Framing bias is a decision bias where the way information is presented changes how an investor interprets the same underlying evidence. The investor risk is not only that the facts are misunderstood, but that a gain/loss frame, risk/opportunity frame, or comparison baseline changes the review before the evidence is restated neutrally.

A frame can make one result feel defensive, another feel attractive, and another feel urgent even when the underlying data has not changed much. In an investing context, this can affect how someone reads valuation, earnings changes, portfolio drawdowns, risk disclosures, or position-review notes.

Key Points

- Framing bias occurs when presentation changes judgment even when the underlying evidence is similar.

- In investing, frames can shift attention toward losses, gains, risk, opportunity, percentages, dollar amounts, or comparison baselines.

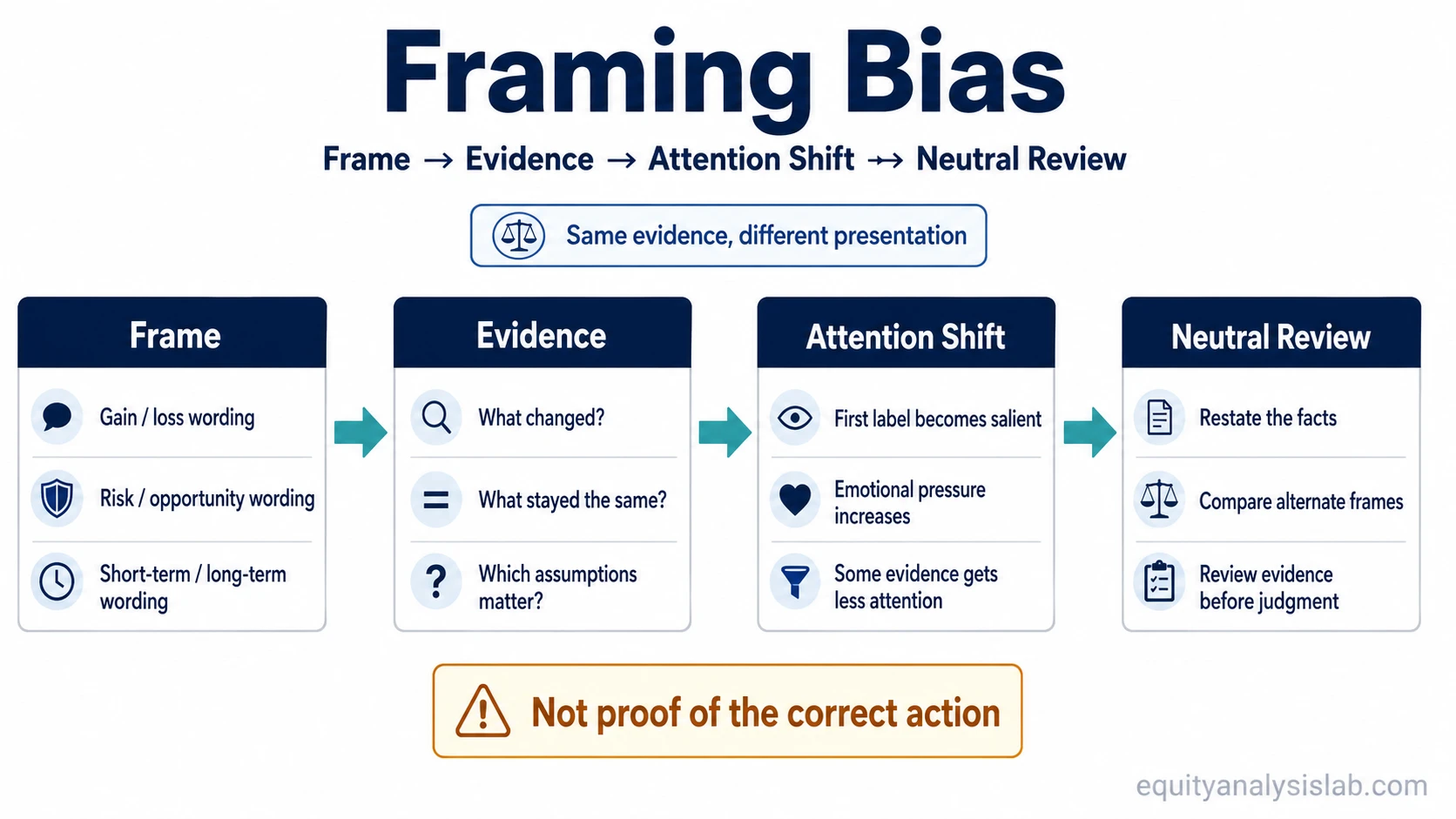

- A framing review restates the evidence neutrally; it does not prove which investment action is correct.

What Framing Bias Means

Framing bias means that the same or similar information can lead to different judgments depending on how it is described, ordered, compared, or emphasized. The related term “framing effect” is often used for the same basic decision problem.

The core issue is presentation versus evidence. A fact framed as “a 20% decline from the recent high” may feel different from the same fact framed as “a return to last year’s valuation range.” A company described as “missing expectations by a small margin” may be interpreted differently from the same result described as “preserving most of its earnings base despite pressure.” The evidence still needs to be checked, but the frame can change which part of the evidence receives attention first.

Framing bias is part of behavioral finance because it affects interpretation before the investor has fully separated facts, assumptions, and emotional response. It is not automatically irrational to respond differently to different descriptions. The bias risk appears when the presentation becomes more influential than the evidence underneath it.

