Representativeness bias is a mental shortcut where a situation is judged by how much it resembles a familiar pattern, prototype, or story. In investing, it can make a stock, sector, or thesis feel stronger before the business, valuation, risk, and portfolio evidence have been tested.

Definition: Representativeness bias occurs when resemblance is treated as evidence. An investor may see a company that looks like a past winner, a sector story that feels familiar, or a management narrative that resembles a successful case, and then accept the idea too quickly because the pattern feels recognizable.

The issue is not pattern recognition itself. Investors need patterns to organize information. The risk appears when recognition lowers the standard of proof. A familiar-looking idea still needs evidence on business quality, earnings durability, valuation, balance-sheet risk, competitive position, and portfolio fit.

Key Points

- Representativeness bias can make resemblance feel like proof before the evidence has been tested.

- For investors, the shortcut often appears when a stock resembles a past winner, a familiar sector cycle, or a “quality company” story.

- The main risk is not optimism; it is accepting an idea before reviewing base rates, valuation, contrary evidence, and portfolio exposure.

- A written checklist helps separate useful pattern recognition from premature thesis acceptance.

What Representativeness Bias Means for Investors

For investors, representativeness bias means an idea can feel more believable because it fits a familiar category. A fast-growing company may resemble an earlier compounder. A turnaround story may resemble a past recovery. A sector may look like it is entering a cycle investors have seen before.

That resemblance can be useful as a starting point, but it is not enough to accept the conclusion. The current company may have a different margin structure, different capital needs, different dilution risk, different competitive pressure, or a different valuation starting point. The story can sound similar while the evidence is materially different.

The practical question is not whether the idea reminds the investor of something. The question is whether the evidence still supports the conclusion after the familiar comparison is removed.

Investor test: If the idea becomes much weaker when the familiar comparison is removed, the decision may be relying more on resemblance than on evidence.

