Compounding is the process where gains are added back to a base, so future gains are calculated on a larger amount. In investing, the concept is useful only when the return source, reinvestment pattern, time horizon, costs, losses, dilution, and assumptions are understood realistically.

Definition: Compounding means that earnings, interest, returns, or reinvested gains become part of the base that future gains are measured from. The base grows first, then the next return applies to that larger base.

The arithmetic is straightforward, but the investor interpretation depends on whether gains are retained, reinvested well, and protected from costs, losses, dilution, or weak assumptions. A larger base can improve the future growth path, but only if the gains are retained or reinvested and if later results do not erase, dilute, or overstate the base being compounded.

What compounding means

Compounding describes a growth process, not a guaranteed result. The starting point can be cash, invested capital, retained earnings, portfolio value, or another base. When gains remain inside that base, the next period begins from a larger amount than before.

Compound interest is one familiar form of compounding, but investing compounding is broader. A company may compound business value when retained earnings are reinvested well. A portfolio can compound when returns are retained instead of withdrawn. An investment thesis can also fail to compound if the underlying returns are weak, unstable, or offset by costs and dilution.

Core idea: compounding is base expansion. The key question is not only whether time passes, but whether the base grows in a durable way and whether future returns are applied to that larger base.

How compounding works

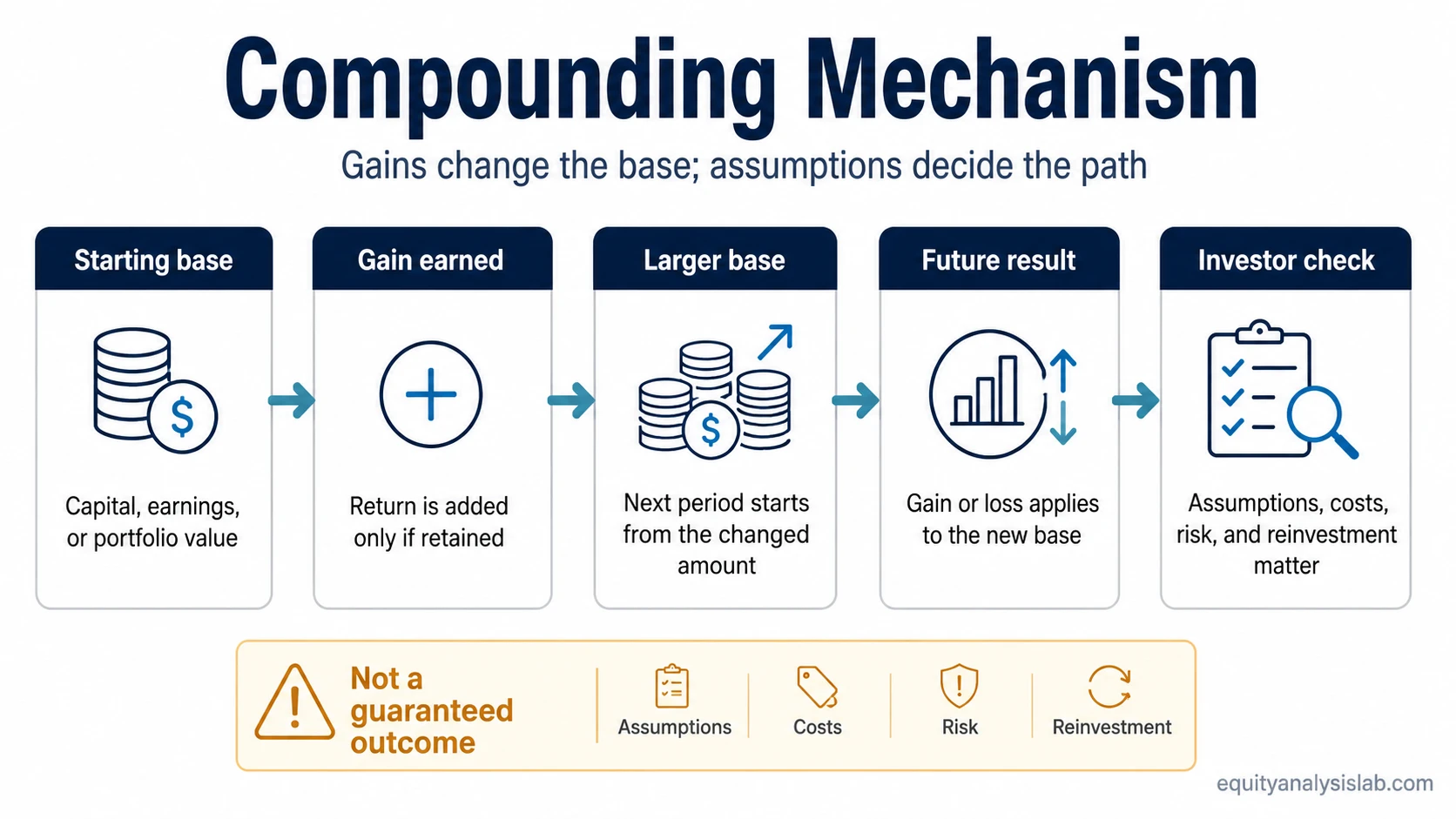

The mechanism has three parts: the base earns a return, the gain is added to the base, and the next return is calculated on the larger base. Time matters because the process can repeat, but time alone is not enough. The quality of the return and the treatment of gains decide whether the compounding path remains useful.

Mechanism sequence: starting base → earned gain → larger base → future gain on the larger base → repeated outcome path if gains are retained and assumptions hold.

A simple interest-style example makes the arithmetic visible. If a $100 base earns 5%, the base becomes $105 if the gain is retained. If the same 5% applies again, the next gain is calculated on $105, not only on the original $100. That illustrates the mechanism, not a promised investment outcome.

For an investor, the same structure can appear through reinvested dividends, retained company earnings, portfolio returns, or capital allocated into productive assets. The important test is whether future gains are being generated by a stronger base or merely by optimistic assumptions.

