile. Nearby concepts such as how delta can change as the underlying price moves help explain sensitivity, while open interest shows remaining contract count.

Related Options Concepts

Open interest is best read as one part of an options-chain interpretation process. It helps describe contract participation, but adjacent concepts explain pricing, sensitivity, and expiration-related risk.

- Black-Scholes model covers the pricing-model context that open interest does not provide.

- Option delta explains price sensitivity to the underlying asset.

- Changing exposure near expiration helps separate strike concentration from risk dynamics.

- How delta can change as the underlying price moves gives more context for sensitivity around strikes.

FAQ

What does open interest mean in options?

Open interest in options means the number of contracts that remain open for a specific option contract. It is measured by contract, strike, expiration, and call or put side, not as one broad number for the entire underlying asset.

Is open interest the same as volume?

No. Volume counts contracts traded during a period, while open interest counts contracts that remain open after opening, closing, exercise, assignment, and expiration effects are processed.

Does high open interest mean an option is bullish?

No. High open interest does not prove bullish or bearish direction. It can show participation or liquidity context, but it does not reveal whether the exposure is speculative, hedging-related, institutional, retail, long, short, or part of a spread.

Can open interest rise even if price does not move much?

Yes. Open interest can rise when new contracts are opened, regardless of whether the underlying price moves sharply. Price movement, option volume, implied volatility, and open interest describe different parts of the option market.

Why can volume be high while open interest changes only slightly?

High volume shows trading activity, but some activity may close existing contracts or transfer exposure between participants. If much of the activity does not leave new contracts open after clearing, open interest may rise only slightly or stay close to unchanged.