Hindsight bias is the tendency to see an investment outcome as more obvious or predictable after it has already happened. In investor decision review, the risk is not only that a past result is remembered incorrectly, but that earlier evidence is reconstructed to make the outcome feel easier to foresee than it actually was.

Definition: Hindsight bias occurs when outcome knowledge changes how an investor remembers prior evidence, prior uncertainty, or prior judgment. It is often described as a “knew it all along” effect, but in investing the more useful focus is the review problem: the final result can make a messy decision record look clearer than it was at the time.

Key Points

- Hindsight bias appears after an outcome is known, not before the decision is made.

- It can make earlier evidence look stronger, cleaner, or more predictive than it was.

- For investors, the main risk is weak post-outcome learning from a distorted memory of the decision process.

- A checklist can reduce the effect by preserving the original evidence, alternatives, uncertainty, and risk reasoning.

- Hindsight bias review does not prove that a decision was wrong, irrational, or that any specific portfolio action was correct.

What Is Hindsight Bias?

Hindsight bias is a post-outcome judgment error. After a stock, fund, sector, or broader market event moves in a visible direction, the investor may remember the earlier setup as if the result was obvious. That memory can feel convincing because the outcome is already known.

The problem is that investment decisions are usually made under uncertainty. Before the result, the evidence may have included mixed earnings signals, valuation tension, competing scenarios, unclear sentiment, or risk that had not yet become visible. Hindsight bias compresses that uncertainty into a cleaner story after the fact.

In an investing context, the concept belongs inside decision review rather than broad psychology. The useful question is not whether the investor “should have known.” The useful question is whether the post-outcome review still matches the evidence that was available before the outcome.

How Hindsight Bias Affects Investor Review

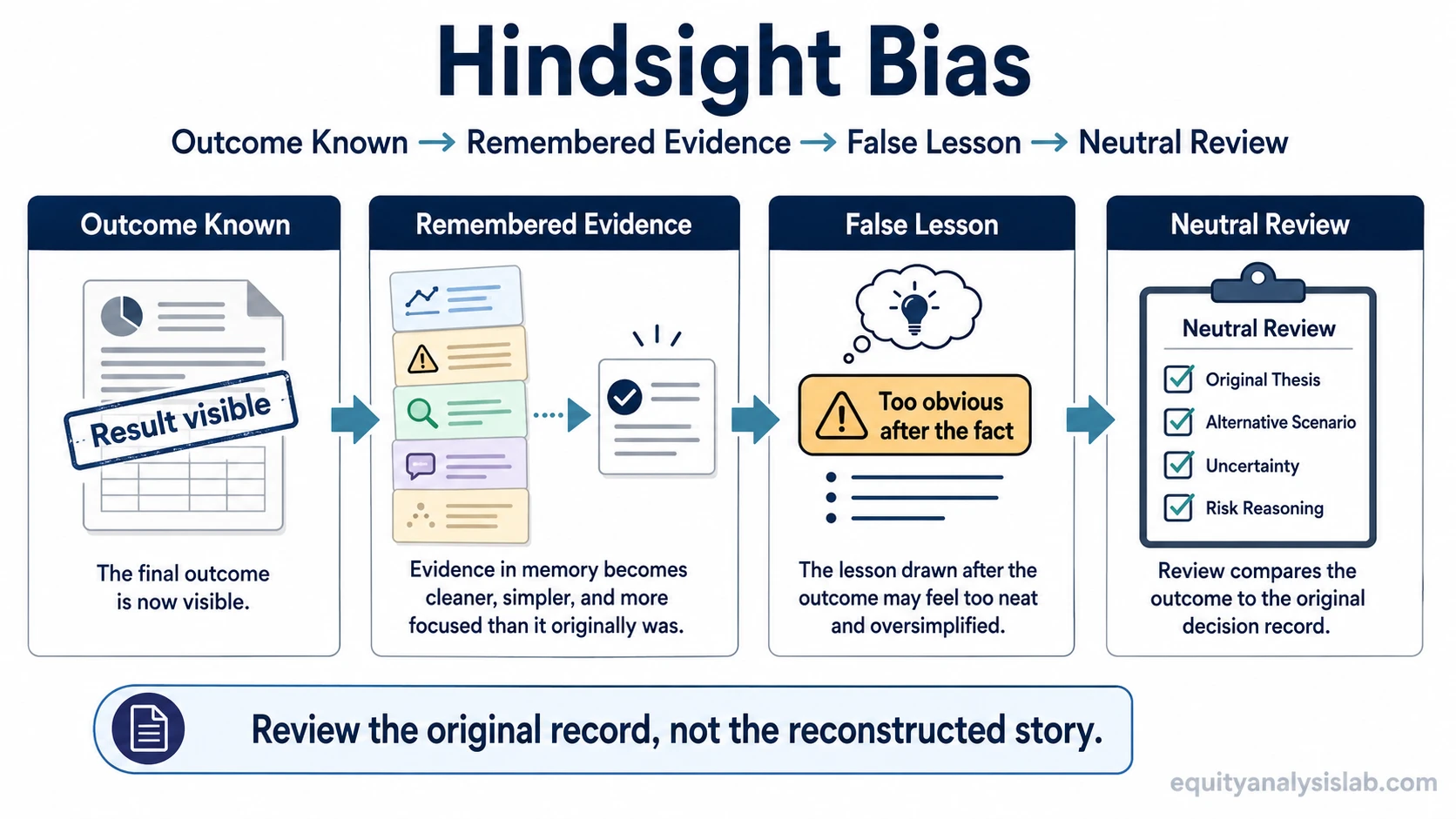

Hindsight bias can weaken investment review by changing the lesson an investor takes from a past result. A correct outcome may be remembered as proof that the original reasoning was strong, even if the decision was partly lucky. A poor outcome may be remembered as obviously avoidable, even if the evidence was genuinely balanced at the time.