Simple growth vs compound growth

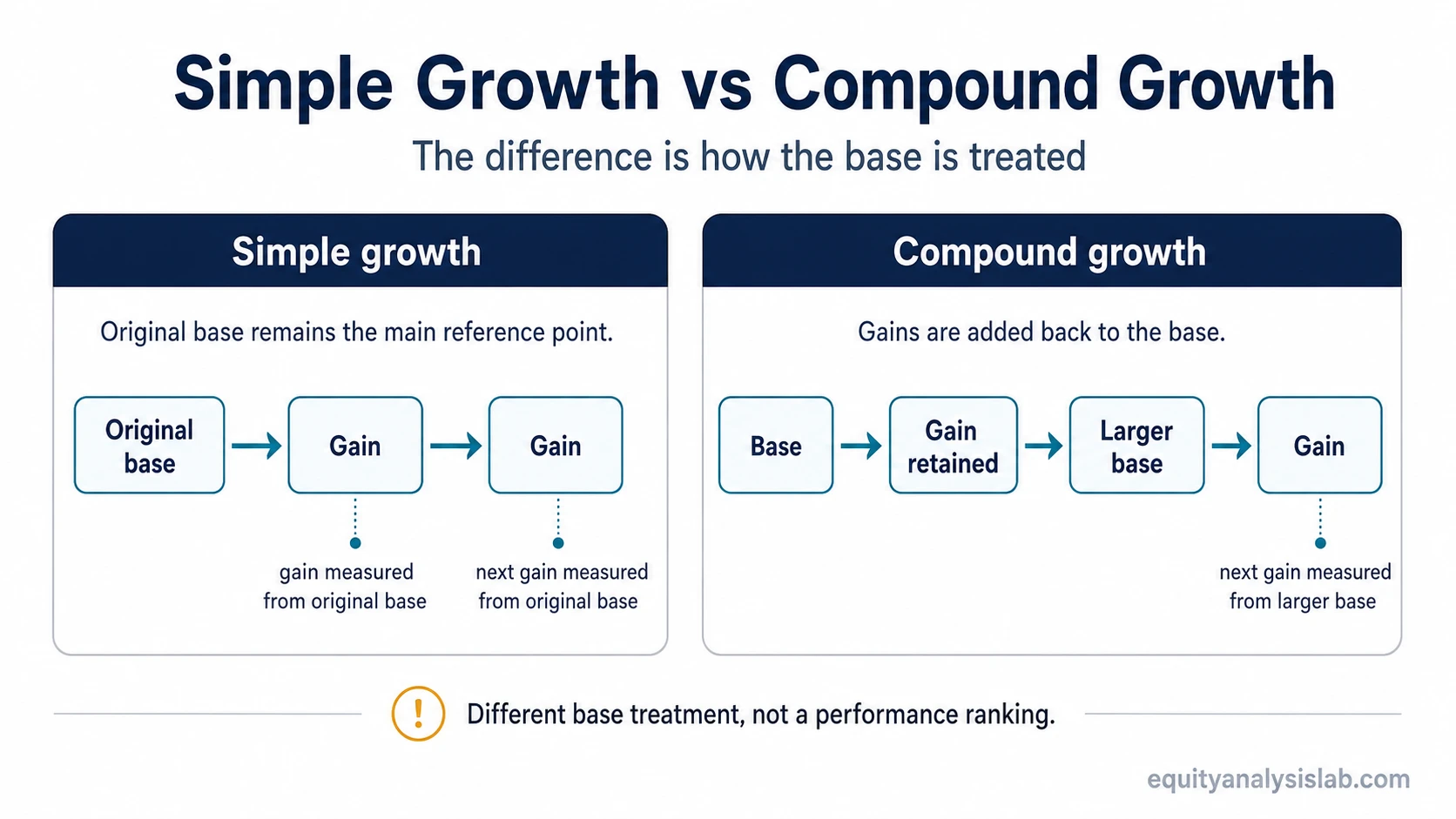

Simple growth and compound growth differ in what future gains are measured against. Simple growth uses the original base as the reference point. Compound growth updates the base after gains are added back.

| Growth pattern | How the base is treated | Investor interpretation |

|---|---|---|

| Simple growth | Future gains are measured mainly against the original base. | Useful for understanding linear increases, fixed payments, or non-reinvested gains. |

| Compound growth | Gains are added to the base, so later gains are measured from a larger amount. | Useful for understanding reinvestment, retained earnings, and long-term outcome paths. |

The distinction matters because compound growth can change the shape of the outcome path. Early differences may look small, while later differences can become larger if gains are retained and future returns remain positive. The same structure can also magnify negative effects when losses, fees, interest costs, or dilution reduce the base.

What affects compounding for investors

Compounding depends on inputs. A chart or formula can show the shape, but the quality of the assumptions determines whether the result is meaningful. Investors usually need to examine the base, the expected return, the time horizon, and the frictions that can weaken the path.

| Input | Why it matters | Common mistake |

|---|---|---|

| Starting base | A larger or smaller base changes the amount that future gains apply to. | Focusing only on the rate while ignoring the size and quality of the base. |

| Return or earnings rate | The rate determines how quickly the base can grow under the stated assumptions. | Treating an assumed rate as certain instead of conditional. |

| Reinvestment pattern | Gains must usually remain in the base for compounding to continue. | Assuming compounding continues even when gains are withdrawn or poorly reinvested. |

| Time horizon | More periods allow the mechanism to repeat, but only if the base survives and keeps earning. | Believing time automatically solves weak returns or poor risk control. |

| Costs, taxes, fees, or dilution | Friction can reduce the base or reduce the rate that actually reaches the investor. | Looking at gross growth while ignoring what remains after friction. |

| Losses and volatility | Losses reduce the base that future gains are applied to. | Ignoring downside compounding when outcomes are negative. |

Expected return assumptions are especially important because compounding calculations can look precise even when the input is uncertain. A small change in the assumed rate can produce a much different long-term path.

