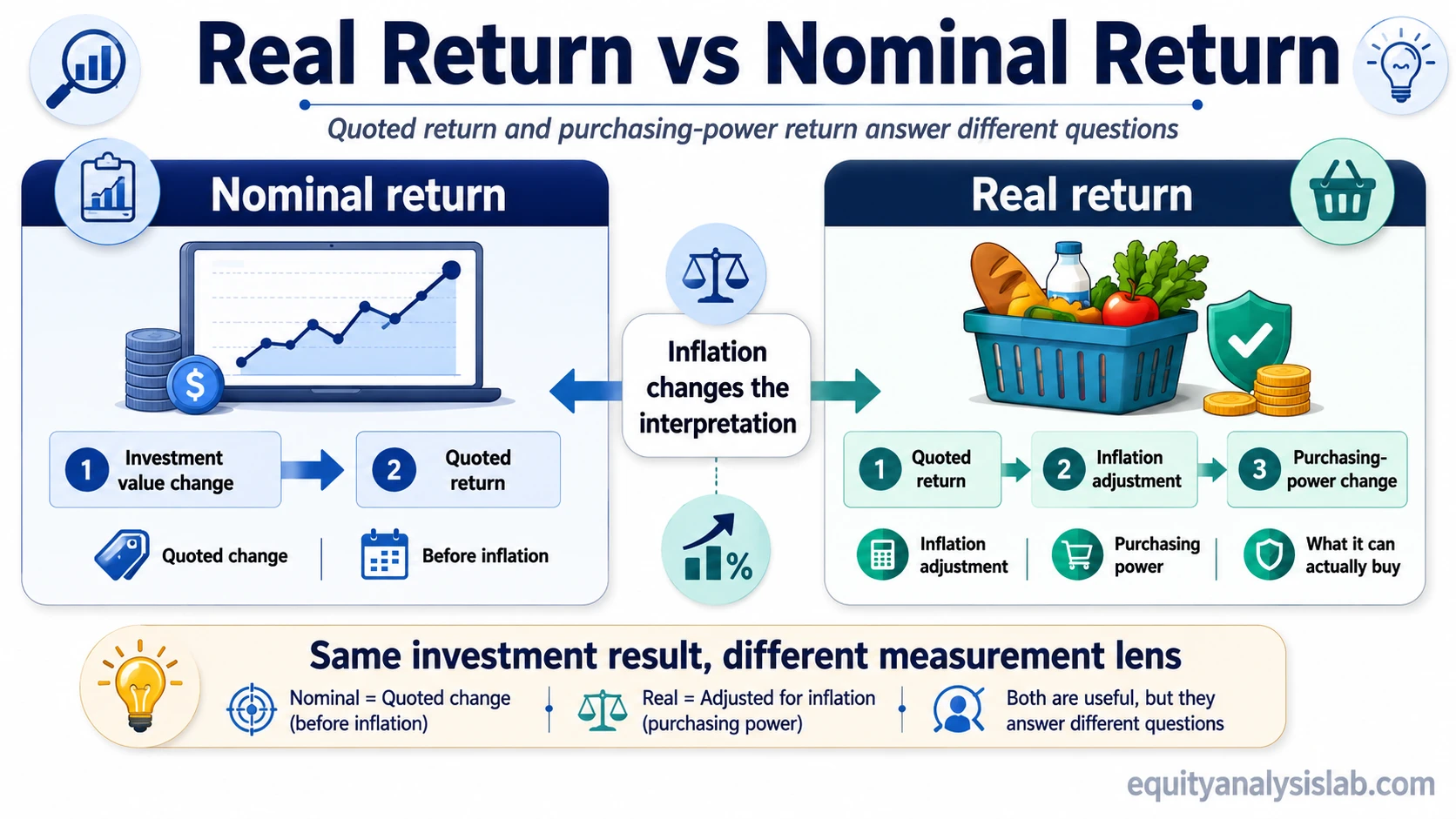

Nominal return is the quoted return before adjusting for inflation. Real return adjusts that return for inflation, so it shows whether purchasing power increased or decreased.

The distinction matters because the same portfolio can show a positive nominal return while delivering a weaker or even negative real return if prices rose faster than the investment value.

Nominal return answers: how much did the investment value change before inflation?

Real return answers: how much purchasing power remained after inflation is considered?

What is the difference between real return and nominal return?

The difference is the inflation adjustment. Nominal return measures the stated percentage gain or loss. Real return translates that gain or loss into purchasing-power terms.

