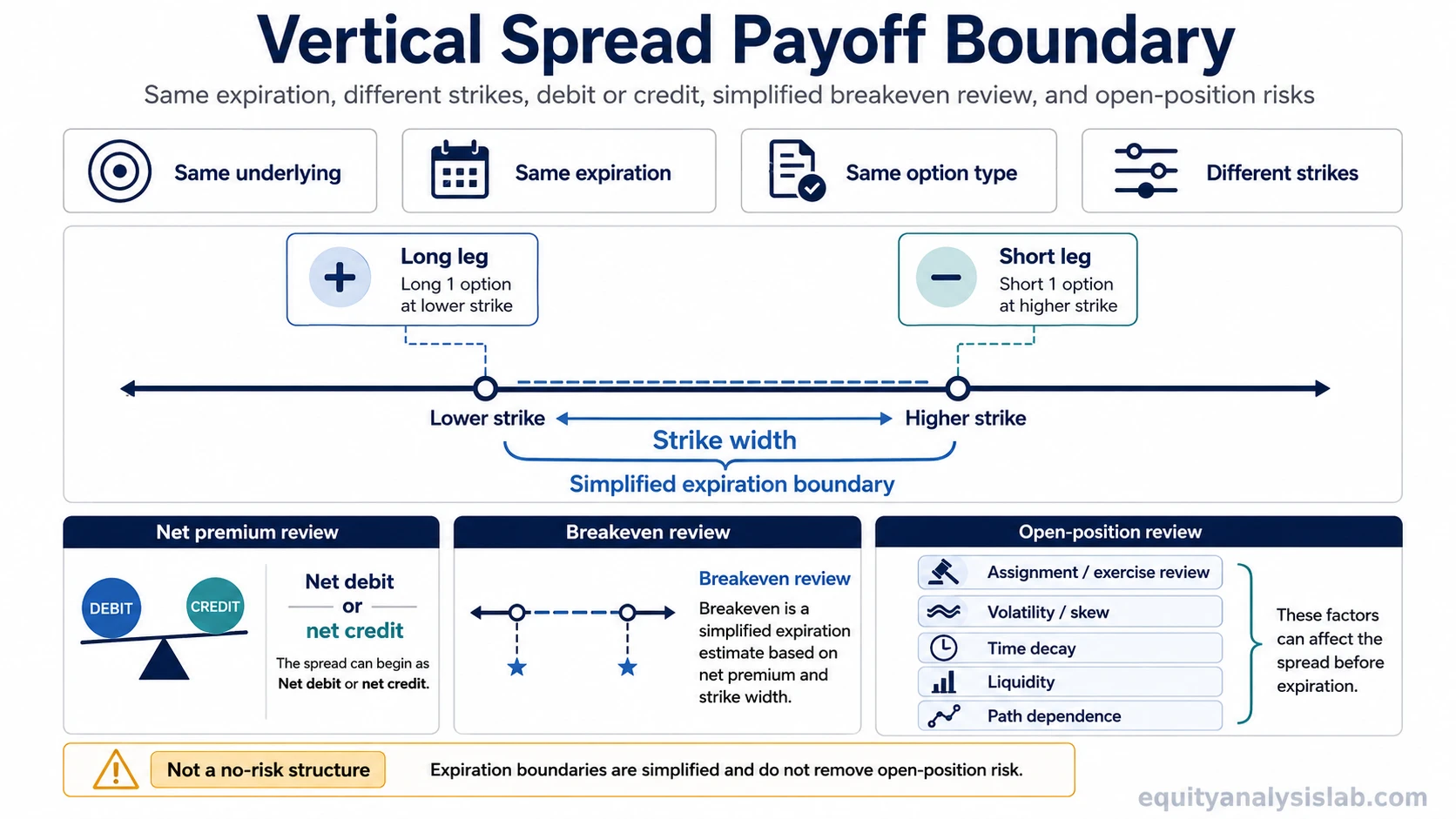

A vertical spread is an options spread that uses the same underlying asset, the same expiration date, the same option type, and two different strike prices. The strike difference creates the spread’s simplified expiration boundary, while the shared expiration keeps the structure vertical rather than calendar-based or diagonal.

