A diagonal spread is an options spread that combines different strike prices with different expiration dates. That structure makes it different from a vertical spread, which changes strike but keeps expiration the same, and from a calendar spread, which changes expiration but keeps the strike the same.

The diagonal structure usually pairs a longer-dated option with a shorter-dated option on the same underlying. Because one leg can expire before the other, the spread is not only a simple expiration payoff shape. Its value can also depend on remaining extrinsic value, implied volatility, time decay, liquidity, and short-leg assignment or exercise risk.

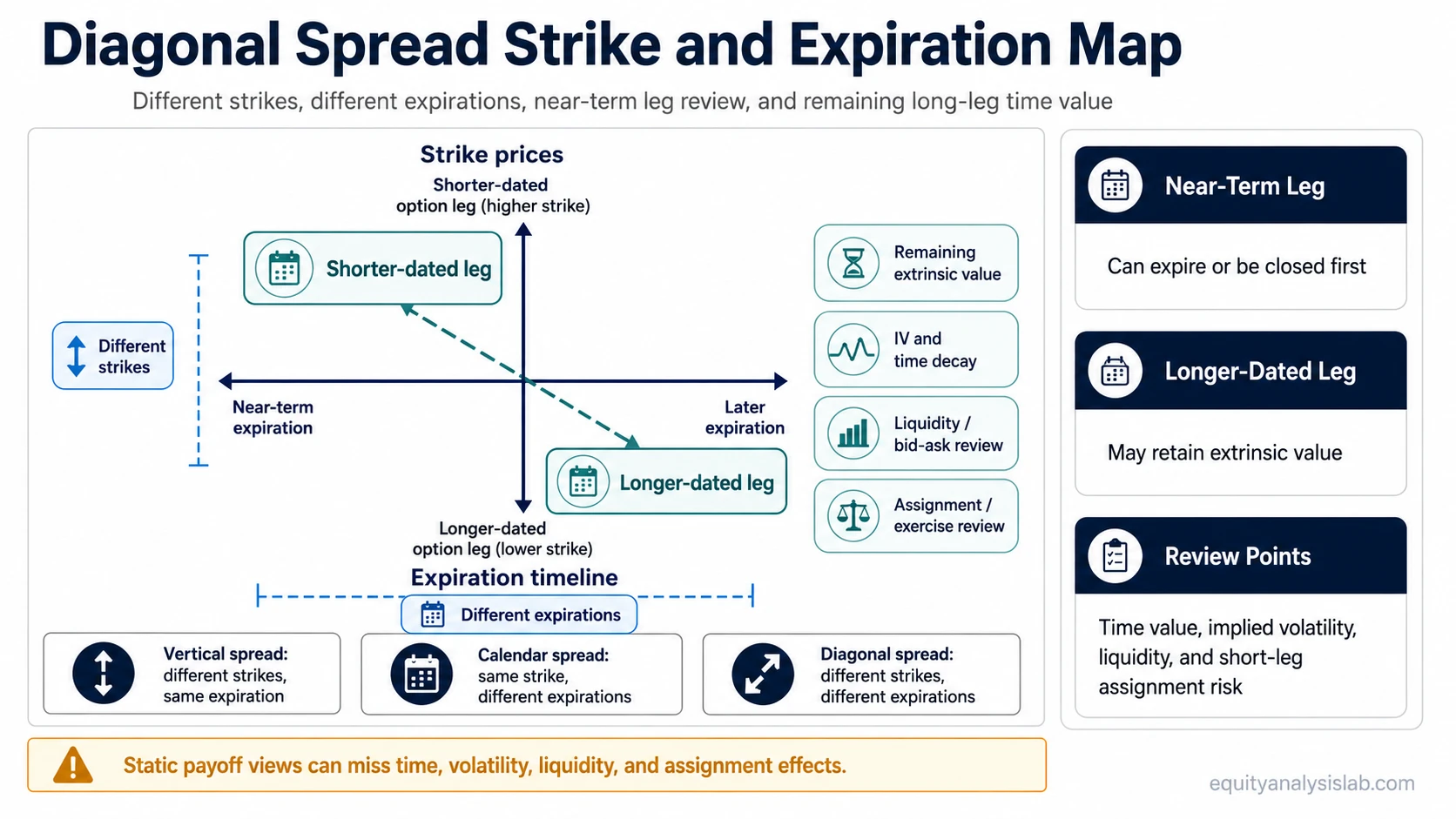

What Is a Diagonal Spread?

