Portfolio concentration risk is the risk that a portfolio depends meaningfully on one holding, issuer, sector, geography, asset class, fund, currency, or overlapping exposure group.

A high concentration reading is not a standalone verdict. It does not prove that a holding is low quality, that future returns will be poor, or that an immediate portfolio action is required. It shows where portfolio results may be more dependent on a smaller set of exposures than the holding count alone suggests.

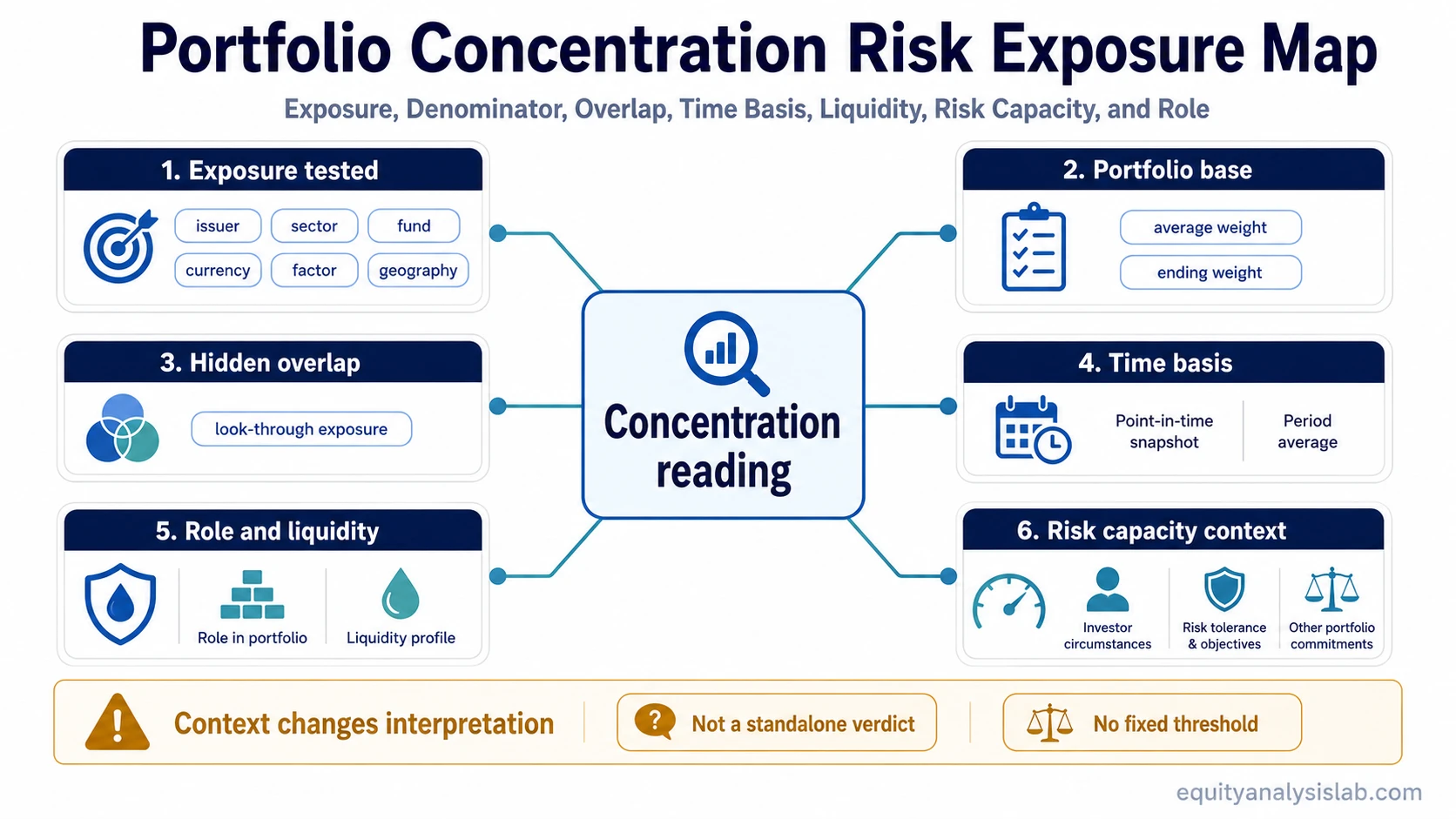

Definition: Portfolio concentration risk is a diagnostic exposure reading that compares a specific exposure group with the portfolio base used to measure it. The reading becomes useful only when the numerator, denominator, time period, overlap, liquidity, and portfolio role are understood together.