How Resemblance Can Replace Evidence Review

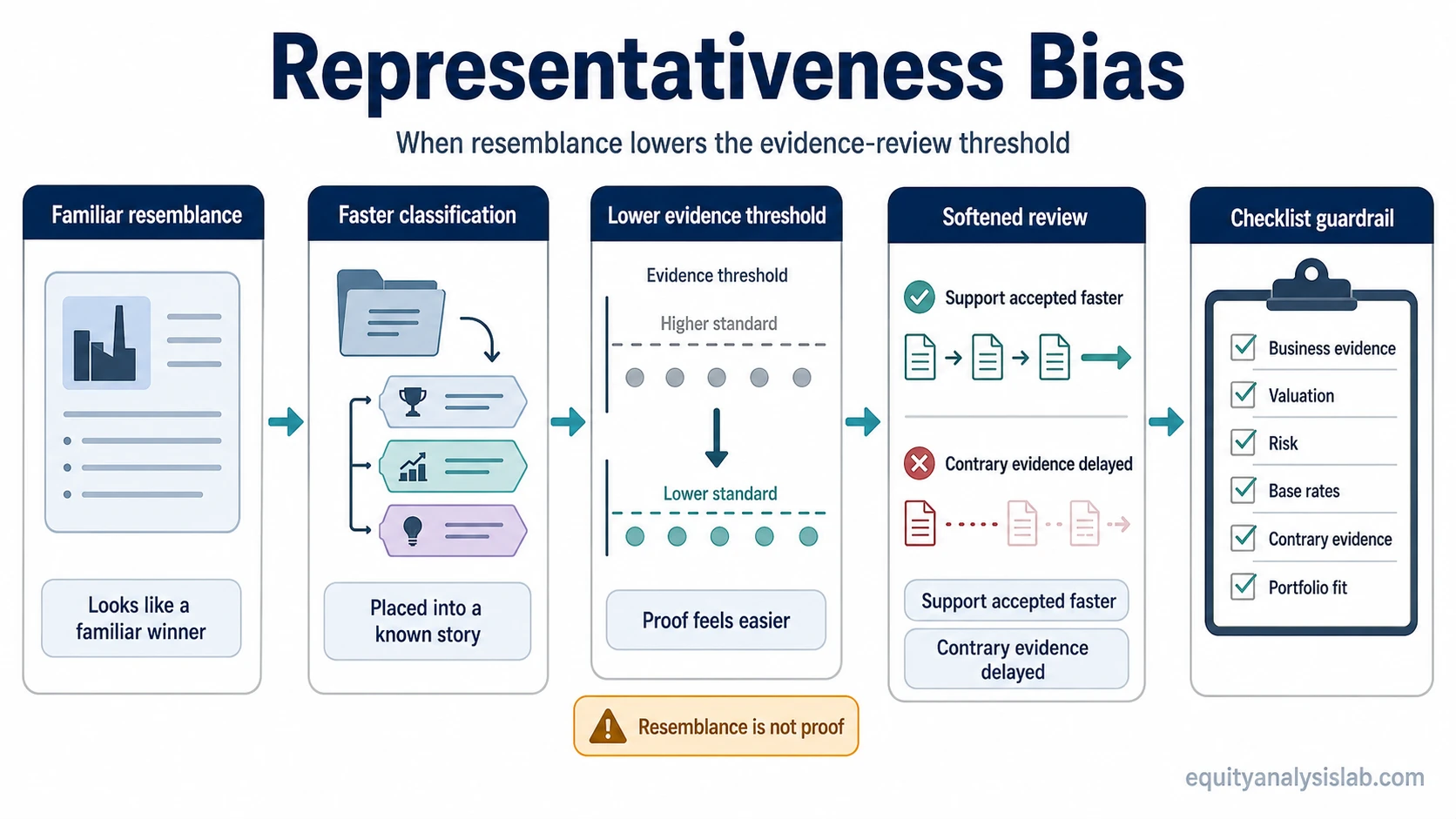

Representativeness bias often follows a simple sequence: a familiar story is recognized, the idea is classified quickly, the required proof feels lower, and contrary information receives less attention. The investor may still believe the process was thorough, even though the conclusion arrived before the facts were tested.

In an investment process, that sequence can look like this:

Familiar pattern: “This looks like a past winner.”

Faster classification: The idea is mentally placed into a successful category.

Lower evidence threshold: Supportive facts feel more convincing because they match the story.

Softened review: Valuation, base rates, balance-sheet risk, or contrary evidence may be delayed or explained away.

The investor may not be ignoring information deliberately. The recognizable story can simply change how much proof feels necessary before the thesis is accepted.

Investor Checklist: Where the Bias Shows Up

Representativeness bias is easier to detect when the process focuses on observable decision points. The issue is not the presence of a familiar story; the issue is whether that story changes the evidence standard.

| Decision trigger | Evidence likely to be overweighted | Evidence likely to be ignored | Checklist step at risk | Review guardrail |

|---|---|---|---|---|

| A company resembles a past compounder | Revenue growth, brand story, management language, market opportunity | Margins, cash conversion, dilution, competitive pressure, valuation multiple | Business quality and valuation review | Test whether current unit economics and cash flow support the comparison |

| A sector story resembles a previous cycle | Headlines, early price strength, familiar macro narrative | Balance-sheet risk, demand durability, cost pressure, cycle maturity | Base-rate and cycle-context review | Compare the current setup with multiple prior outcomes, not one memorable case |

| A turnaround resembles a successful recovery | New leadership, cost cuts, optimistic guidance, early operational improvement | Debt load, execution risk, customer retention, margin sustainability | Contrary-evidence review | Write the conditions that would weaken the turnaround thesis before accepting it |

| A familiar quality-company label is applied quickly | High margins, recognizable product, strong narrative, historical reputation | Forward growth risk, reinvestment needs, valuation compression, changing competition | Current thesis evidence review | Separate the company’s reputation from the current investment evidence |

| Position size becomes easier to justify | Confidence from the recognizable story | Portfolio concentration, downside scenario, thesis invalidation, review date | Portfolio risk review | Check whether sizing is based on evidence quality or resemblance-driven confidence |

Practical Investor Scenario

Example: An investor studies a fast-growing company with a strong product story and high customer enthusiasm. The company reminds the investor of an earlier market winner. Because the resemblance feels strong, the investor focuses on the growth narrative, management tone, and brand potential.

The risk is that the comparison may make the idea feel tested before the work is complete. The investor still needs to examine margins, cash flow, reinvestment needs, share dilution, valuation, competitive pressure, and the conditions that would weaken the thesis.

