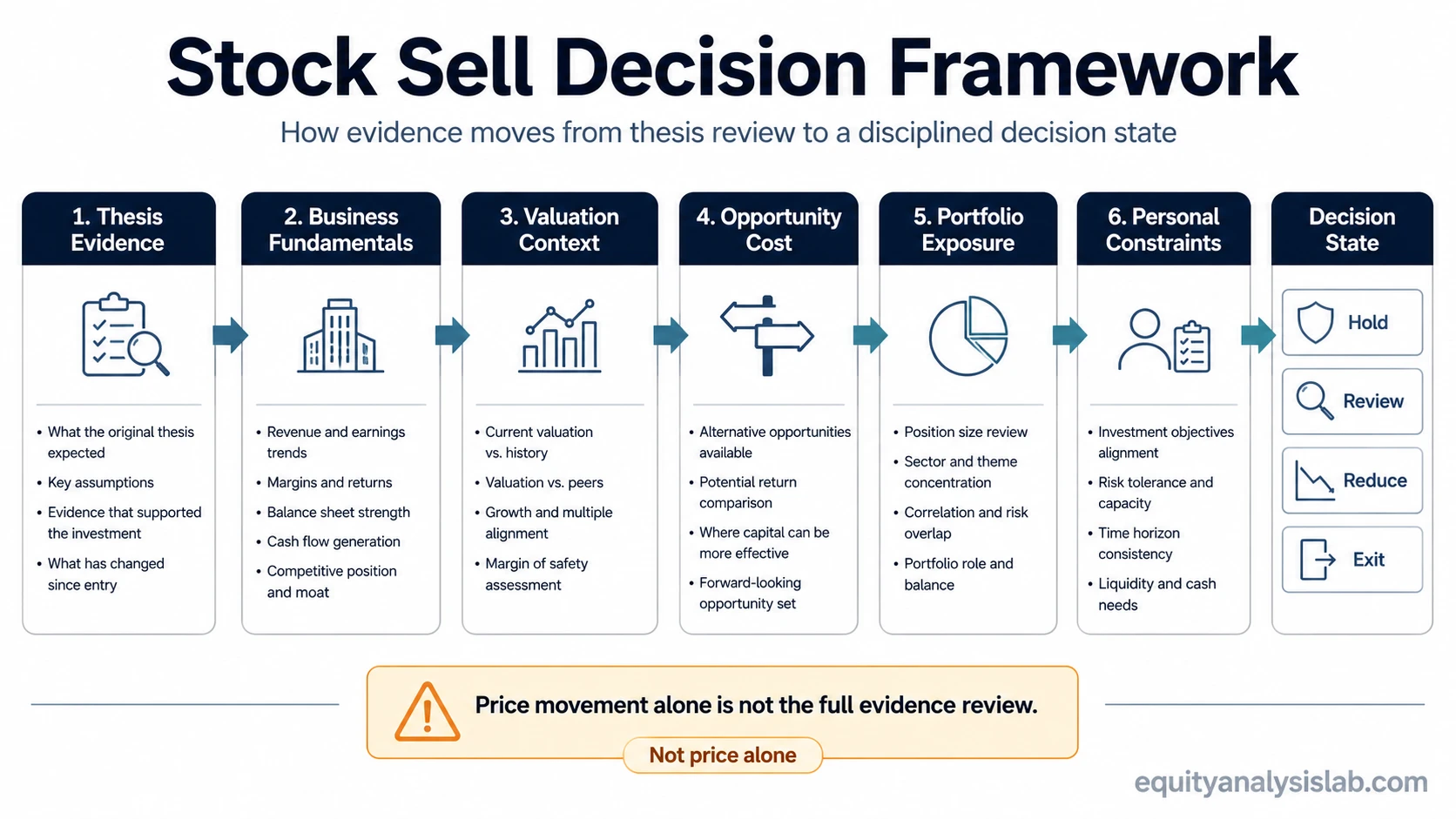

Knowing when to sell a stock starts with evidence, not with price movement alone. The useful question is whether the original reason for owning the company still holds after reviewing thesis evidence, business fundamentals, valuation context, opportunity cost, portfolio exposure, and personal constraints.

Price can rise while the business case weakens. Price can fall while the long-term case remains intact. A disciplined sell process separates market movement from evidence change, then decides whether the position belongs in a hold, review, reduce, or exit state.

