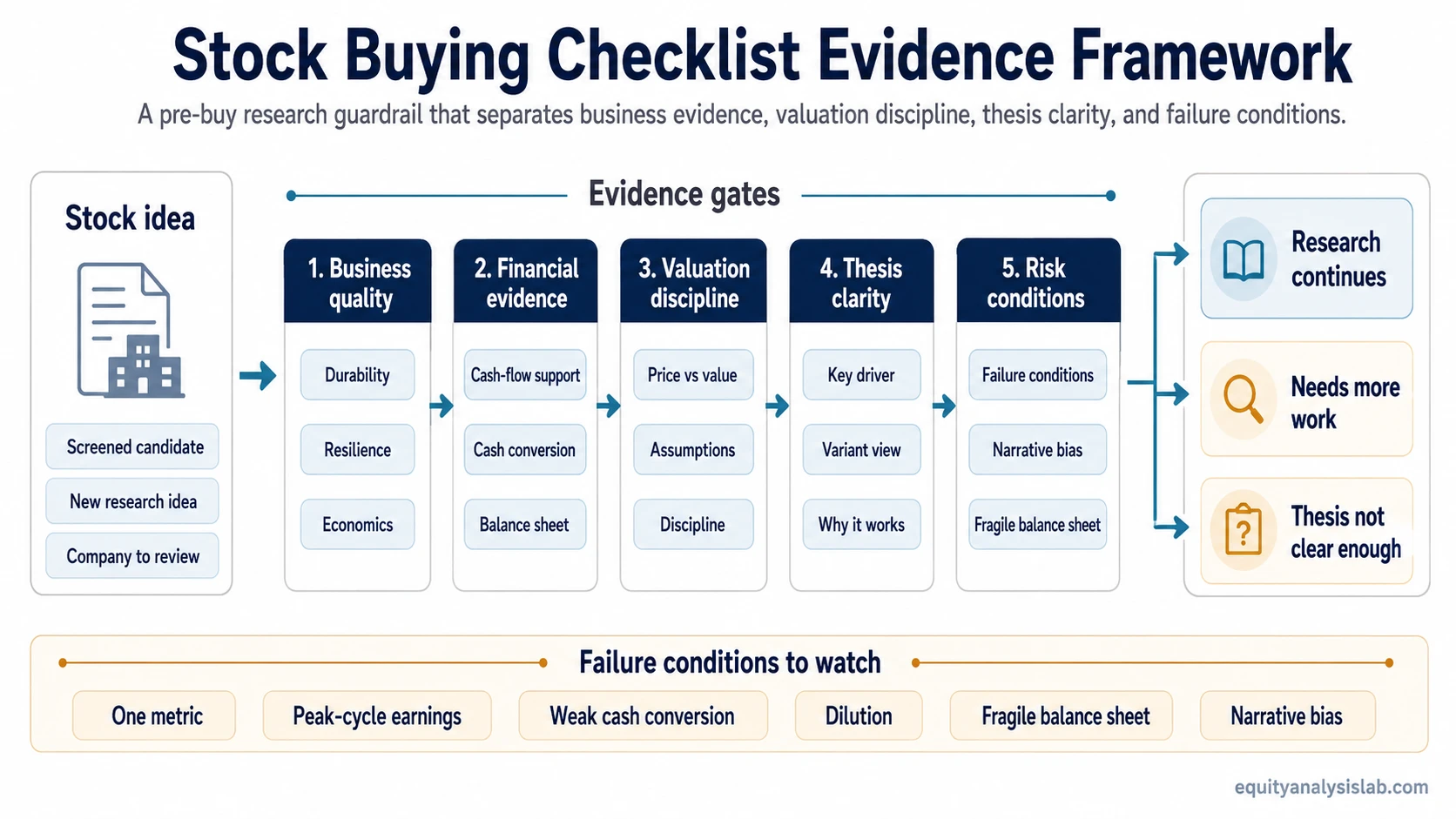

A stock buying checklist is a pre-buy research guardrail for testing whether a company’s business quality, financial evidence, valuation, thesis fit, and risk conditions support further investment work.