That boundary is an expiration view, not a complete description of risk while the position is open. Assignment or exercise review, liquidity, implied volatility, skew, time decay, and the underlying asset’s path can still change the spread’s market value before expiration.

What Is a Vertical Spread?

A vertical spread is a two-leg options structure built with one long option and one short option on the same underlying asset. Both legs use the same expiration date and the same option type, but they have different strike prices.

The word “vertical” refers to the strike-price difference. On an options chain, strike prices are commonly displayed vertically, while expiration dates are separated across time. A vertical spread changes strike exposure while keeping expiration constant.

Key Points

- A vertical spread uses two options with the same expiration and different strikes.

- The structure can be built with calls or puts.

- The spread can begin as a net debit or a net credit depending on the premiums paid and received.

- Strike width and net premium shape the simplified expiration payoff boundary.

- Defined expiration boundaries do not remove assignment, exercise, liquidity, volatility, or open-position value risk before expiration.

How a Vertical Spread Works

A vertical spread combines a long option leg with a short option leg. The long leg creates exposure at one strike, while the short leg offsets premium or changes the payoff profile at another strike. Because both legs expire on the same date, the structure is mainly defined by strike distance and net premium.

The distance between the two strikes sets the maximum intrinsic-value gap the spread can have at expiration. The net premium determines whether the position starts as a debit or a credit and where the simplified breakeven sits.

| Component | Role in the vertical spread | What to review |

|---|---|---|

| Long option leg | Creates exposure at one strike. | Premium paid, remaining time value, and sensitivity to volatility. |

| Short option leg | Offsets premium or caps part of the payoff profile. | Assignment or exercise risk, especially near expiration or around dividends where relevant. |

| Strike width | Sets the maximum intrinsic-value distance between the two legs at expiration. | Whether the width matches the intended expiration boundary. |

| Net premium | Determines whether the spread starts as a debit or credit. | How the debit or credit affects breakeven and expiration payoff. |

| Same expiration | Keeps the structure vertical rather than diagonal or calendar-based. | How both legs behave as expiration approaches. |

Debit vs Credit Vertical Spreads

A vertical spread is classified by its initial net premium. A debit vertical spread costs money to open before fees and commissions. A credit vertical spread receives money upfront before fees and commissions. That cash-flow label does not by itself make one structure safer, better, or more attractive.

| Classification | Initial cash flow | Basic interpretation | Risk note |

|---|---|---|---|

| Debit vertical spread | Net premium paid | The long leg costs more than the premium received from the short leg. | A lower debit does not automatically mean a better risk/reward profile. |

| Credit vertical spread | Net premium received | The short leg brings in more premium than the long leg costs. | Credit received is not pure income; the spread can still move toward its loss boundary. |

Main Types of Vertical Spreads

Vertical spreads are usually grouped by option type, strike order, and whether the structure begins as a debit or credit. The table below is a taxonomy, not a trade instruction.

| Vertical spread type | Option type | Typical premium category | High-level payoff idea |

|---|---|---|---|

| Bull call spread | Calls | Debit | Uses a lower-strike long call and a higher-strike short call, creating capped upside exposure at expiration. |

| Bear put spread | Puts | Debit | Uses a higher-strike long put and a lower-strike short put, creating capped downside exposure at expiration. |

| Bull put spread | Puts | Credit | Uses a higher-strike short put and a lower-strike long put, creating a defined expiration boundary before costs. |

| Bear call spread | Calls | Credit | Uses a lower-strike short call and a higher-strike long call, creating a capped credit-spread profile at expiration. |

What the Payoff Boundary Shows

The simplified payoff boundary shows how the spread behaves at expiration before transaction costs, taxes, early assignment, exercise decisions, and changes in open-position market value. It is useful for understanding the structure, but it should not be treated as the whole risk picture.

