Operating cash flow is the cash a company generates from normal business operations during a reporting period. It appears in the operating activities section of the cash flow statement and helps investors compare accrual profit with cash actually produced by the business.

Operating cash flow is often shortened to OCF. It focuses on cash from core operations, not cash raised from financing activities or cash spent on investments such as acquisitions, securities purchases, or capital assets.

What operating cash flow means

Operating cash flow: cash generated or used by a company’s ordinary business activities before investing and financing cash flows are considered.

For investors, OCF is a cash-conversion measure. It helps show whether reported profit is supported by operating cash movement, but it does not by itself prove that a company is high quality, undervalued, or likely to produce strong future returns.

Key points about operating cash flow

- OCF belongs in the operating activities section, separate from investing and financing cash flows.

- The indirect method starts with net income and adjusts for non-cash items and working-capital changes.

- The direct method summarizes operating cash receipts and operating cash payments.

- OCF can differ sharply from net income because accrual accounting and cash movement do not always occur at the same time.

- A strong OCF number still needs follow-up checks, especially capital expenditures, working capital, debt obligations, and classification quality.

Where operating cash flow appears

Operating cash flow appears in the operating activities section of the cash flow statement. That section captures cash connected to the company’s normal business activity, such as customer collections, supplier payments, employee costs, tax payments, and other operating receipts or payments.

The boundary matters because the same company can show positive operating cash flow while using cash for capital expenditures, acquisitions, debt repayment, or share repurchases elsewhere on the statement. OCF is one section of the cash flow statement, not the full cash movement of the business.

| Cash flow section | Main question it answers | OCF boundary |

|---|---|---|

| Operating activities | Did core operations generate or use cash? | Operating cash flow is reported here. |

| Investing activities | How much cash went into assets, acquisitions, or investments? | Excluded from OCF. |

| Financing activities | How did debt, equity, dividends, or buybacks affect cash? | Excluded from OCF. |

