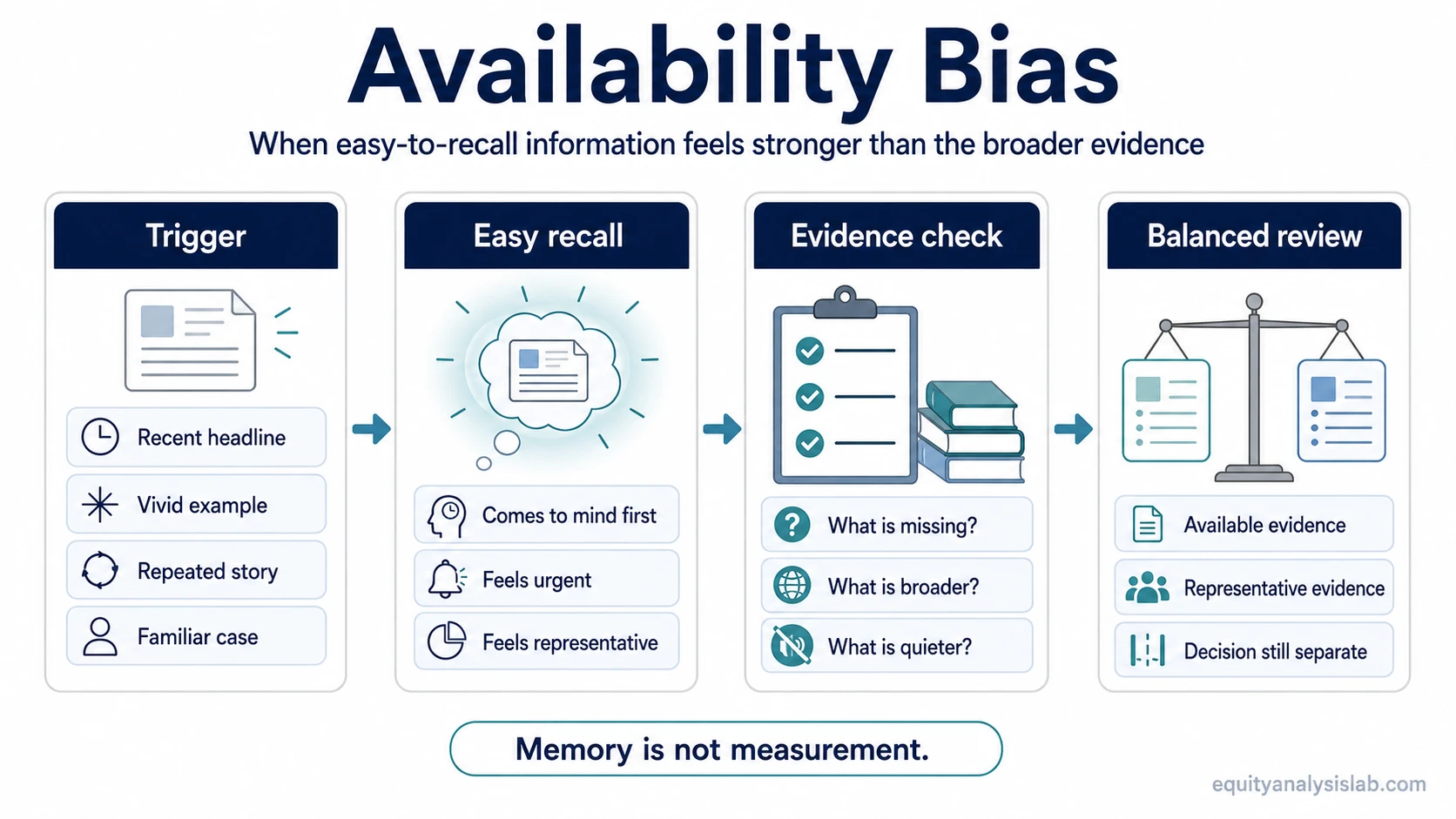

Availability bias is the tendency to give too much weight to information that comes to mind easily, especially when that information is recent, vivid, familiar, or emotionally memorable. In an investing review, the risk is not that the investor is automatically wrong. The risk is that easy-to-recall evidence can feel more representative than it really is.

A recent headline, a memorable earnings surprise, or a familiar market story can pull attention toward the facts that are most visible and away from inputs that are broader, older, quieter, or less dramatic. The useful question is not only “What do I remember?” but also “Is what I remember a fair sample of the evidence?”

Definition: Availability bias is a behavioral bias where readily available information receives more influence than less visible but potentially more representative information. For investors, it can distort the judgment process by making recent news, vivid examples, or familiar stories feel stronger than a fuller data set.

- Availability bias gives extra weight to information that is easy to recall.

- In investing, the main risk is evidence selection, not proof that the conclusion is wrong.

- The bias often appears after vivid headlines, memorable cases, repeated news exposure, or recent personal experience.

- A checklist can slow the move from memorable evidence to portfolio judgment.

- The practical test is whether the available evidence is also representative evidence.

How availability bias changes investor decision review

Availability bias affects the order and weight of evidence. The input that appears first in memory can begin to shape the investment review before the investor has compared it with a wider set of relevant facts.

This can happen when a recent earnings headline receives more attention than several years of margin history, when a memorable collapse in one company makes a whole sector feel riskier than its data suggests, or when repeated media coverage makes one risk factor feel more dominant than quieter balance-sheet, valuation, or cash-flow evidence.

The bias becomes more important when the available information is vivid but incomplete. A dramatic example may be useful as a warning, but it does not automatically replace a wider review of company fundamentals, valuation assumptions, competitive position, earnings quality, and portfolio role.