This scenario does not mean the company is weak or that the thesis is wrong. It shows how resemblance can move ahead of evidence. The same initial pattern can lead to different investment conclusions depending on the facts.

What Representativeness Bias Is Not

Not the same as optimism: An investor can be optimistic after reviewing evidence carefully. Representativeness bias is about accepting the thesis too quickly because the idea resembles a familiar story.

Not proof that the decision is wrong: A familiar-looking investment can still be attractive. The bias concerns the review process, not the final outcome.

Not a reason to ignore patterns: Pattern recognition can help investors organize information. The problem starts when the pattern replaces evidence, base rates, valuation work, or contrary-evidence review.

A disciplined process does not remove pattern recognition. It slows down the point where the pattern becomes a conclusion.

Representativeness Bias vs Nearby Biases

Representativeness bias often overlaps with other behavioral biases, but the trigger is specific: the idea feels convincing because it resembles a familiar category. The distinction matters because each bias needs a different review question.

| Bias | Main trigger | Investor review question |

|---|---|---|

| Availability bias | The information is easy to recall | Am I overweighting this because it is recent, vivid, or easy to remember? |

| Confirmation bias | The information supports an existing belief | Am I looking for evidence that supports the thesis more than evidence that could weaken it? |

| Overconfidence bias | Confidence rises faster than evidence quality | Has my conviction increased without a matching increase in tested evidence? |

| Recency bias | Recent information receives too much weight | Am I treating the latest pattern as more durable than the evidence supports? |

| Anchoring bias | An initial number, price, estimate, or reference point shapes later judgment | Am I still relying on the first reference point after new evidence has appeared? |

The shortest distinction is this: representativeness bias asks whether the idea was accepted because it looked like a familiar type. Availability bias asks whether the idea came to mind too easily. Confirmation bias asks whether the investor searched for support after already leaning toward the thesis.

How Investors Can Reduce the Risk

The goal is not to eliminate intuition. The goal is to keep intuition from finishing the work before the evidence has been tested. A written checklist makes the investment process slower at the exact point where resemblance can create premature confidence.

Write the thesis before the conclusion: State the business evidence, valuation evidence, risk evidence, and portfolio role separately before deciding whether the idea fits.

Check base rates: Ask how often similar-looking companies, sectors, or turnarounds have produced different outcomes. One familiar success story should not become the whole reference class.

List contrary evidence: Identify facts that would weaken the thesis, including margin pressure, dilution, balance-sheet risk, slowing growth, competitive changes, or valuation risk.

Separate valuation from story: A company can resemble a high-quality business while still being priced for assumptions that require careful testing.

Review sizing pressure: If the familiar comparison makes a larger position feel easier to justify, check whether position size is being driven by evidence quality or by resemblance-driven confidence.

Schedule a review date: A review date reduces the risk that the original story keeps controlling the thesis after new evidence appears.

A useful guardrail is to ask: “What evidence would still support this idea if the familiar comparison were removed?” If the answer is thin, resemblance may be doing too much of the work.

Why Base Rates Matter

Base rates help counter representativeness bias because they widen the comparison set. Instead of comparing one company to one memorable winner, the investor asks how similar-looking situations have behaved under different conditions.

That does not require a perfect statistical model. Even a simple base-rate question can improve the process: “How many companies with this profile actually sustained the growth, margins, reinvestment returns, and valuation needed for the thesis?” The question shifts attention from resemblance to evidence.

Common mistake: Using one memorable success story as the reference class. A stronger review compares the current thesis against a wider set of outcomes, including failures, slower-growth cases, and companies that looked similar at first but later proved different.

FAQ

Is representativeness bias always harmful?

No. Pattern recognition can be useful when it helps an investor organize information. The risk appears when resemblance replaces evidence review or lowers the standard for accepting a thesis.

How is representativeness bias different from availability bias?

Representativeness bias is driven by resemblance to a familiar pattern or prototype. Availability bias is driven by information that is easy to recall, such as a recent headline, vivid example, or memorable market story.

How can investors reduce representativeness bias?

Investors can reduce the risk by writing the thesis evidence before the conclusion, checking base rates, listing contrary evidence, separating valuation from story, reviewing sizing pressure, and scheduling a later review.