| Boundary item | What it usually tells you | What it does not fully capture |

|---|---|---|

| Strike width | The maximum intrinsic-value distance between the two strikes at expiration. | How volatility, skew, or liquidity can affect the spread before expiration. |

| Net debit | The amount paid to open a debit vertical spread before costs. | Whether the spread will hold that value before expiration. |

| Net credit | The amount received to open a credit vertical spread before costs. | Whether the credit compensates adequately for the risk being carried. |

| Breakeven | A simplified expiration price where the net premium is offset. | The mark-to-market value of the spread before expiration. |

| Maximum expiration outcome | The capped profit or loss range implied by the strikes and net premium. | Assignment timing, exercise decisions, slippage, bid-ask spreads, or changing implied volatility. |

Breakeven and Boundary Review

A debit call vertical spread generally has a simplified expiration breakeven near the lower strike plus the net debit. A debit put vertical spread generally has a simplified expiration breakeven near the higher strike minus the net debit.

For credit vertical spreads, the simplified expiration breakeven is usually adjusted from the short strike by the net credit received. Those formulas are useful for structure review, but they do not show how the spread can trade before expiration when volatility, skew, time value, and liquidity change.

What the Payoff Boundary Can Miss

A payoff diagram normally simplifies the position as if both legs are held to expiration. That view can hide several issues that still matter while the spread is open.

- Assignment and exercise review: the short leg can create assignment risk, and the long leg may require an exercise decision near expiration.

- Open-position value: the spread can gain or lose value before expiration even when the expiration boundary appears defined.

- Implied volatility and skew: changes in option pricing can affect the two legs differently.

- Liquidity: wide bid-ask spreads or thin markets can make entry, adjustment, or exit less efficient.

- Path dependence: the route the underlying takes before expiration can affect risk, stress, and decision points.

- Time decay and extrinsic value: both legs can lose or retain time value at different rates before expiration.

Simple Vertical Spread Example

Assume a call vertical spread uses a long call at a 50 strike and a short call at a 55 strike with the same expiration. The strike width is 5 points. If the spread is opened for a 2-point net debit, the simplified expiration boundary is shaped by the 5-point width and the 2-point cost.

In that simplified expiration view, the spread cannot be worth more than the distance between the strikes before costs. The net debit reduces the potential expiration gain and represents the amount at risk if both calls expire without intrinsic value.

Before expiration, the same 50/55 spread can look different from the final payoff diagram. A volatility change, a wider bid-ask spread, a fast move toward the short strike, or a slow path that erodes time value can all change the mark-to-market value before the expiration outcome is known.

Common Misunderstandings

Defined expiration risk is not the same as no risk. The spread may have a bounded payoff at expiration, but the position can still require review before expiration.

Credit received is not pure income. A credit vertical spread receives premium upfront, but that premium compensates for risk. The spread can still move toward its loss boundary.

A lower net debit is not automatically better. Reducing cost by adding a short leg also changes the payoff profile and can cap part of the exposure.

Vertical and diagonal spreads are not the same structure. A vertical spread keeps expiration the same and changes strikes. A diagonal spread changes both strike and expiration.

Related Vertical Spread Concepts

Each vertical spread type has its own structure, payoff boundary, and risk review. Bull call spreads and bear put spreads are debit structures. Bull put spreads and bear call spreads are credit structures. The shared vertical-spread idea is the same-expiration, different-strike relationship, but each type deserves separate review rather than being treated as interchangeable.

Vertical Spread FAQ

Is a vertical spread always a debit spread?

No. A vertical spread can be a debit or credit structure. The classification depends on whether the initial premium paid is greater or smaller than the premium received.

Does a vertical spread remove assignment risk?

No. A long leg can define part of the expiration payoff boundary, but the short leg can still require assignment or exercise review.

Is defined expiration risk the same as no risk?

No. Defined expiration boundaries describe a simplified outcome at expiration. The spread can still change value before expiration because of volatility, time decay, liquidity, and the underlying asset’s path.