Key Points

- A sell decision is a conditional review of evidence, not an automatic reaction to a gain or loss.

- The strongest reasons to reconsider a stock usually involve thesis damage, weaker fundamentals, valuation pressure, opportunity cost, portfolio concentration, or personal constraints.

- A checklist can organize the review, but it cannot replace judgment about business quality, valuation assumptions, or portfolio role.

- Hold, review, reduce, and exit are different decision states. Treating every concern as a full-sale decision can create avoidable mistakes.

The stock sell framework

The first step is to compare current evidence against the original investment thesis. If the company still fits the reason it was owned, a price move alone may not be enough to justify a sale. If the evidence now contradicts the thesis, the position deserves a deeper review.

The framework works best as a sequence. Start with the business case, then move to financial evidence, valuation, alternatives, portfolio exposure, and constraints. That order helps prevent a common mistake: making the sell decision about recent emotion before checking whether the underlying evidence has actually changed.

| Framework component | What to check | What it can indicate | What it cannot prove |

|---|---|---|---|

| Thesis evidence | Whether the original reason for ownership still matches current business evidence | The position may still have a valid research basis or may need review | It cannot prove that the stock is cheap, safe, or about to recover |

| Fundamentals | Revenue quality, margins, cash flow, balance-sheet risk, competitive position, and management execution | The business may be improving, weakening, or changing character | It cannot remove valuation risk or portfolio concentration risk |

| Valuation context | Whether price is still reasonable compared with fair value, assumptions, and scenario range | The expected return may have narrowed or the downside may have increased | It cannot produce a mechanical sell signal by itself |

| Opportunity cost | Whether capital is tied to a weaker idea while stronger evidence exists elsewhere | The stock may no longer be the best use of limited portfolio capital | It cannot justify constant switching without a clear process |

| Portfolio exposure | Position size, concentration, correlation, and role inside the portfolio | The investment may create more portfolio risk than intended | It cannot decide whether the company itself is fundamentally impaired |

| Personal constraints | Cash needs, time horizon, risk capacity, and tax boundaries | The right portfolio action may differ from the pure company-analysis answer | It cannot replace personal tax, legal, or financial advice |

Reasons to consider selling a stock

A sell review becomes more serious when the evidence changes in a way that damages the reason for ownership. The cleanest cases are not based on discomfort alone. They usually involve a visible break between the original thesis and the company’s current facts.

The thesis no longer holds: The company may no longer match the assumptions that supported ownership. A growth thesis, turnaround thesis, capital-allocation thesis, or quality thesis can weaken when the evidence no longer supports the original logic.

Fundamentals deteriorate: Weaker margins, lower cash conversion, rising leverage, poor execution, declining competitive position, or repeated earnings-quality issues can change the business case.

Valuation no longer compensates for risk: A stock can remain a good company while becoming less attractive if price moves far beyond fair value or if the assumptions needed to justify the price become too aggressive.

Opportunity cost rises: A position may deserve review if capital is tied to a weaker idea while another researched idea has stronger evidence, better valuation support, and a clearer risk boundary.

Portfolio risk changes: A successful stock can become too large relative to the intended portfolio role. In that case, position sizing, concentration, and correlation may matter as much as the company thesis.

Personal constraints change: A cash need, shorter time horizon, lower risk capacity, or tax boundary can change the acceptable exposure level. Tax and legal questions require separate professional review.

Reasons not to sell a stock by themselves

Many weak sell decisions start with a real feeling but incomplete evidence. A price move can create pressure, but pressure is not the same as a broken thesis.

| Trigger | Why it feels persuasive | Why it is incomplete |

|---|---|---|

| The stock is down | A loss creates discomfort and urgency | The decline may be noise unless the business case, valuation support, or portfolio role has changed |

| The stock is up | A gain feels like something that should be protected | A gain alone does not prove the thesis is finished or the valuation is unreasonable |

| Short-term commentary changes | News and opinion can make recent movement feel more meaningful | Commentary can shift faster than business evidence |

| A macro forecast changes | Broad market narratives can affect confidence | A macro view does not automatically decide a company-level investment case |

| A mechanical rule is triggered | Rules can feel objective and clean | A single rule can ignore thesis quality, valuation, portfolio role, and constraints |

