ETF vs mutual fund tax efficiency is mainly a comparison of how two fund wrappers create, realize, and pass through taxable events. ETFs and mutual funds can expose investors to similar tax categories, but an ETF often has structural tools that reduce capital gains distributions, while a mutual fund can pass realized gains to shareholders when holdings are sold, rebalanced, or redeemed.

The difference matters most in taxable accounts. In a tax-advantaged account, the wrapper-level distinction may matter less, depending on account rules, because the account structure can defer or shield many current-year tax consequences. In a taxable brokerage account, however, fund-level distributions can affect the investor even when the investor did not sell any fund shares.

Tax rules vary by jurisdiction, so the practical comparison should be checked against the investor’s local tax rules and the fund’s own tax reporting. The mechanics below are most relevant when fund distributions create current taxable-account consequences.

Key points

- ETFs and mutual funds can face similar tax categories, but their fund mechanics can create different taxable-event patterns.

- ETF structure can reduce capital gains distributions, especially when creation and redemption activity happens in kind.

- Mutual funds can distribute realized gains to shareholders even when a shareholder keeps holding the fund.

- Account type, turnover, dividends, distribution history, costs, liquidity, and holding period all affect the practical comparison.

Why ETFs and mutual funds can be taxed differently

The basic tax categories can overlap. A fund investor may still encounter dividends, capital gains distributions, or taxes after selling shares at a gain. The wrapper difference is not that ETFs live in a separate tax universe. The difference is that ETF structure can reduce how often taxable gains are realized and distributed at the fund level.

A mutual fund is typically priced and transacted at net asset value after the market close. When shareholders redeem mutual fund shares, the fund may need to sell portfolio holdings to raise cash. If those sales realize gains, the gains can be distributed across remaining shareholders according to fund rules and tax reporting.

An ETF trades on an exchange during the day. Large creation and redemption activity is usually handled through authorized participants, and the process can often use baskets of securities rather than cash sales inside the fund. That mechanism is a central reason ETF tax efficiency can look stronger than mutual fund tax efficiency in many taxable-account comparisons.

ETF vs mutual fund tax-efficiency comparison

The cleaner comparison is not “ETF good, mutual fund bad.” It is a set of conditions that change the likelihood, timing, and visibility of taxable events.

| Comparison factor | ETF tax-efficiency angle | Mutual fund tax-efficiency angle | Investor check |

|---|---|---|---|

| Fund structure | Exchange trading and creation/redemption mechanics can reduce the need for internal taxable sales. | Shareholder redemptions can require the fund to sell holdings for cash. | Check whether the structure reduces fund-level taxable events or only changes how shares trade. |

| Turnover | Low-turnover ETFs may have fewer realized gains to distribute. | High-turnover mutual funds may realize more gains, but low-turnover index mutual funds can be relatively efficient. | Review portfolio turnover and strategy style, not only the wrapper label. |

| Capital gains distributions | Many ETFs distribute fewer capital gains because in-kind redemptions can remove appreciated positions without ordinary portfolio sales. | Mutual funds can distribute gains created by portfolio sales, rebalancing, or redemption pressure. | Look at the fund’s distribution history and tax documents. |

| Investor sale of shares | The investor may owe tax after selling ETF shares at a gain. | The investor may owe tax after selling mutual fund shares at a gain. | Separate fund-level distributions from the tax effect of your own sale. |

| Dividends | ETF dividends can still be taxable and may be ordinary or qualified depending on holdings, rules, and holding periods. | Mutual fund dividends can also be taxable and depend on the income received by the fund and shareholder context. | Do not assume the wrapper alone determines dividend treatment. |

| Taxable vs tax-advantaged account | The ETF advantage is usually more relevant in a taxable account. | Mutual fund distributions may matter less inside tax-advantaged accounts. | Match the fund wrapper question to the account type. |

| Expense ratio | A tax-efficient ETF can still be less attractive if its cost is high relative to alternatives. | A low-cost mutual fund can remain competitive when turnover and distributions are controlled. | Compare after-tax outcome together with fund costs. |