A diagonal spread is a multi-leg options position built with options that have both different strikes and different expiration dates. The name comes from the way the legs differ across two dimensions at once: strike price and time to expiration.

In a common structure, the longer-dated leg keeps exposure after the shorter-dated leg expires. The shorter-dated leg can collect or define part of the premium relationship, but it also introduces timing and assignment considerations. For that reason, a diagonal spread is best understood as a strike-and-expiration structure, not simply as a debit spread, credit spread, bullish spread, or bearish spread.

- Strike dimension: the legs are placed at different strike prices.

- Expiration dimension: the legs expire on different dates.

- Time dimension: the shorter-dated leg can expire while the longer-dated leg still has time value.

- Risk dimension: payoff, implied volatility exposure, liquidity, and assignment risk can change before the final expiration.

How a Diagonal Spread Works

A diagonal spread normally uses two options from the same option type family, such as two calls or two puts. One leg has a longer expiration, and the other has a shorter expiration. The strikes are not the same, which separates the structure from a calendar spread.

A long diagonal often involves buying the longer-dated option and selling the shorter-dated option at a different strike. A short diagonal reverses that premium and exposure relationship. The exact debit or credit depends on the strikes, expirations, implied volatility, and option prices at the time the spread is opened.

Call diagonals and put diagonals are structural variants. A call diagonal uses call options; a put diagonal uses put options. That distinction does not make either version a recommendation or a forecast. It only describes which option type is used to build the spread.

Diagonal Spread vs Vertical Spread vs Calendar Spread

The fastest way to separate a diagonal spread from nearby spread types is to check what changes: strike, expiration, or both.

| Spread type | Strike prices | Expiration dates | Main structural idea | Payoff interpretation |

|---|---|---|---|---|

| Vertical spread | Different strikes | Same expiration | Defines an expiration payoff range between two strikes. | Usually cleaner at expiration because both legs expire together. |

| Calendar spread | Same strike | Different expirations | Separates near-term and longer-term time value at the same strike. | More dependent on time decay and volatility around the shared strike. |

| Diagonal spread | Different strikes | Different expirations | Combines a vertical-style strike difference with a calendar-style expiration difference. | Less clean than a simple vertical because the later-expiring leg can retain extrinsic value after the short leg expires. |

This is why a diagonal spread sits between vertical and calendar logic. It has the strike separation of a vertical spread, but it also has the time separation of a calendar spread.

Debit, Credit, and Payoff Boundary

Debit and credit describe how premium moves when the spread is opened. They do not define the structure by themselves. A diagonal spread can be opened for a net debit or a net credit depending on the strikes, expirations, option type, and volatility environment.

The payoff boundary is usually less straightforward than a same-expiration vertical spread. In a vertical spread, both legs expire together, so the expiration value can often be described directly from the distance between strikes and the premium paid or received. In a diagonal spread, the shorter-dated leg may expire first while the longer-dated leg still has time value. That remaining value can change with implied volatility, underlying price movement, and time left to expiration.

For long diagonals, the best-case outcome is often not a fixed number that can be known with the same simplicity as a basic vertical spread at entry. A static payoff diagram can help describe the structure, but the actual value depends on what the longer-dated option is worth when the shorter-dated option expires or is closed.