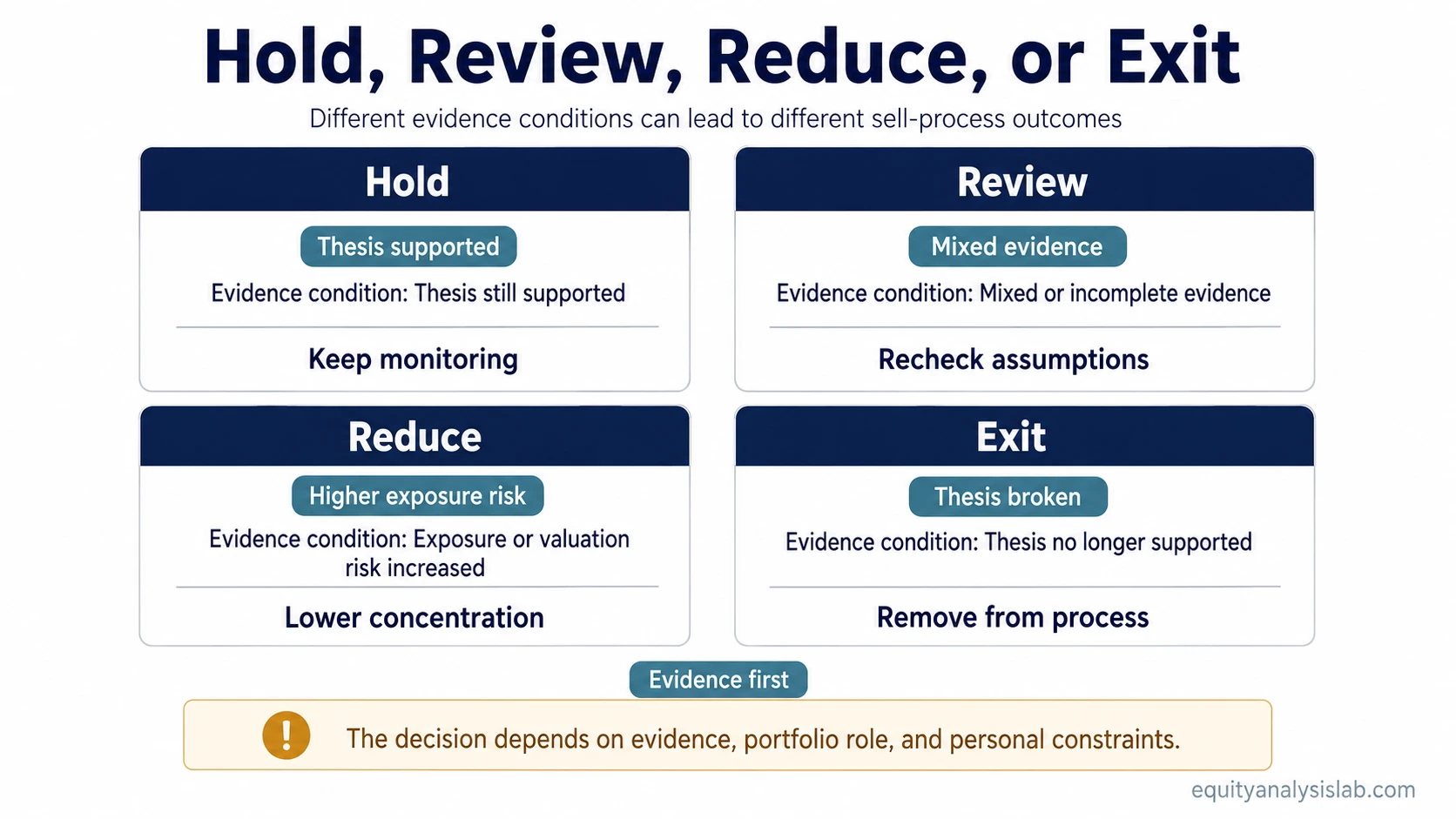

Decision states: hold, review, reduce, or exit

A sell process does not need to treat every concern as an all-or-nothing decision. The decision state should match the strength of the evidence and the role of the position.