| Bid/ask spread and liquidity | ETF trading introduces spread and execution considerations. | Mutual funds avoid intraday spread costs but transact at end-of-day net asset value. | Do not treat tax efficiency as the only cost dimension. |

| Distribution history | A history of low or no capital gains distributions can support the tax-efficiency case. | A history of repeated taxable distributions can weaken the mutual fund comparison. | Use actual fund reporting rather than relying on category labels. |

| Holding period | The investor’s holding period can affect the tax treatment of gains after selling ETF shares. | The investor’s holding period can affect the tax treatment of gains after selling mutual fund shares. | Distinguish the fund’s activity from the shareholder’s own holding-period outcome. |

Why ETFs can be more tax-efficient

ETFs can be more tax-efficient because their creation and redemption process may avoid the fund selling appreciated securities for cash. When authorized participants exchange a basket of securities for ETF shares, or redeem ETF shares for a basket of securities, the fund can often manage portfolio changes without creating the same level of realized capital gains inside the fund.

This does not eliminate taxes for the investor. If the ETF pays taxable income, distributes gains, or is sold by the shareholder at a gain, taxes may still arise depending on account type and investor circumstances. The structural point is narrower: the ETF wrapper can reduce the frequency of fund-level capital gains distributions compared with many mutual funds.

The structural benefit is often clearer when the ETF is diversified, low-turnover, liquid, and able to use the in-kind process effectively. It is weaker when the fund holds assets that are harder to transfer in kind, uses strategies with higher taxable activity, or creates distributions for reasons unrelated to redemption mechanics.

Why mutual funds can create taxable distributions

Mutual funds can create taxable distributions when the fund realizes gains inside the portfolio. That can happen because the manager sells appreciated holdings, rebalances the portfolio, meets shareholder redemptions, or changes exposure. Once those gains are realized at the fund level, they may be passed through to shareholders as capital gains distributions.

The confusing part is that a shareholder can owe tax on a mutual fund distribution without selling the fund shares. The taxable event came from the fund’s portfolio activity, not from the shareholder’s own sale. That is different from the tax an investor may owe after personally selling fund shares at a gain.

