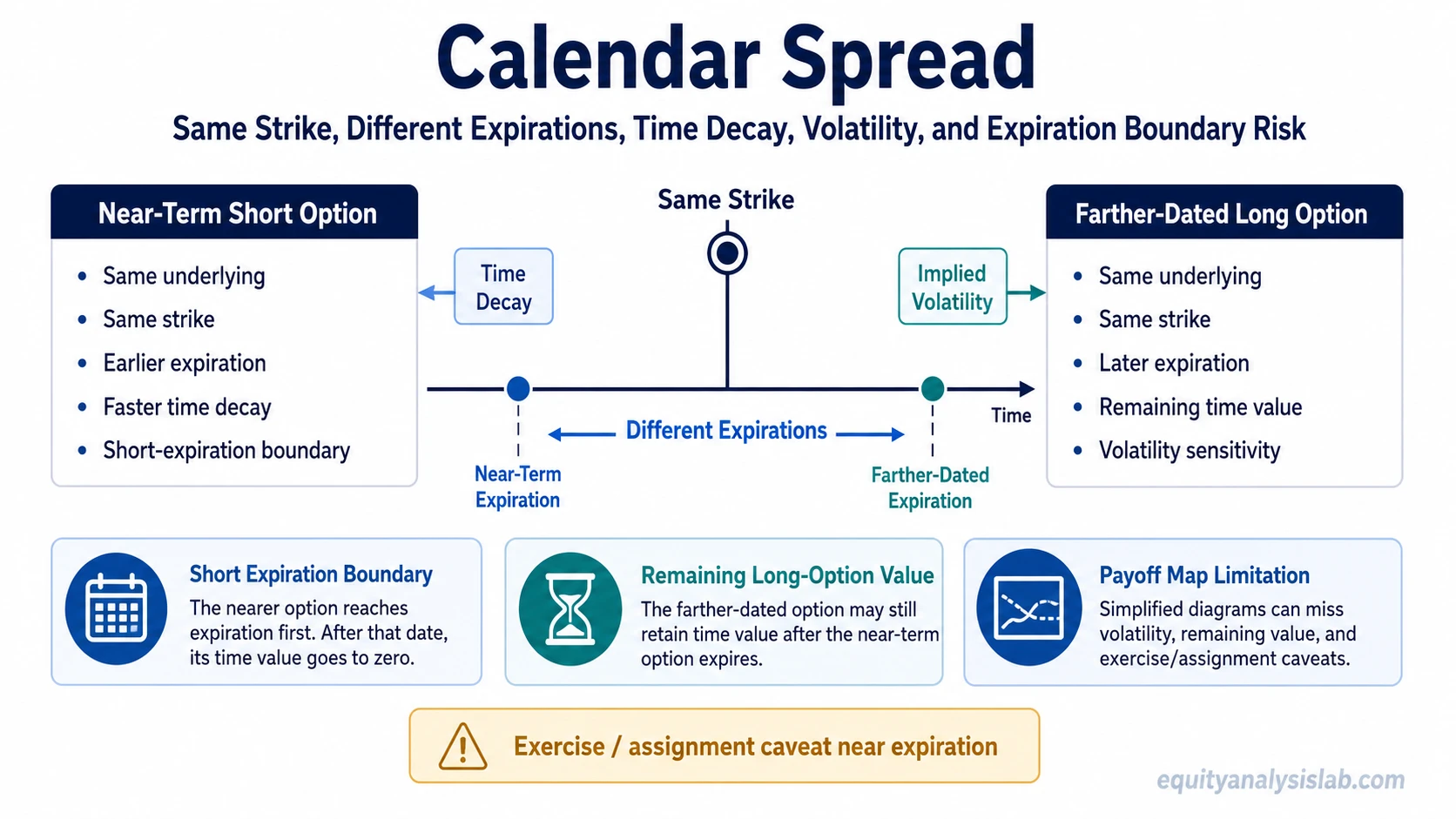

A calendar spread is an options spread that combines two options on the same underlying and strike but with different expiration dates. The structure separates near-term expiration exposure from longer-term option value, so time decay, implied volatility, and price location near the strike all affect interpretation.