This is why nominal vs real returns should not be treated as interchangeable labels.

A nominal return can look positive while the real return is weak if inflation absorbed most of the gain. A real return can also be positive when the investment grew faster than the general price level. These measures are connected, but they do not answer the same investor question.

Real return vs nominal return comparison

The cleanest way to separate the two measures is to ask what each one is measuring before using it in an investment discussion.

The false equivalence is treating a quoted gain and a purchasing-power gain as the same result.

| Criteria | Nominal return | Real return |

|---|---|---|

| What it measures | The quoted change in investment value. | The change in purchasing power after inflation. |

| Inflation treatment | Does not adjust for inflation. | Adjusts the return for inflation. |

| Investor question | What did the account value or quoted return do? | Did the investment outpace the rise in prices? |

| Formula role | Usually the starting number. | Uses nominal return and inflation to estimate purchasing-power change. |

| When it is useful | Reading reported returns, account statements, quoted yields, or performance summaries. | Comparing economic progress after inflation, especially over longer horizons. |

| Main limitation | Can overstate economic progress when inflation is high. | Does not prove investment quality by itself. |

Nominal return definition

Nominal return is the return before inflation adjustment. If an investment rises from 100 to 108, the nominal return is 8% before considering what happened to prices in the wider economy.

This makes nominal return useful for seeing the quoted gain or loss, but it does not show whether the investor gained purchasing power. It is the visible return number, not the complete economic interpretation.

Real return definition

Real return is the inflation-adjusted return. It estimates how much purchasing power changed after the nominal return is compared with inflation.

A simple approximation is:

Real return ≈ nominal return − inflation

The exact formula is:

Real return = ((1 + nominal return) / (1 + inflation rate)) − 1

The approximate formula is usually enough for a quick interpretation. The exact formula matters more when precision is needed, but the investor question is the same: did the investment increase purchasing power after inflation?

