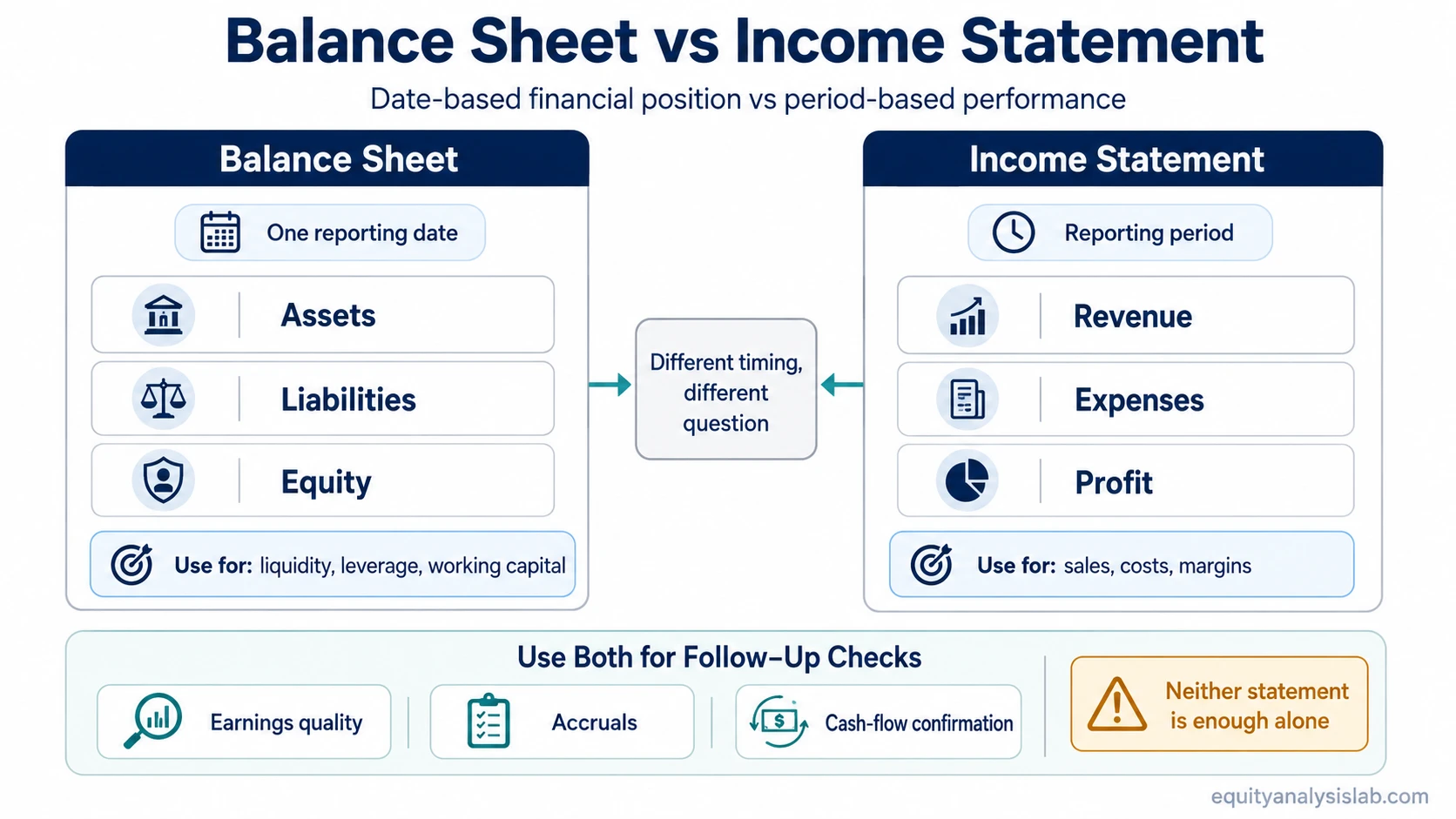

A balance sheet shows a company’s financial position at one specific date; an income statement shows how the company performed over a period. Investors compare them because one shows what the company owns and owes, while the other shows how revenue, expenses, and profit developed during the reporting period.

Balance sheet: A balance sheet reports assets, liabilities, and shareholders’ equity at a specific reporting date.

Income statement: An income statement reports revenue, expenses, gains, losses, and profit over a reporting period.

The useful comparison is not which statement is more important. The better starting point is the question being asked: financial position at the reporting date, or performance during the reporting period.

Key Points

- The balance sheet is a date-based snapshot of financial position.

- The income statement is a period-based report of operating performance.

- Balance sheet analysis focuses on assets, liabilities, liquidity, leverage, and equity structure.

- Income statement analysis focuses on revenue, expenses, margins, operating profit, and net income.

- Investors usually need both because profit can look strong while financial risk is building, or financial position can look stable while profitability is weakening.

Balance Sheet vs Income Statement: The Core Difference

The core difference is timing and purpose. A balance sheet is measured at one date, such as the end of a quarter or fiscal year. An income statement covers activity across a period, such as a quarter or full fiscal year.

| Comparison point | Balance sheet | Income statement |

|---|---|---|

| Time covered | One specific date | A reporting period |

| Main question answered | What does the company own, owe, and retain for shareholders? | How much revenue, expense, and profit did the company generate? |

| Main categories | Assets, liabilities, and shareholders’ equity | Revenue, expenses, gains, losses, operating income, and net income |

| Investor use | Checks liquidity, leverage, working capital, capital structure, and financial resilience | Checks sales growth, cost structure, margins, operating performance, and profitability |

| Main limitation | Does not show the full period’s operating performance by itself | Does not show the full financial position or funding risk by itself |

A company can report a strong profit for the period while ending the period with more debt, lower cash, or weaker working capital. The reverse can also happen: a company can have a solid financial cushion while current-period margins are under pressure.