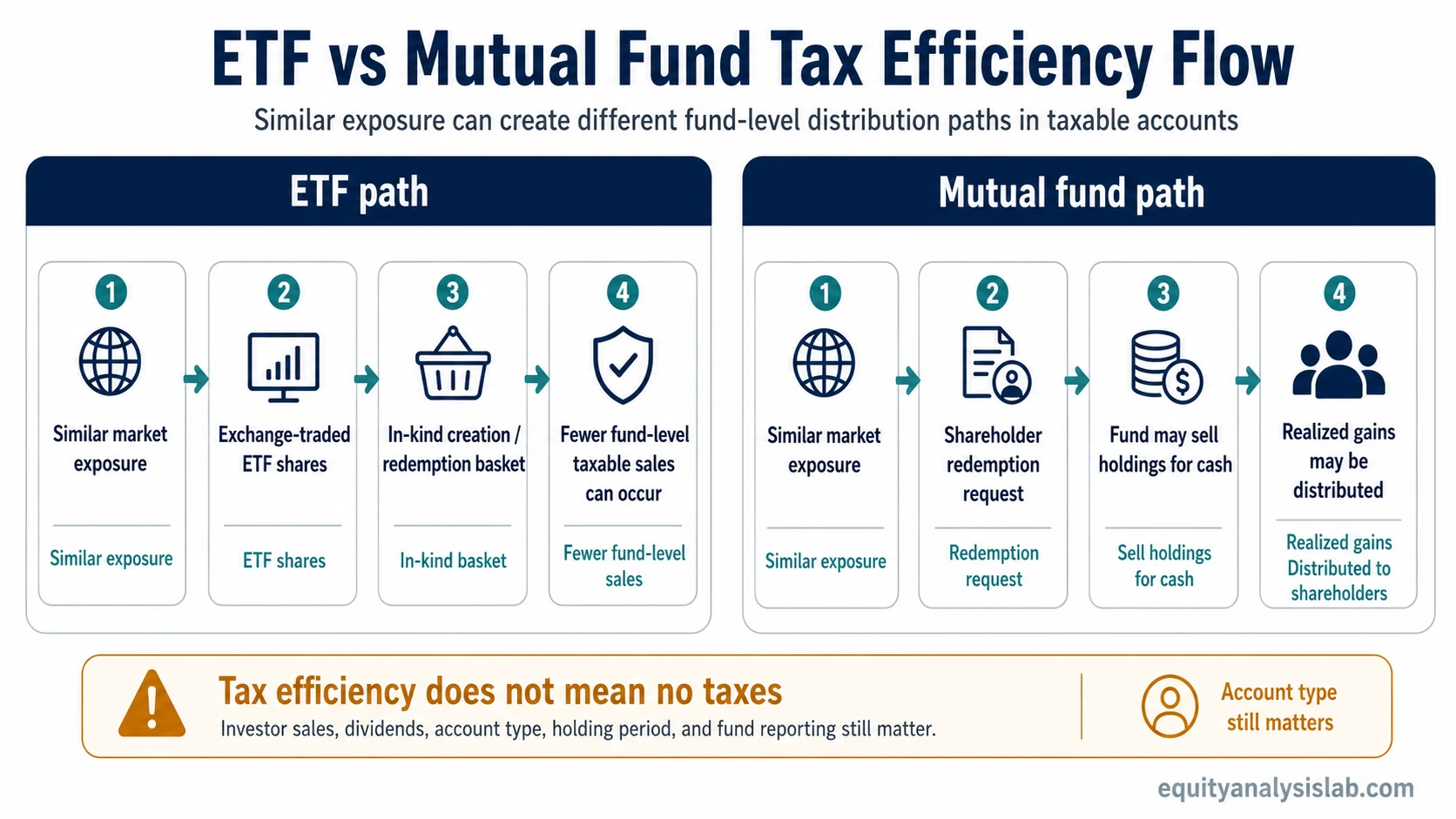

This is why two investors can own similar market exposure but experience different distribution timing. The exposure matters, but the wrapper and portfolio mechanics determine how gains are realized and distributed along the way.

Same exposure, different distribution path

Illustrative comparison:

Suppose two funds track a similar broad equity exposure. One is an ETF, and the other is a traditional mutual fund. Both funds hold many of the same underlying stocks, and both shareholders keep their positions through the year.

If some investors redeem from the mutual fund, the fund may need to sell appreciated holdings to raise cash. Those sales can realize gains inside the fund, and those gains may later be distributed to shareholders who never sold their shares.

If the ETF handles large redemptions through an in-kind process, appreciated securities may leave the fund through the redemption basket rather than through taxable cash sales inside the portfolio. The ETF shareholder still owns market exposure and can still owe tax in other situations, but the fund-level taxable distribution path may be different.

The lesson is not that the ETF always produces a better after-tax result. The lesson is that similar exposure does not guarantee similar tax-event timing. Wrapper mechanics can change whether the investor mainly faces tax after selling shares, through fund distributions, or through both.

When the ETF tax advantage can be smaller

The ETF advantage can be smaller when the mutual fund is already low-turnover, index-based, and careful about realizing gains. Some index mutual funds can be relatively tax-efficient because they trade less, track broad benchmarks, and avoid frequent taxable portfolio changes.

Account type can also shrink the practical difference. Inside tax-advantaged accounts, current-year capital gains distributions may not affect the investor the same way they do in a taxable brokerage account. In that setting, expense ratio, tracking quality, trading access, and fund availability may matter more than wrapper tax mechanics.

Dividends remain a separate caveat. ETF dividends are not automatically tax-free or automatically qualified because the fund is an ETF. Dividend treatment depends on the income source, fund reporting, shareholder holding period, and account context.

Trading costs can also matter. An ETF with a wide bid/ask spread, weak liquidity, or poor execution may give back part of the practical benefit that appears from tax structure alone. Tax efficiency is one input in fund selection, not the full decision.