Key Points

- Portfolio concentration risk measures exposure dependence, not investment quality by itself.

- The same percentage can carry different meaning depending on the holding’s role, liquidity, time horizon, and risk capacity.

- Hidden overlap can make a portfolio more concentrated than the number of holdings suggests.

- Measurement basis matters because beginning weight, ending weight, average weight, and look-through exposure can produce different readings.

What Portfolio Concentration Risk Measures

Portfolio concentration risk measures how much of a portfolio’s outcome is tied to a defined exposure. That exposure may be a single stock, an employer stock position, a sector, a country, a currency, a commodity-linked group, a fund, a business model, or a factor such as growth, value, duration sensitivity, or credit sensitivity.

The broader concept of portfolio concentration describes the condition itself. Portfolio concentration risk focuses on the interpretation problem: how much dependence exists, where it comes from, and whether the exposure is intentional, drifted, hidden, or misunderstood.

A portfolio can look diversified by holding count while still depending on a narrow driver. Ten holdings across different tickers may still share the same revenue sensitivity, valuation factor, interest-rate exposure, geography, or customer cycle. The risk reading improves when the investor looks through labels and asks what actually drives the holdings together.

How the Measurement Works

The basic measurement starts with a numerator and a denominator. The numerator is the exposure being tested. The denominator is the portfolio base used for comparison. A simple single-position reading may compare one holding’s market value with total portfolio value. A broader reading may combine several holdings that share the same sector, country, factor, currency, or economic driver.

The same number can mean different things if the denominator changes. A position may be 12% of an equity sleeve, 8% of the full investment portfolio, and 5% of total liquid assets. None of those readings is automatically wrong, but each answers a different question.

| Measurement input | Question it answers | Why it changes interpretation |

|---|---|---|

| Single holding weight | How much depends on one issuer? | A large position can dominate results even if the rest of the portfolio is broadly spread. |

| Sector or industry weight | How much depends on one business cycle? | Several separate holdings can still react to the same earnings cycle, regulation, commodity price, or valuation pressure. |

| Fund look-through exposure | What exposures exist inside pooled vehicles? | Two funds may hold different names while still leaning on the same mega-cap, sector, country, or factor exposure. |

| Geography or currency exposure | How much depends on one region or currency regime? | Revenue source, listing location, and reporting currency may not tell the same story. |

| Average versus ending weight | Was the exposure persistent or temporary? | A year-end weight can miss a large exposure that existed for most of the period, while an average can smooth a recent drift. |

| Portfolio sleeve versus total assets | Which portfolio base is being tested? | An exposure can look large inside one sleeve but smaller across the full portfolio, or the reverse if the sleeve carries most of the relevant risk. |

Why the Same Concentration Reading Can Mean Different Things

A concentration reading needs context before it becomes useful. A large holding that is liquid, intentionally sized, well understood, and matched to the portfolio’s time horizon is different from a large holding that grew by drift, became hard to sell, or duplicates exposure already present elsewhere.

The role of the position matters. A core holding, a satellite holding, an inherited position, an employer-linked position, and a temporary cash substitute do not carry the same interpretation. The number may be similar, but the reason for the exposure and the consequence of being wrong can differ sharply.

Liquidity also changes the reading. Concentration in an easily traded large-cap instrument is not the same as concentration in an illiquid security, private investment, thinly traded fund, or restricted position. Liquidity does not remove concentration risk, but it affects how flexible the portfolio may be if circumstances change.

Broader asset allocation context matters as well. A stock position can look large in isolation but may be part of a deliberate equity sleeve, while a smaller position can still matter if it duplicates risks already present across funds, sectors, or correlated assets.

Common Mistake: Treating Concentration as a Standalone Verdict

Not this: A high concentration reading automatically means the portfolio is poorly built, too risky, or in need of action.