How Framing Bias Changes Investor Decisions

In investor review, framing bias often starts with the first label attached to the information. A report described as “resilient margins” can pull attention toward stability. The same report described as “margin compression remains unresolved” can pull attention toward risk. Both frames may contain useful information, but neither should replace a neutral review of revenue, margins, cash flow, balance-sheet position, valuation, and forward assumptions.

Gain/loss framing can be powerful because investors can react differently to information presented as avoiding loss versus achieving gain. A portfolio position described as “still down 15%” can create a different reaction than the same position described as “up 10% from the review date.” Neither frame alone answers whether the thesis has improved, weakened, or stayed uncertain.

Risk/opportunity framing works in a similar way. A lower valuation can be described as “cheaper than before” or “reflecting weaker expectations.” The useful review question is not which phrase sounds more persuasive. The useful question is what evidence supports the implied interpretation.

Review principle: A framing review does not remove judgment. It slows the decision down long enough to compare the frame with the evidence underneath it.

Framing Bias Examples in Investing

Framing bias is easiest to see when the facts stay similar but the description changes. The same information can be framed through losses, gains, risk, opportunity, time horizon, percentage change, dollar change, or comparison baseline.

| Frame | How it can sound | Neutral review question |

|---|---|---|

| Gain/loss frame | The position is still below the original purchase price. | Has the investment thesis changed since the purchase? |

| Risk/opportunity frame | The lower valuation creates upside or signals weaker expectations. | Which evidence supports opportunity, and which evidence supports risk? |

| Percentage/dollar frame | A small percentage move may still be a large dollar effect in a concentrated holding. | Which measure better reflects portfolio impact? |

| Short-term/long-term frame | A quarterly disappointment may look severe or temporary depending on the time frame used. | Is the issue temporary noise, thesis damage, or unresolved uncertainty? |

| Positive/negative wording frame | The same result can be described as “resilient” or “not yet recovered.” | What did the data actually show before the label was added? |

Example: Suppose a company reports flat revenue, slightly lower margins, and stable free cash flow. One investor note frames the result as “margin pressure continues.” Another frames it as “cash generation remains intact.” Both descriptions can be partly true. A neutral review separates the frame from the evidence by asking whether margin pressure is temporary, whether cash flow quality is durable, and whether valuation already reflects either interpretation.

Framing Bias Review Checklist

A practical framing review does not ask the investor to ignore the original presentation. It asks the investor to restate the same issue in more than one way before treating the frame as decisive.

| Checklist step | Question to ask | Decision risk reduced |

|---|---|---|

| Identify the frame | Is the information being framed as gain, loss, risk, opportunity, short-term, or long-term? | Reacting to presentation before reviewing evidence. |

| Restate the evidence | What facts remain if emotional wording and comparison labels are removed? | Letting labels replace analysis. |

| Compare opposite frames | How would the same evidence look if framed from the opposite side? | Accepting only the first interpretation. |

| Check the baseline | What comparison point is being used, and is it still relevant? | Relying on an outdated or selective reference point. |

| Separate action from review | Does the frame prove an action, or does it only identify what needs review? | Turning framing awareness into a false investment signal. |

How to Review a Framed Investment Decision

A framed decision can be reviewed without assuming that the decision is wrong. The goal is to test whether the investor is responding to the facts or to the presentation of the facts.

The review can start with four neutral steps. First, rewrite the statement without emotional labels. Second, separate the facts from the interpretation. Third, express the same information in at least one alternative frame. Fourth, ask what evidence would support or weaken each interpretation.

Frame: How is the information being presented?

Evidence: What facts, assumptions, or metrics sit underneath the presentation?

Attention shift: What part of the decision does the frame make more noticeable?

Neutral review: What question would still matter if the information were presented in the opposite way?

Framing bias often works before a full checklist begins. That is why the first step is not to debate the conclusion. The first step is to notice what the presentation made salient.

Framing Bias vs Related Behavioral Biases

Framing bias can overlap with other investor decision biases, but the source of the problem is different.

| Bias | Main decision problem | How it differs from framing bias |

|---|---|---|

| anchoring bias | The investor relies too heavily on a fixed reference point. | Framing bias is about presentation; anchoring bias is about the reference point that receives too much weight. |

| availability bias in investor decisions | The investor overweights information that is easier to recall. | Framing bias changes how the same evidence is presented; availability bias changes which evidence feels most accessible. |

| confirming an existing investment thesis | The investor favors evidence that supports an existing view. | Framing bias can occur before thesis filtering begins, because the first presentation already shapes attention. |

Limits of Framing Bias Review

Framing bias review is not investment advice. Identifying a frame does not prove that a stock should be bought, sold, held, avoided, resized, or added to a portfolio. It only shows that the presentation of information may be affecting interpretation.

A frame can be misleading, but it can also highlight a real issue. A risk frame may correctly point to deteriorating evidence. An opportunity frame may correctly point to valuation improvement. The review problem is not that every frame is wrong. The problem is that the frame should not be allowed to replace the evidence.

Framing review is most useful when it improves decision discipline. It helps the investor slow down, restate the facts, compare alternative interpretations, and separate emotional reaction from evidence review.

FAQ

What is framing bias in investing?

Framing bias in investing occurs when the presentation of information changes how an investor interprets the same underlying evidence. A gain/loss frame, risk/opportunity frame, or short-term/long-term frame can shift attention before the facts are reviewed neutrally.

How is framing bias different from anchoring bias?

Framing bias is about how information is presented. Anchoring bias is about relying too heavily on a fixed reference point, such as a prior price, estimate, target, or valuation level.

How can investors review framing bias without assuming the decision is wrong?

They can restate the same evidence in neutral language, compare alternative frames, separate facts from interpretation, and ask which assumptions changed. This review checks the decision process without claiming that any specific action is correct.