Calendar spread definition: a calendar spread, also called a time spread or horizontal spread, uses options with the same underlying asset and the same strike price but different expiration dates. In a typical long calendar spread, the nearer-expiration option is sold and the farther-expiration option is bought.

The defining feature is not a wider strike range. It is the expiration gap. That gap means the short option and the long option can respond differently to time decay, implied volatility, and price movement before the near-term option expires.

Key Points

- A calendar spread uses the same strike with different expiration dates.

- A typical long calendar spread sells the nearer expiration and buys the farther expiration.

- The structure is sensitive to time decay, implied volatility, and where the underlying price sits near the short option expiration.

- Simplified payoff diagrams can miss remaining long-option value, changing volatility, and assignment or exercise risk.

What Is a Calendar Spread?

A calendar spread is an options structure built around expiration separation. Both option legs reference the same underlying asset and the same strike price, but one option expires earlier than the other.

In the common long calendar version, the farther-dated option is long and the nearer-dated option is short. The structure is usually a net-debit spread because the longer-dated option generally carries more time value than the shorter-dated option. That debit is often used as a simplified maximum-loss boundary, but the real risk picture can also depend on assignment, exercise, liquidity, and how the remaining long option is valued after the short option expires.

A calendar spread can be built with calls or puts. A call calendar uses call options at the same strike and different expirations. A put calendar uses put options at the same strike and different expirations. The option type changes the contract exposure, but the core calendar logic remains the expiration mismatch.

How a Calendar Spread Works

The mechanism begins with two time layers. The short option has less time remaining and reaches expiration first. The long option has more time remaining and can retain time value after the short option expires.

| Part of the structure | What it does | Why it matters |

|---|---|---|

| Same underlying | Keeps both option legs tied to the same asset price. | The spread is not a cross-asset or pair structure. |

| Same strike | Centers both legs around one price level. | This separates calendar spreads from diagonal spreads. |

| Different expirations | Creates a near-term leg and a longer-term leg. | Time decay and remaining option value become central. |

| Nearer-expiration short option | Expires first in a typical long calendar spread. | Its expiration can create payoff-map, exercise, or assignment complexity. |

| Farther-expiration long option | Can still have time value after the short option expires. | Its remaining value affects the actual outcome before final expiration. |

A short calendar spread reverses the usual long-calendar construction. The long calendar is the usual baseline for explaining the structure, while short-calendar mechanics create a different risk profile and should not be confused with the standard long-calendar explanation.

Payoff, Time Decay, and Volatility Exposure

A long calendar spread is often explained through time decay, but time decay alone does not define the position. The near-term short option may lose time value faster, while the longer-term option may keep value from remaining time and implied volatility. The spread’s interpretation depends on how these forces interact, not on a single variable.

| Risk question | What changes in a calendar spread? | Interpretation boundary |

|---|---|---|

| Where is the underlying price? | The price location relative to the shared strike shapes the near-expiration payoff area. | A price near the strike may support the simplified payoff map, but it does not guarantee a specific result. |

| How much time remains? | The short option and long option decay on different clocks. | The calendar structure depends on expiration separation, not simply on “time passing.” |

| What happens to implied volatility? | The remaining long option can be sensitive to changes in implied volatility. | Lower or higher implied volatility can change the value left in the longer-dated option. |

| What happens at short expiration? | The short option reaches its decision point before the long option expires. | Exercise or assignment risk can matter, especially when the underlying is near the strike. |

| What is the simplified risk boundary? | A long calendar is commonly entered for a net debit. | The debit is a simplified loss reference, but practical risk can include execution, liquidity, and exercise or assignment effects. |

| What does the payoff map miss? | The longer-dated option may still have time and volatility value after the short option expires. | Maximum profit and breakeven are not fixed as cleanly as in a simple expiration-only vertical spread diagram. |

The strongest calendar-spread explanation is therefore a risk-boundary explanation. It asks what the structure changes across price, time, volatility, expiration, assignment, and remaining option value.