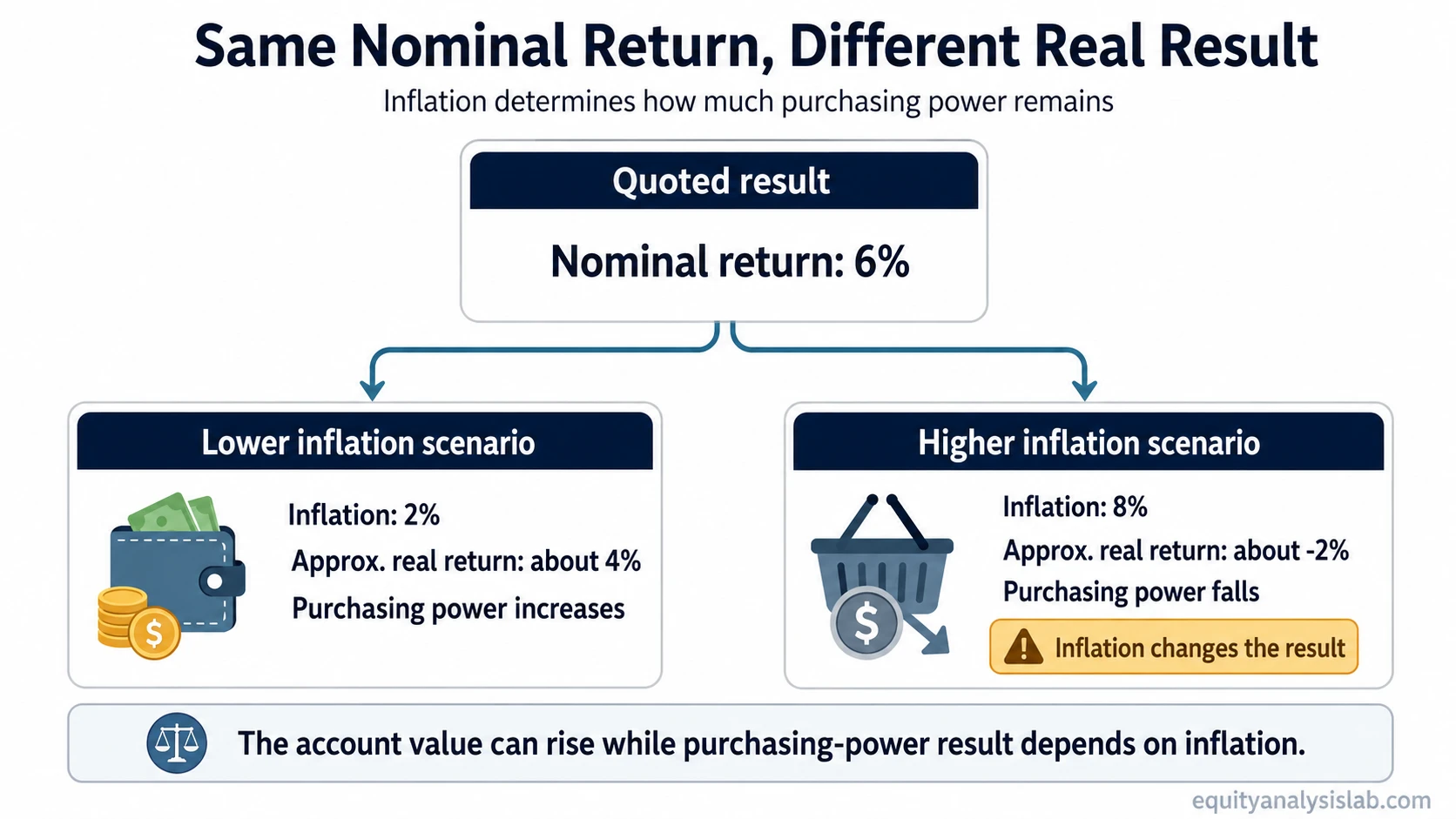

Example: same nominal return, different purchasing-power result

A portfolio can gain 6% in quoted value while inflation determines how much of that gain remains in purchasing-power terms. The nominal return is 6% because the portfolio value increased before inflation is considered.

If inflation over the same period is 2%, the approximate real return is about 4%. The investor gained purchasing power.

If inflation over the same period is 8%, the approximate real return is about -2%. The portfolio value still rose in quoted terms, but purchasing power fell.

The same quoted gain can therefore answer two different questions: account value rose, but purchasing power depends on inflation.

Why nominal return can mislead

The common mistake is treating a positive nominal return as proof of economic progress. A quoted gain is not the same as a purchasing-power gain.

That does not make nominal return useless. It is still the starting point for reported performance, quoted return figures, and many valuation inputs. The problem appears when the nominal number is used as if inflation did not exist.

The opposite mistake is treating real return as a complete investment-quality test. Real return adjusts for inflation, but it does not replace business analysis, valuation work, taxes, fees, liquidity needs, or risk assessment.

When to use each measure

Nominal and real return are best understood as different measurement lenses. The right lens depends on the question being asked.

| Investor question | More relevant measure | Reason |

|---|---|---|

| What return was quoted or reported? | Nominal return | Most reported return numbers are shown before inflation adjustment. |

| Did purchasing power increase? | Real return | Inflation determines how much of the quoted gain remains economically meaningful. |

| How should future assumptions be interpreted? | Both | An expected return assumption should be clear about whether it is nominal or inflation-adjusted. |

| How should yield-like valuation inputs be read? | Usually nominal first, then inflation context | A metric such as earnings yield may be quoted in nominal terms, but the investor may still compare it with inflation and required return assumptions. |

| Does the investment offer an attractive tradeoff? | Neither measure alone | Return labels do not replace broader risk and return analysis. |

What real return does not prove

Real return is useful because it adjusts for inflation, but it should not be treated as a full investment verdict.

A positive real return does not automatically mean an investment was attractive. The investor still has to consider the risk taken, the time horizon, taxes, fees, liquidity needs, valuation context, and whether the result was repeatable or unusual.

A negative real return also needs context. It may reflect high inflation, a weak investment outcome, a short measurement window, or a period where purchasing power was difficult to preserve across many assets. The label identifies the purchasing-power result; it does not explain every cause.

Related concepts

Real and nominal return become more useful when they are connected to the investor’s broader return framework. Expected return helps clarify whether assumptions are quoted before or after inflation. Earnings yield can show how a valuation-based return input is being interpreted. Risk and return analysis keeps the inflation-adjusted result from being treated as a standalone decision rule.

FAQ

Can nominal return be positive while real return is negative?

Yes. If the investment return is positive but inflation is higher than that return, the nominal return can be positive while the real return is negative.

Is real return the same as inflation-adjusted return?

Yes. Real return is the return after adjusting for inflation, so it is commonly described as inflation-adjusted return.

Is real return always more useful than nominal return?

No. Real return is better for purchasing-power questions, while nominal return is useful for quoted performance and reported return figures. They answer different questions.