Why a Diagonal Spread Payoff Diagram Can Be Misleading

A diagonal spread payoff diagram can show the static shape of the structure, but it can understate how the position changes when the short leg expires first, implied volatility moves, liquidity is thin, or assignment risk appears.

| Risk driver | Why it matters | Mistaken assumption to avoid |

|---|---|---|

| Expiration sequence | The short-dated leg can expire while the long-dated leg still has value. | Do not treat the spread as if both legs always resolve at the same time. |

| Remaining extrinsic value | The longer-dated option may still contain time value after the near-term leg expires. | Do not assume the expiration payoff is only intrinsic value between strikes. |

| Implied volatility | Changes in implied volatility can affect the longer-dated option differently from the shorter-dated option. | Do not treat the spread as a pure directional position. |

| Time decay | Time decay can help one leg and hurt the other depending on structure and timing. | Do not assume time decay is automatically favorable. |

| Assignment or exercise risk | A short option can create assignment risk, especially near expiration or when early exercise incentives exist. | Do not ignore the short leg just because the position is part of a spread. |

| Liquidity and bid-ask spread | Multi-leg structures can be harder to price and adjust when markets are wide or thin. | Do not assume displayed theoretical value is the same as executable value. |

Time Decay and Implied Volatility Exposure

Time decay in a diagonal spread is mixed because the legs have different expirations. The shorter-dated option usually loses time value faster, while the longer-dated option keeps more remaining extrinsic value. That can be useful for understanding the structure, but it does not make time decay automatically favorable.

Implied volatility also matters because the longer-dated leg can respond differently from the shorter-dated leg. If implied volatility falls, the remaining long-dated option may lose value even if the underlying price movement looks directionally reasonable. If implied volatility rises, the long-dated leg may retain more value, but the short leg and exit conditions still matter.

The practical point is that a diagonal spread is not only a price-direction structure. It combines price, time, volatility, and execution conditions.

Simple Illustrative Example

Assume an investor reviews two call options on the same underlying. One call expires in a later month and has a lower strike. Another call expires sooner and has a higher strike. Combining those two calls creates a diagonal structure because both the strike and expiration are different.

The initial read may be tempting because the shorter-dated call can offset part of the longer-dated call’s cost. That read is incomplete unless the investor also considers what happens when the short call expires, what the long call may still be worth, whether implied volatility changes, and whether the short call creates assignment or exercise risk.

A stronger interpretation separates structure from outcome: the diagonal spread defines a relationship between two option legs, but it does not guarantee a clean maximum profit, a fixed risk experience, or a simple one-date payoff like a same-expiration vertical spread.

How Diagonal Spreads Relate to Other Spread Structures

Diagonal spreads should not be mixed up with same-expiration vertical spreads. A bull call spread, for example, is a debit-style vertical structure that uses different call strikes with the same expiration. A put credit spread such as a bull put spread also uses the same-expiration vertical framework, but with put options and net credit logic.

A bear put spread is another same-expiration vertical structure. The distinction is structural: a diagonal spread changes both strike and expiration instead of only changing strike inside one expiration cycle.

FAQ

What makes a spread diagonal?

A spread is diagonal when the option legs have different strike prices and different expiration dates. The structure combines a vertical-style strike difference with a calendar-style expiration difference.

Is a diagonal spread the same as a calendar spread?

No. A calendar spread uses the same strike with different expirations. A diagonal spread uses different strikes and different expirations.

Can a diagonal spread be a debit or a credit?

Yes. Debit or credit describes the net premium paid or received. Diagonal describes the structure of different strikes and different expirations.

Why is maximum profit harder to define in a diagonal spread?

The shorter-dated leg can expire before the longer-dated leg, leaving remaining extrinsic value in the later-expiring option. That value can depend on price, time, implied volatility, and liquidity at the time the near-term leg is resolved.

Does the short leg create assignment risk?

It can. A short option inside a diagonal spread may carry assignment or exercise risk, especially near expiration or when early exercise incentives are present. The spread structure does not remove the need to review the short leg.