What the Payoff Map Can Miss

A simplified calendar spread payoff map usually focuses on the short option expiration. That can be useful for orientation, but it is incomplete because the longer-dated option does not expire at the same time.

Payoff-map limitation: a calendar spread does not have one fully fixed expiration payoff line until the later-dated option is also resolved. Before that point, the remaining long option can still be affected by implied volatility, time value, bid-ask spread, and the path the underlying price took before the short expiration.

This is why maximum profit and breakeven are usually less precise than they look in a simple diagram. The short option’s expiration creates one boundary, but the value of the remaining long option can still move.

Exercise and assignment deserve separate caution. If the short option is in the money near expiration, assignment or exercise mechanics may affect the position. The exact process depends on the option contract, market, broker rules, and whether the option is American-style or European-style. This draft keeps that point general rather than turning the page into a legal, tax, or platform guide.

Calendar Spread vs Diagonal Spread

A calendar spread uses the same strike price with different expiration dates. A diagonal spread uses different strikes and different expiration dates. That single strike difference changes how the structure behaves.

| Structure | Strike relationship | Expiration relationship | Main boundary |

|---|---|---|---|

| Calendar spread | Same strike | Different expirations | Expiration separation and remaining time value |

| Diagonal spread | Different strikes | Different expirations | Strike separation plus expiration separation |

The distinction matters because a diagonal spread blends vertical-spread and calendar-spread features. A calendar spread is cleaner as a same-strike expiration structure.

Example of a Calendar Spread Structure

Suppose an option chain has two contracts on the same underlying with the same $50 strike. One contract expires in one month, and another expires in three months. A long call calendar could involve selling the one-month $50 call and buying the three-month $50 call. A long put calendar could use the same expiration relationship with puts.

Illustrative structure only: the example shows contract relationships, not a recommendation. It does not say that the spread should be opened, held, adjusted, closed, or rolled. It also does not assume any real ticker, price path, volatility move, or investment outcome.

The useful lesson is the separation between the short option’s near-term expiration and the longer option’s remaining value. If the underlying is near the shared strike as the short option approaches expiration, the simplified payoff map may look centered around that strike. But the final interpretation still depends on volatility, remaining time value, exercise or assignment mechanics, and execution conditions.

Related Spread Structures

Calendar spreads are different from vertical debit and credit spreads because the main design feature is expiration separation rather than strike separation. A bear put spread uses two put strikes to define a bearish debit-spread payoff boundary.

A bull call spread uses two call strikes to define a bullish debit-spread boundary, so its structure is organized around strike width rather than a same-strike expiration gap.

Credit-spread structures also use strike width differently from a calendar spread. A put credit spread is usually organized around short and long put strikes in the same expiration cycle, rather than the same strike across different expirations.

FAQ

What is a calendar spread in options?

A calendar spread is an options spread using the same underlying asset and same strike price with different expiration dates. In the common long version, the nearer-expiration option is sold and the farther-expiration option is bought.

Why is a calendar spread also called a time spread?

It is called a time spread because the main structural difference between the two option legs is expiration date. The position separates near-term option decay from longer-term option value.

Is a calendar spread the same as a diagonal spread?

No. A calendar spread uses the same strike with different expirations. A diagonal spread uses different strikes and different expirations, so it adds strike separation to the expiration difference.

Does a calendar spread have a fixed maximum profit?

Not in the same clean way as a simple same-expiration vertical spread. The value of the longer-dated option can still depend on implied volatility, remaining time value, and market conditions when the short option expires.