Common tax-efficiency mistakes

| Mistake | Cleaner interpretation |

|---|---|

| Treating tax efficiency as no taxes | An ETF can still create taxable income, taxable distributions, or taxable gains when the shareholder sells. |

| Assuming every ETF is better than every mutual fund | Low-turnover index mutual funds can be close to ETFs in practical tax efficiency. |

| Ignoring account type | The comparison is usually more important in taxable accounts than in tax-advantaged accounts. |

| Confusing fund distributions with investor sales | A fund-level capital gains distribution is different from the investor selling fund shares at a gain. |

| Looking only at taxes | Expense ratio, tracking difference, liquidity, bid/ask spread, and portfolio fit still belong in the fund comparison. |

How to compare tax efficiency before choosing a wrapper

A practical comparison starts with account location. If the fund will sit in a taxable account, capital gains distribution history and turnover deserve closer attention. If the fund will sit in a tax-advantaged account, wrapper-level tax efficiency may be less important than cost, access, and portfolio role.

| Question to check | Why it matters |

|---|---|

| Will the fund sit in a taxable account? | Taxable accounts make fund-level distributions and shareholder gains more visible. |

| Does the fund have high turnover? | Higher turnover can create more realized gains inside either wrapper. |

| What is the capital gains distribution history? | Actual distributions show more than wrapper labels alone. |

| Does the ETF trade with tight spreads and enough liquidity? | Trading friction can affect the practical comparison even when tax mechanics are favorable. |

| Are dividends a major part of expected return? | Dividend taxation can matter separately from capital gains distribution efficiency. |

| Is the mutual fund low-turnover and index-based? | Some mutual funds can be relatively tax-efficient when portfolio activity is limited. |

ETF tax efficiency vs fund selection

Tax efficiency should not be isolated from the rest of the fund decision. A fund can have attractive tax mechanics and still be a weak fit if its exposure, cost, liquidity, tracking quality, or portfolio role does not match the investor’s objective.

The comparison should start with exposure. If the ETF and mutual fund do not track the same market, strategy, or holdings profile, the tax-efficiency comparison becomes secondary. A more tax-efficient wrapper does not fix the wrong exposure.

After exposure, review structure, cost, distribution history, turnover, liquidity, and account context together. That sequence keeps tax efficiency in the right place: important for taxable-account ownership, but not a standalone fund-selection rule.

Bottom line

ETFs are often more tax-efficient than mutual funds in taxable accounts because in-kind creation and redemption mechanics can reduce fund-level capital gains distributions. Mutual funds can be less tax-efficient when portfolio turnover, rebalancing, or shareholder redemptions create realized gains that pass through to remaining shareholders.

The better investor question is narrower: in this account, with this fund strategy, this turnover profile, this distribution history, and these costs, which wrapper produces the cleaner after-tax ownership path? That framing keeps the comparison useful without pretending that tax efficiency alone decides the best fund.

FAQ

Are ETFs always more tax-efficient than mutual funds?

No. ETFs often have structural tax-efficiency advantages, but the result depends on the fund strategy, turnover, holdings, distribution history, account type, and investor behavior. A low-turnover index mutual fund can be relatively tax-efficient.

Can I owe tax on a mutual fund if I did not sell shares?

Yes, in a taxable account. A mutual fund can pass through realized capital gains from portfolio sales, rebalancing, or redemption-related activity. That distribution can affect shareholders even if they did not sell their own fund shares.

Can I owe tax on an ETF?

Yes. An ETF can pay taxable dividends, make taxable distributions, or create a taxable gain when the shareholder sells ETF shares above their cost basis. Tax efficiency reduces some taxable-event pressure; it does not eliminate taxes.

Does tax efficiency matter inside a retirement account?

It may matter less than it does in a taxable account because the account structure can defer or shield many current tax effects. In that setting, cost, liquidity, exposure, tracking quality, and portfolio fit may become more important comparison factors.