Review mechanism: outcome knowledge can lead to reconstructed evidence, reconstructed evidence can create a false lesson, and the false lesson can weaken the next checklist decision.

| Review stage | How hindsight bias can distort it | Better review question |

|---|---|---|

| Original evidence | The investor remembers the evidence as cleaner than it was. | What was actually known before the outcome? |

| Alternative scenario | The rejected scenario is treated as if it never had a reasonable case. | What could have made the opposite outcome plausible? |

| Decision confidence | The final result changes how confident the investor remembers being. | Was confidence documented before the result? |

| Position pressure | A past result becomes a reason to overcorrect future risk review or confidence. | Did the review separate process quality from outcome emotion? |

| Lesson learned | The investor draws a simple rule from a complex decision. | What lesson survives if the outcome is removed from the review? |

How It Shows Up in an Investment Checklist

Hindsight bias often appears when an investor reviews a checklist only after the result is already visible. A checklist that was incomplete before the outcome may feel complete afterward because the final result supplies a story that the original notes did not contain.

Common checklist failure: the investor reviews the final result more carefully than the original decision record. This can turn outcome review into story reconstruction instead of evidence review.

A useful checklist should record the original thesis, the main uncertainty, the alternative scenario, the evidence that would weaken the thesis, and the risk reasoning that shaped the decision record. Without that record, the investor may later remember the decision through the outcome rather than through the evidence that existed at the time.

This is also where selective evidence can become a problem. If the investor only remembers facts that supported the final story, the review starts to resemble evidence filtering rather than neutral learning.

Hindsight Bias Example in Investor Decision Review

Consider an investor who followed a company with mixed evidence. Revenue growth looked strong, but margins were weakening, cash conversion was uneven, and management guidance depended on a favorable demand environment. Before the earnings release, the investor wrote down two scenarios: a bullish case if margins stabilized and a cautious case if cash flow continued to lag reported growth.

After the stock fell on disappointing results, hindsight bias could make the negative outcome feel obvious. The investor might say the warning signs were clear all along, even though the original notes showed a mixed setup rather than a one-sided conclusion.

The better review is more precise. The investor can ask whether the cash-flow warning deserved more weight, whether the alternative scenario was documented clearly, whether the original risk reasoning reflected uncertainty, and whether the process missed evidence that was available before the outcome. That review improves the next decision without pretending the future was fully knowable.

Decision-review guardrail: write the pre-outcome evidence before the result is known. A useful review compares the later outcome with the original thesis, not with a reconstructed version of the thesis.

Hindsight Bias vs Related Behavioral Biases

Hindsight bias overlaps with other investor psychology problems, but it should not absorb them. Its defining feature is timing: the distortion appears after the outcome is known.

| Bias | Main distortion | Boundary against hindsight bias |

|---|---|---|

| anchoring bias | Judgment stays tied to a fixed reference point. | Anchoring can shape the decision before the outcome, while hindsight bias reshapes the review after the outcome. |

| availability bias | Vivid, recent, or easy-to-recall information receives too much weight. | Availability can affect what evidence feels most salient, while hindsight bias changes how predictable the result feels later. |

| selective evidence review | Evidence that supports an existing belief receives more attention than conflicting evidence. | Confirmation bias can operate during research, while hindsight bias often appears when the investor reviews the decision after the result. |

The distinction matters because each bias calls for a different review tool. Hindsight bias is best checked with pre-outcome notes, decision logs, alternative scenarios, and post-outcome comparison against the original evidence record.

Why Hindsight Bias Can Weaken Post-Outcome Learning

Post-outcome learning is useful only if it separates process quality from result quality. A good result can come from weak reasoning, and a poor result can come from a reasonable process that faced adverse conditions. Hindsight bias blurs that distinction by making the final outcome dominate the review.

The investor may then learn the wrong lesson. A profitable decision may encourage excessive confidence because the outcome confirms the story. A losing decision may encourage excessive caution because the loss feels obvious in retrospect. In both cases, the review becomes less about what was knowable and more about what happened.

Cleaner review sequence: preserve the original thesis, record the evidence that supported and challenged it, mark the alternative scenario, then compare the final outcome against that record. This keeps the review tied to decision quality rather than outcome hindsight.

Limits of Hindsight Bias Review

Hindsight bias is a review lens, not a verdict. It does not prove that an investor was wrong, irrational, careless, or that a specific portfolio action was correct. It also does not prove that an outcome was predictable.

Important limitation: hindsight bias review should improve evidence discipline, not create certainty. The goal is to compare the original decision record with the later outcome, while preserving the uncertainty that existed before the result was known.

The concept is most useful when it helps the investor ask better process questions: Was the original evidence recorded accurately? Were alternatives considered? Was confidence calibrated? Did the final result change the memory of the decision? Those questions can improve review quality without turning the outcome into investment advice.

FAQ

What is hindsight bias in investing?

Hindsight bias in investing is the tendency to see a market or company outcome as more obvious after it has happened. It can distort how the investor remembers the evidence that was available before the result.

Why is hindsight bias a problem for investors?

It can weaken post-outcome learning. The investor may judge the original decision through the final result instead of reviewing the evidence, uncertainty, alternatives, and process that existed at the time.

Does hindsight bias mean the investor made a bad decision?

No. Hindsight bias does not prove that a decision was bad or irrational. It only describes a review risk where the known outcome changes how the earlier decision is remembered.

How can an investor reduce hindsight bias during review?

An investor can reduce hindsight bias during review by recording the original thesis, uncertainty, alternative scenario, evidence limits, and risk reasoning before the outcome is known. The later review should compare the result with that original record.