| Decision state | When it may fit | What to avoid |

|---|---|---|

| Hold | The thesis remains intact, fundamentals still support the case, valuation is acceptable, and portfolio exposure is intentional | Holding only because selling feels difficult |

| Review | Evidence is mixed, new information needs interpretation, or the position has moved away from its original role | Calling review a decision when it is only a delay |

| Reduce exposure | The thesis still has support, but valuation, concentration, risk capacity, or opportunity cost has changed | Reducing without knowing which risk is being controlled |

| Exit | The thesis is broken, fundamentals have changed materially, valuation no longer compensates for risk, or the position no longer fits the portfolio | Exiting only because the recent price move feels uncomfortable |

Evidence checklist with limits

A checklist can slow down emotional decisions and make the review more complete. It should not be treated as a formula that produces an automatic answer. Each item only tells where to look; judgment still matters.

| Checklist area | Evidence question | Why it matters | Limit |

|---|---|---|---|

| Original thesis | What had to be true for the stock to deserve ownership? | Sell discipline starts by comparing current facts with thesis evidence | A thesis can be incomplete, biased, or outdated |

| Business quality | Has the competitive position, pricing power, customer base, or capital allocation changed? | Business deterioration can matter more than short-term price action | One data point may be noise rather than a durable change |

| Financial statements | Are margins, cash flow, leverage, dilution, or earnings quality moving against the thesis? | Financial evidence can confirm or contradict the narrative | Accounting data needs context across periods and peers |

| Valuation | Does the current price still make sense against estimated intrinsic value and scenario assumptions? | Valuation defines whether expected return still compensates for risk | Valuation estimates are sensitive to growth, margin, discount-rate, and multiple assumptions |

| Risk buffer | Has the margin of safety narrowed enough to change the decision boundary? | A smaller buffer can reduce tolerance for bad news | A margin of safety is an estimate, not a guarantee |

| Portfolio role | Does the position still serve the intended role inside the portfolio? | A stock can be fundamentally sound but too large, too correlated, or no longer aligned with objectives | Portfolio fit does not prove business quality |

| Constraints | Have cash needs, time horizon, risk capacity, or tax boundaries changed? | Personal constraints can change the acceptable exposure level | Tax and legal questions require separate professional review |

Checklist limit: A checklist can organize evidence, but it cannot make the decision safe by itself. Weak thesis quality, fragile valuation assumptions, or concentrated exposure can still create risk even when several checklist items appear acceptable.

A compact stock sell-decision scenario

Consider a generic company that was originally owned because it had durable revenue growth, improving margins, and a valuation that left room for a reasonable return. After several reporting periods, revenue still grows, but margins weaken, cash conversion falls, and management begins relying on more aggressive assumptions to defend the outlook.

The stock price alone does not answer the sell question. If valuation is still moderate and the margin issue looks temporary, the position may belong in review. If the valuation already assumes strong margin recovery and the portfolio position has become large, reducing exposure may be more consistent with the evidence. If the original thesis depended on margin expansion and the new evidence contradicts that assumption, exit becomes easier to justify as a research conclusion rather than a reaction to price.

Where sell decisions often fail

Sell decisions often fail when the process starts with the desired action and then looks for evidence afterward. That can happen after a fast gain, a sharp decline, a tax concern, or a persuasive market narrative.

A stronger process keeps the order reversed. Evidence comes first, then interpretation, then decision boundary. That is where investment discipline matters: the goal is not to avoid every mistake, but to avoid letting emotion, hindsight, or a single metric control the whole decision.

FAQ

How do you know when to sell a stock?

The decision becomes more defensible when current evidence no longer supports the original thesis, fundamentals have deteriorated, valuation no longer compensates for risk, or the position no longer fits portfolio constraints. Price movement alone is not enough.

Is a falling stock always a reason to sell?

No. A falling price may justify a review, but the important question is whether the decline reflects thesis damage, weaker fundamentals, poorer valuation support, or a portfolio risk that no longer fits.

Is a rising stock always a reason to take profits?

No. A rising price may reduce future return potential or create concentration risk, but it does not automatically mean the business case is finished. Valuation, thesis quality, and portfolio exposure still matter.

Can a checklist tell you exactly when to sell?

A checklist can organize the review, but it cannot tell you exactly when to sell. The final interpretation still depends on thesis quality, financial evidence, valuation assumptions, portfolio role, and constraints.