A realistic time horizon also changes the interpretation. A long horizon gives the mechanism more periods to work, but it also creates more time for business risk, valuation change, fees, inflation, and investor behavior to affect the result.

Why compounding matters in investing

Compounding matters because investment outcomes often depend on what happens after the first gain. If gains are retained and future returns are earned on a larger base, the path can become meaningfully different from a one-period return.

The investor version of compounding is not only about arithmetic. It depends on what is being compounded. Durable earnings, cash-flow-supported growth, disciplined reinvestment, and sensible capital allocation can make the base more reliable. Weak earnings quality, excessive dilution, poor reinvestment, or unrealistic assumptions can make the apparent compounding path less useful.

In equity investing, compounding can appear at more than one level. A business may reinvest earnings. A shareholder may reinvest dividends. A portfolio may retain gains. Each layer depends on different assumptions, so the word “compounding” should not be treated as proof that value is being created.

Why compounding is not a guarantee

Compounding can improve an outcome path when the base keeps growing, but it can also work against an investor. Debt interest can compound. Fees can compound. Losses reduce the base. Dilution can spread future earnings across more shares. Poor reinvestment can turn retained capital into a weaker business rather than a stronger one.

Limitation: compounding is a mechanism, not a decision rule. It does not prove that an investment is attractive, that returns will continue, or that a longer holding period will fix weak assumptions.

The most common misuse is treating a clean compound growth curve as if it were evidence. A curve is only as reliable as the assumptions behind it. If the return rate is too high, if costs are ignored, or if losses are excluded, the result may describe a spreadsheet more than a realistic investment path.

That is why compounding belongs next to risk and return. The upside path and downside path both matter. A gain that compounds from a larger base can materially change the path, but a loss from a larger base also changes the amount of capital that must recover.

A short compounding example

Assume a $100 base earns 5% and the gain remains in the base. The next period starts at $105. If another 5% return occurs, the gain is $5.25 rather than $5 because the return applies to $105. The extra $0.25 is the effect of earning on the prior gain.

The example is intentionally simple. It does not describe a real market return, a recommended investment, or a guaranteed path. It only isolates the mechanism: retained gains increase the base, and a larger base changes the size of future gains or losses.

When contributions are added over time, dollar-cost averaging becomes a separate concept. Contributions change the base, while compounding describes how retained gains can make future gains apply to a larger amount.

Related investing concepts

Several nearby concepts help clarify compounding without replacing it.

| Concept | How it connects to compounding |

|---|---|

| Expected return | Defines the assumed rate used in a compounding path, but the assumption needs uncertainty and realism. |

| Risk and return | Frames the possibility that the base can shrink, not only grow. |

| Time horizon | Sets the number of periods over which compounding may repeat. |

| Dollar-cost averaging | Changes the invested base through contributions, which is different from gains compounding on the existing base. |

| Equity investing | Places compounding inside the broader question of business ownership, earnings quality, and reinvestment. |

Compounding FAQ

Is compounding the same as compound interest?

No. Compound interest is one form of compounding. Compounding in investing can also involve reinvested dividends, retained earnings, portfolio gains, or any process where gains are added back to a base and future gains are measured from that larger base.

Why does time matter for compounding?

Time matters because it allows the base-growth process to repeat. More periods can make the effect larger, but only if the base keeps earning and gains are retained instead of being withdrawn, lost, or offset by friction.

Can compounding work against an investor?

Yes. Losses, debt interest, fees, taxes, poor reinvestment, and dilution can also compound or reduce the base. Compounding describes how a base changes over time; it does not guarantee that the change is favorable.