What Goes on Each Statement

Line-item placement is one of the easiest ways to separate the two statements. If the item describes what the company owns, owes, or has accumulated at a date, it usually belongs on the balance sheet. If the item describes revenue earned, costs incurred, or profit generated during a period, it usually belongs on the income statement.

| Item type | Usually appears on | Why it belongs there |

|---|---|---|

| Cash and cash equivalents | Balance sheet | Cash is an asset held at the reporting date. |

| Accounts receivable | Balance sheet | Receivables are amounts owed to the company at the reporting date. |

| Inventory | Balance sheet | Inventory is an asset the company still holds. |

| Debt | Balance sheet | Debt is an obligation outstanding at the reporting date. |

| Shareholders’ equity | Balance sheet | Equity shows the residual claim after liabilities are deducted from assets. |

| Revenue | Income statement | Revenue reflects sales or services recognized during the period. |

| Cost of goods sold | Income statement | It is a period cost tied to revenue generation. |

| Operating expenses | Income statement | These expenses are incurred during the reporting period. |

| Operating income | Income statement | It measures profit from operations during the period. |

| Net income | Income statement | It is the final profit result for the period after expenses and other items. |

Some items connect the statements. Net income flows into retained earnings after dividends and other equity adjustments, so the income statement can change part of the equity section on the balance sheet. That connection is useful, but it does not make the two reports interchangeable.

How Investors Use Each Statement

Balance sheet analysis starts with financial position. Cash, manageable debt, working capital, and the equity base help show whether the company has enough cushion to handle weaker periods. Liquidity pressure, rising leverage, or assets that are not converting into cash can change that reading.

The income statement shifts the focus to period performance. Revenue growth, gross margin, operating margin, expense control, and net income help show whether the business model produced stronger or weaker results during the reporting period.

| Investor question | Start with | What to check |

|---|---|---|

| Can the company meet near-term obligations? | Balance sheet | Cash, current assets, current liabilities, and working capital |

| Is the company taking on more financial risk? | Balance sheet | Debt, liabilities, equity base, and capital structure |

| Is the company growing sales? | Income statement | Revenue growth and revenue mix |

| Is the company converting sales into profit? | Income statement | Gross profit, operating income, margins, and net income |

| Are reported profits supported by financial position? | Both | Receivables, inventory, debt, retained earnings, and cash-flow confirmation |

The statement choice depends on the investor question. Profitability questions usually begin with the income statement. Liquidity, leverage, and capital-structure questions usually begin with the balance sheet. Quality-of-earnings questions often require both.

Same Company, Different Reading

Illustrative scenario: A company reports higher revenue and higher net income for the year. On the income statement, the period looks better because sales increased and profit improved.

At the same time, the balance sheet shows that accounts receivable, inventory, and debt also increased. That does not automatically make the company weak, but it changes the follow-up question. The investor now needs to ask whether growth is converting into cash, whether customers are paying on time, whether inventory is building too quickly, and whether debt is funding too much of the expansion.

The income statement describes the improved period performance. The balance sheet shows what financial position remained after that performance was recorded. Reading only the income statement could miss balance-sheet pressure. Reading only the balance sheet could miss the operating improvement that created the change.

Why Neither Statement Works Alone

Neither statement is universally more useful. A profitable company can still carry balance-sheet risk. A cash-rich company can still face weak revenue growth or margin pressure. The better starting point depends on the question being asked.

Common mistake: Treating one statement as the whole story. The income statement can make a company look attractive when profit is rising, but the balance sheet may show that the growth required more borrowing or tied up more cash in receivables and inventory. The balance sheet can make a company look financially secure, but the income statement may show that operations are becoming less profitable.

Cross-statement reading is especially important with accrual accounting. Revenue and expenses can be recognized before the related cash movement is fully visible. That is why investors often use the cash flow statement as a follow-up check, without turning every balance sheet vs income statement comparison into a full three-statement analysis.

When to Start With the Balance Sheet or Income Statement

Start with the balance sheet when the question is about financial position, solvency, liquidity, leverage, asset quality, or working capital. Start with the income statement when the question is about revenue, costs, margins, operating income, or net income.

| Analytical situation | Better starting point | Why |

|---|---|---|

| A company has rising debt | Balance sheet | Debt and related obligations are balance-sheet items. |

| A company’s profit margin is shrinking | Income statement | Margins come from revenue, costs, and profit during the period. |

| A company is growing quickly but cash feels tight | Both | Growth appears in revenue, while cash strain may appear in receivables, inventory, debt, or working capital. |

| A company has stable assets but weaker earnings | Income statement first, then balance sheet | The income statement shows the operating decline, while the balance sheet helps judge how much cushion remains. |

Choose the statement that answers the immediate question, then use the other statement to check whether the first answer is complete.

FAQ

What is the main difference between a balance sheet and an income statement?

A balance sheet shows financial position at one date. An income statement shows performance over a period. The balance sheet focuses on assets, liabilities, and equity; the income statement focuses on revenue, expenses, and profit.

Does net income appear on the balance sheet?

Net income appears on the income statement. It can affect the balance sheet through retained earnings after dividends and other equity adjustments, but the net income line itself is part of the income statement.

Are salaries on the balance sheet or income statement?

Salaries are usually recorded as expenses on the income statement when they relate to the reporting period. Unpaid salary obligations may also appear as liabilities on the balance sheet until they are paid.

Which statement should investors read first?

It depends on the question. Profitability and margin questions usually start with the income statement. Liquidity, debt, and financial-position questions usually start with the balance sheet. A complete analysis often uses both.