Available evidence vs representative evidence

The central distinction is between evidence that is easy to retrieve and evidence that fairly represents the question being reviewed. Available evidence may be true, but still incomplete. Representative evidence is broader, more balanced, and closer to the decision being made.

| Evidence type | What it means | Investor risk |

|---|---|---|

| Available evidence | Information that is recent, vivid, familiar, repeated, or easy to remember. | It can feel more important than it deserves because it is mentally easy to access. |

| Representative evidence | Evidence that reflects the broader base of relevant facts for the decision. | It may be less dramatic, but it gives a more balanced view of the investment question. |

| Checklist evidence | Information reviewed through a defined process instead of memory alone. | It reduces the chance that one memorable input dominates the whole decision. |

Availability bias often begins when the investor treats the first category as if it were the second. The evidence may be real, but the weighting may be distorted.

A practical investor checklist scenario

An investor reviewing a company sees a recent headline about disappointing earnings. The headline is easy to remember because it is new, specific, and widely discussed. That information may deserve attention, but it can become misleading if it crowds out older evidence about revenue durability, margin trend, balance-sheet strength, cash generation, and management guidance.

A cleaner review separates the trigger from the conclusion:

- Trigger: What recent or vivid information pulled attention into the decision?

- Evidence used: Which facts are receiving the most weight right now?

- Evidence ignored: Which relevant facts are missing from the first reaction?

- Broader sample: Does the visible evidence match a longer or wider record?

- Decision pressure: Is the investor rushing because the information feels urgent?

The checklist does not decide whether the investment is attractive or unattractive. It forces the review to compare vivid evidence with a broader record before judgment hardens.

Common mistake: treating easy recall as stronger evidence

The common mistake is assuming that the evidence that comes to mind first is the evidence that matters most. A memorable example can be useful, but memory is not the same as measurement.

For investors, this mistake can affect thesis updates, watchlist reviews, portfolio risk checks, and company comparisons. A recent negative story may make a business feel permanently impaired. A recent positive story may make a weak thesis feel stronger than the underlying facts support. In both cases, availability bias changes the evidence weight before the investor has tested whether the evidence is representative.

Availability bias does not mean the conclusion is wrong

Availability bias is a warning about process, not a verdict on the final conclusion. The easily recalled information may be accurate. A recent warning sign may be relevant. A vivid example may point to a real risk.

The problem appears when the information becomes dominant only because it is easy to remember. A more controlled review asks whether the same conclusion still holds after less visible evidence is included.

A checklist for reviewing availability bias

A useful guardrail is to slow the decision at the point where vivid evidence begins to feel decisive. The goal is not to ignore recent information. The goal is to place it inside a fuller review.

| Checklist step | Question to ask | What it protects against |

|---|---|---|

| Name the trigger | What made this issue feel urgent or important? | Confusing salience with importance. |

| List the visible evidence | Which facts are easiest to recall right now? | Letting recent or familiar inputs dominate silently. |

| Search for missing evidence | What relevant data would be easy to overlook? | Ignoring quieter evidence such as longer-term trends or base rates. |

| Compare the evidence base | Does the visible evidence represent the broader record? | Overweighting one example, one headline, or one recent event. |

| Separate review from action | Is the decision being pushed by evidence or by urgency? | Turning a memorable input into an immediate portfolio decision. |

Where availability bias appears in investor decisions

Availability bias can appear in many parts of an investor’s process. It may affect how a company is first screened, how an investment thesis is updated, how risk is judged after bad news, or how portfolio exposure feels after a recent market move.

- Company review: A recent earnings miss may dominate a longer record of business quality or cash-flow resilience.

- Sector judgment: A memorable failure in one company may make an entire industry feel weaker than the evidence suggests.

- Risk review: A vivid market drawdown may make current risk feel higher even when the underlying setup is different.

- Thesis update: Repeated headlines may make one factor feel central while other thesis drivers receive too little attention.

In each case, the investor does not need to dismiss the available evidence. A more evidence-aware process tests whether that evidence is proportionate to the whole decision.

Availability bias vs nearby behavioral biases

Availability bias overlaps with other investor psychology concepts, but it has a specific role: it is about evidence becoming influential because it is easy to recall.

| Bias | Main distortion | Investor distinction |

|---|---|---|

| Anchoring bias | A starting reference point remains too sticky. | The problem is the pull of an initial number, estimate, or prior view. |

| Confirmation bias | Evidence that supports an existing belief receives preferred treatment. | The problem is favoring thesis-supporting evidence over contradictory evidence. |

| Framing bias | The presentation of information changes interpretation. | The problem is how the same fact is framed, not only how easily it is remembered. |

| Availability bias | Easy-to-recall information receives too much weight. | The problem is treating vivid or recent evidence as if it were representative. |

Availability bias FAQ

Is availability bias always harmful for investors?

No. Easily recalled information can sometimes point to a real risk or opportunity. The issue is whether that information receives too much weight before broader evidence is reviewed.

What is the difference between availability bias and recency bias?

Recency bias emphasizes the newest information. Availability bias is broader: recent information can be available, but so can vivid, familiar, repeated, or emotionally memorable information.

How can an investor check for availability bias?

The simplest check is to ask what evidence came to mind first, what evidence was ignored, and whether the visible evidence represents the broader record relevant to the investment decision.

The useful test

Availability bias becomes easier to manage when the investor separates memory from evidence quality. A fact that is vivid, recent, or familiar may still matter, but it earns its weight through relevance and representativeness, not only through ease of recall.