The checklist should reduce decision error. It should not turn a stock into an automatic yes/no decision, a buy signal, a trade plan, or a scorecard that replaces judgment.

A useful checklist separates business evidence, cash-flow support, valuation discipline, thesis clarity, and failure conditions before an investor treats a stock idea as investable.

Definition: A stock buying checklist is a structured review used before an investor treats a stock idea as investable. It tests the business, the financial evidence, the price paid, the thesis, and the conditions that could make the idea weaker than it first appears.

Key Points

- A checklist is a research guardrail, not a buy signal.

- Business quality, cash flow, valuation, thesis fit, and risk conditions need to work together.

- A screen can surface candidates, but the checklist tests whether the idea deserves deeper review.

- Weak answers should pause the decision, not create a mechanical rejection every time.

- The checklist fails when it becomes a justification tool after the investor has already decided.

What a Stock Buying Checklist Should Test

A useful checklist starts with the business rather than the share price. Product familiarity, brand recognition, or a popular story can make a company feel easier to understand than it really is. The first check is whether the business model, customer demand, margins, competitive position, and capital needs can be explained without relying on excitement alone.

The financial review then tests whether reported earnings have support from cash flow, margins, debt capacity, and share-count discipline. Earnings improvement is more useful when revenue, margins, cash conversion, and forward assumptions point in the same general direction. EPS growth without cash-flow support, heavy dilution, or a fragile balance sheet should slow the review.

Valuation discipline keeps the checklist from treating a good company as automatically attractive at any price. A strong business can still require conservative assumptions, an estimate range, and a clear margin of safety before price and value appear aligned.

The final check is thesis clarity. A stock idea should not rest on a vague narrative, a single metric, or a recent price move. The investor should be able to state the core investment thesis, what evidence supports it, what could weaken it, and what new information would require more work.

Stock Buying Checklist Framework

The strongest checklist items are not isolated boxes. Each item should connect an evidence question to what would strengthen the interpretation, what would weaken it, and which deeper concept deserves review when the answer is unclear.

| Checklist stage | Evidence question | Strengthens the reading | Weakens the reading | Related review |

|---|---|---|---|---|

| Business quality | Is the business durable and understandable? | Recurring demand, pricing power, clear unit economics, and a visible economic moat. | Product admiration without economics, weak customer durability, or a story that depends mainly on popularity. | Business durability and competitive advantage review. |

| Financial evidence | Do earnings have cash-flow support? | Cash conversion, stable or improving margins, manageable debt, and limited dilution pressure. | EPS improvement without cash flow, rising leverage, fragile liquidity, or ownership dilution that offsets growth. | Financial quality review. |

| Valuation discipline | Does price leave room for error? | Conservative estimate range, assumptions that do not require perfection, and room for valuation error. | Peak-cycle earnings, optimistic growth assumptions, or a valuation that only works under the best case. | Price versus estimated value review. |

| Thesis fit | Is the reason for owning the stock clear? | An evidence-backed thesis that connects business quality, financial support, valuation, and risk. | Narrative, hype, unclear driver, or reliance on one metric without supporting evidence. | Thesis clarity review. |

| Screening boundary | Did a screen find an idea, or did analysis support it? | A screen is used as a starting filter before deeper company review. | A screener result is treated as a conclusion before business, valuation, and risk checks are complete. | Filtering versus judgment review. |

Manual review gate: A weak checklist answer does not always mean permanent rejection. Some answers mean the idea needs more evidence, a better estimate range, cleaner financial support, or a clearer thesis before it belongs on an investable list.

Checklist Review vs Stock Screener Filtering

A stock screener filters a large universe into a smaller set of candidates. It can sort by valuation multiples, margins, returns on capital, growth rates, leverage, dividend data, or other measurable fields.