Instead: A concentration reading identifies where portfolio dependence is located. The next question is whether that dependence is intentional, understood, liquid enough, aligned with the investor’s time horizon, and consistent with the rest of the portfolio structure.

The opposite mistake is also common. A low single-position weight does not automatically mean the portfolio is well diversified. If many holdings depend on the same sector, same valuation style, same country, same currency, or same economic driver, the portfolio can still carry meaningful concentration beneath the surface.

Concentration risk is therefore a diagnostic, not a command. It is most useful when it separates exposure awareness from action. The measurement can reveal a question that deserves review without answering what the investor should do next.

How Hidden Overlap Can Increase Portfolio Concentration

Hidden overlap appears when holdings look separate but respond to the same underlying driver. A portfolio may own several funds, individual stocks, and sector exposures that all rely on the same large companies, same region, same factor, or same earnings cycle.

Holding count can create false comfort in this situation. Twenty holdings may still leave the portfolio dependent on a small set of business models or market conditions. The practical question is not only “how many holdings are there?” but “which risks are repeated?”

That is where exposure spread becomes more important than label count. A portfolio can include different tickers yet still lack meaningful diversified exposure if the holdings move for similar reasons.

Portfolio concentration risk example: A hypothetical portfolio has 18 holdings. The largest single holding is 9%, so no individual position appears dominant at first glance. After grouping the holdings by business driver, several technology funds and individual stocks create a combined 38% exposure to the same growth-stock factor and a small group of overlapping large-cap issuers. The more useful reading is not only the 9% single-position weight. It is the combined dependence on the same driver, measured against the relevant portfolio base.

How Measurement Basis Can Distort the Reading

Portfolio concentration risk can be overstated or understated when the measurement basis is unclear. A point-in-time reading may capture the portfolio only on one date. An average reading may better describe the exposure carried across a period, but it can smooth recent changes. A look-through reading may be more useful for funds, but it requires enough transparency into the underlying holdings.

Peer comparison can also mislead. A concentrated portfolio, a broad index portfolio, a thematic fund, a family portfolio, and a retirement account may have different constraints and purposes. A concentration number from one structure should not be treated as a universal benchmark for another.

Time horizon matters because exposure dependence is not experienced the same way over every holding period. A portfolio built around a long-term thesis may tolerate a different kind of exposure than a portfolio intended to fund near-term cash needs. That does not make concentration harmless. It means the interpretation must connect the number with the portfolio’s role.

Risk capacity also changes the reading because the same exposure can be easier or harder to absorb depending on liquidity, cash needs, income stability, and how much of the portfolio depends on the same driver.

How to Read Portfolio Concentration Risk Without Overreacting

A useful reading starts with the exposure being measured. The first question is whether the concentration is single-name, sector, industry, geography, currency, fund, factor, customer, liquidity, or business-model exposure. A vague “concentration is high” statement is less useful than a precise statement about what the portfolio depends on.

The next question is whether the exposure is intentional or accidental. Intentional concentration can still carry risk, but it is different from concentration created by price drift, fund overlap, employer exposure, inheritance, or repeated exposure inside different wrappers.

The final question is whether the measurement matches the decision being reviewed. A single-stock reading can help identify issuer dependence. A sector reading can identify economic-cycle dependence. A look-through fund reading can identify overlap that is not visible from the fund names alone. A liquidity reading can show whether the portfolio has flexibility if assumptions change.

Interpretation note: Portfolio concentration risk becomes more useful when it names the exposure, defines the measurement base, identifies whether overlap is visible or hidden, and separates diagnostic review from action advice.

FAQ

Is portfolio concentration risk always bad?

No. Portfolio concentration risk identifies exposure dependence. The same reading can be intentional, accidental, liquid, illiquid, temporary, persistent, understood, or misunderstood. The number needs context before it can be interpreted.

Can a portfolio with many holdings still have concentration risk?

Yes. Many holdings can still share the same sector, issuer overlap, country, currency, factor, or business driver. Holding count alone does not prove that exposure is spread across different sources of risk.

What makes a concentration-risk reading more useful?

The reading becomes more useful when it states the exposure being measured, the denominator used, the time period, whether the value is average or ending weight, and whether hidden overlap is included.