A stock buying checklist comes after that filter. It asks whether the numbers make sense together, whether the business evidence supports the metrics, whether valuation assumptions are reasonable, and whether the thesis is clear enough to continue.

Screening question: Which companies meet a chosen filter?

Checklist question: Does one candidate have enough business, financial, valuation, and thesis evidence to deserve further investment work?

A Pre-Buy Checklist Scenario

A screen surfaces a company with rising earnings, moderate debt, and a valuation that appears inexpensive against comparable businesses. The checklist begins by asking whether the business is understandable, whether demand is recurring, and whether the company has any durable advantage beyond a familiar product or strong brand impression.

The next review compares earnings with operating cash flow, margins, working-capital needs, and share-count changes. If earnings have improved but cash conversion is weak or dilution is absorbing much of the growth, the checklist does not treat the headline EPS trend as enough evidence.

The valuation review then tests whether the estimate range depends on peak margins, unusually strong demand, or aggressive growth assumptions. Cyclical businesses need extra caution because a low multiple can look attractive near peak earnings while cash flow and margins are already vulnerable.

The final step is thesis clarity. If the investor cannot explain why the business should remain durable, why the valuation leaves room for error, and what would weaken the case, the idea stays in further research rather than moving automatically into an investable list.

When a Stock Buying Checklist Fails

A checklist fails when it becomes a ritual instead of a decision guardrail. The most common failure is using the checklist after the decision has already been made, then selecting only the evidence that supports the preferred conclusion.

Common failure conditions:

- One-metric overfiltering: A low multiple, high growth rate, or strong margin is treated as enough evidence by itself.

- Peak-cycle earnings: A cyclical company looks cheap because profits are near a favorable point in the cycle.

- Weak cash conversion: Accounting earnings improve while operating cash flow, working capital, or free cash flow tells a weaker story.

- Dilution: Business growth does not fully benefit shareholders because the share count keeps rising.

- Balance-sheet fragility: Debt, refinancing needs, or liquidity pressure reduces the room for error.

- Ignored valuation: A high-quality business is treated as attractive without testing the price paid.

- Product admiration: Liking a product or brand replaces analysis of economics, cash flow, durability, and valuation.

- Narrative bias: The checklist is used to defend a story rather than test it.

How to Treat Unclear Checklist Results

Checklist output is more useful when it separates decision states rather than forcing a simple pass or fail. A company can remain interesting while still lacking enough evidence for an investable thesis.

| Checklist result | What it means | Next analytical state |

|---|---|---|

| Research continues | The business, financial evidence, valuation, and thesis are directionally coherent. | Deepen estimates, risks, scenario ranges, and portfolio fit. |

| Needs more work | Some evidence is promising, but one or more checks remain unresolved. | Review financial statements, assumptions, debt, dilution, or thesis drivers. |

| Thesis not clear enough | The idea depends mainly on narrative, screening output, cheapness, or recent price movement. | Keep outside the investable list until evidence improves. |

Limitation: A checklist cannot remove uncertainty. It can only organize the evidence, highlight weak links, and reduce the chance that a decision is driven by price action, product familiarity, or a single attractive metric.

FAQ

Is a stock buying checklist a buy signal?

No. A stock buying checklist is a research guardrail. It can support further analysis when evidence is coherent, but it does not make a stock automatically investable.

What should a checklist include before buying a stock?

It should include business quality, financial evidence, valuation discipline, thesis clarity, balance-sheet risk, dilution review, and failure conditions that would slow the decision.

How is a checklist different from a stock screener?

A screener filters candidates using measurable fields. A checklist reviews whether a specific candidate has enough business, financial, valuation, and thesis evidence to deserve deeper work.

Does one weak checklist item end the review?

Not always. Some weak answers call for more research rather than permanent rejection. The important point is that unresolved evidence should slow the decision.