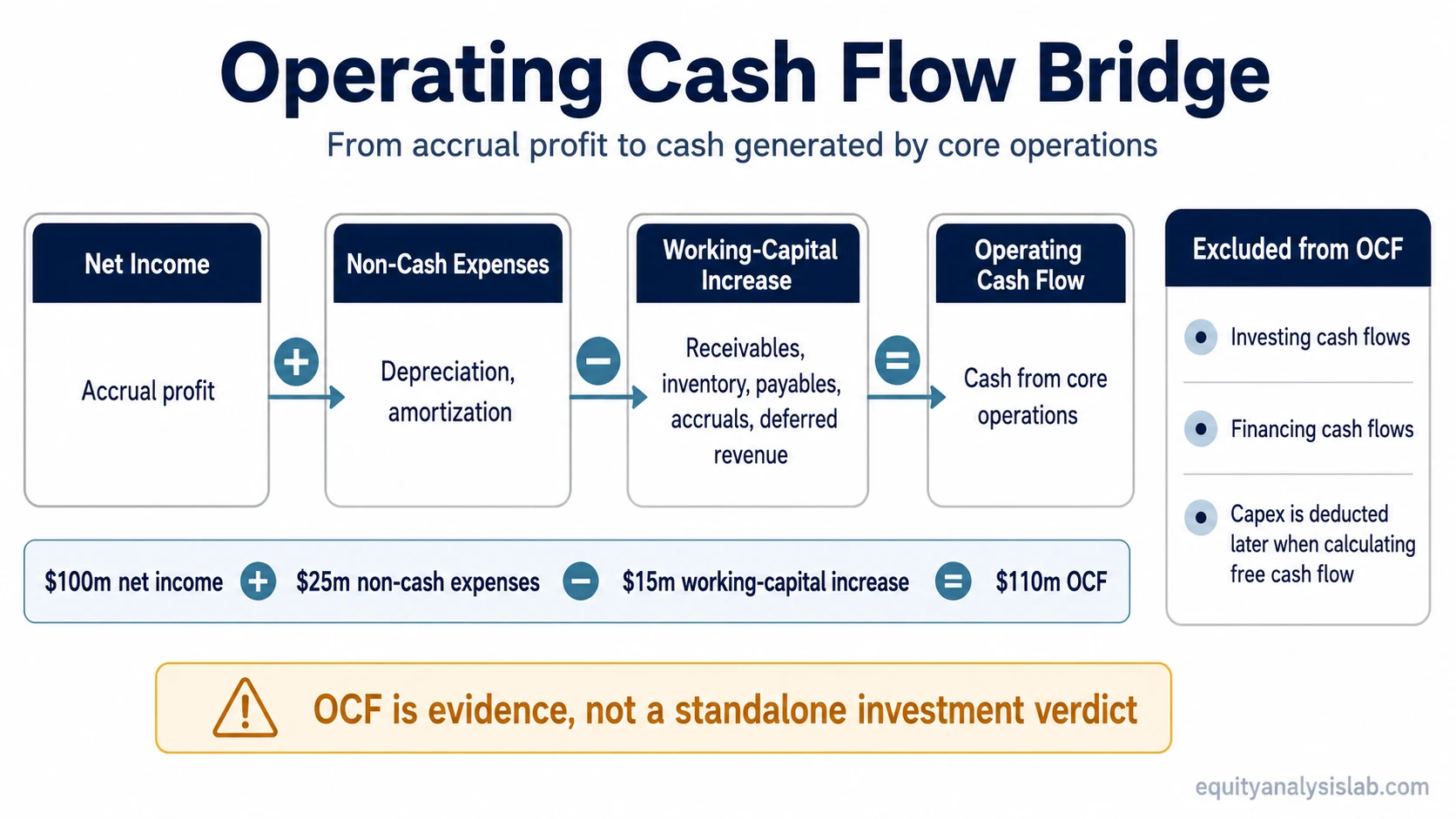

Operating cash flow formula

Under the indirect method, operating cash flow starts with net income and then adjusts for non-cash expenses and changes in operating working capital.

| Formula |

|---|

| Operating Cash Flow = Net Income + Non-Cash Expenses − Increase in Working Capital |

This simplified formula captures the main logic. Actual filings can include additional operating adjustments, but the core idea is to reconcile accounting profit to cash generated or used by operations.

| Component | What it does | Investor check |

|---|---|---|

| Net income | Starts from accrual-based profit. | Check whether profit is recurring or affected by unusual items. |

| Non-cash expenses | Adds back charges such as depreciation and amortization that reduced profit but did not use cash in the period. | Check whether non-cash add-backs are normal for the business model. |

| Working-capital changes | Adjusts for cash tied up in receivables, inventory, payables, accrued expenses, and deferred revenue. | Check whether cash conversion is improving because of operations or because of timing effects. |

Indirect method vs direct method

The indirect method reconciles net income to operating cash flow. It is useful because it connects the income statement to cash movement and shows where accrual profit differs from operating cash.

The direct method starts from actual operating cash inflows and outflows. It usually presents cash received from customers and cash paid for operating costs, then arrives at net cash from operating activities.

Two ways to present operating cash flow

| Method | Starting point | Main use |

|---|---|---|

| Indirect method | Net income | Shows the bridge from accounting profit to operating cash. |

| Direct method | Operating cash receipts and operating cash payments | Shows operating cash movement more directly. |

Why operating cash flow differs from net income

Net income is based on accrual accounting, so revenue and expenses can be recognized before or after cash changes hands. Operating cash flow adjusts that profit number to reflect the cash effect of operations during the period.

A company can report profit while cash collections lag behind revenue recognition. A company can also show weaker profit while OCF looks stronger because depreciation reduced net income without using current-period cash.

The distinction is especially important when receivables, inventory, payables, or deferred revenue move sharply. OCF helps test whether the profit story is supported by cash movement, but it still needs context from the income statement and the balance sheet.

Working-capital effects on operating cash flow

Working capital can make OCF stronger or weaker even when the underlying business has not changed as much as the cash flow number suggests. That is why investors usually compare OCF with balance sheet movements rather than reading one period in isolation.

| Working-capital item | How it can affect OCF | What to check next |

|---|---|---|

| Accounts receivable | Rising receivables can reduce OCF because sales have been recognized before cash is collected. | Compare receivables growth with revenue growth and collection quality. |

| Inventory | Rising inventory can use cash before the company sells the goods. | Check whether inventory is building because demand is strong, timing is seasonal, or sales are slowing. |

| Accounts payable | Rising payables can improve OCF temporarily because the company is paying suppliers later. | Check whether supplier financing is sustainable or only a timing benefit. |

| Accrued expenses | Accruals can lift OCF when expenses are recognized before cash is paid. | Check whether the accrual pattern reverses in later periods. |

| Deferred revenue | Customer payments received before revenue recognition can strengthen OCF. | Check whether deferred revenue reflects durable demand or timing of billings. |

Operating cash flow vs free cash flow

Operating cash flow measures cash from core operations before capital expenditures. Free cash flow goes one step further by subtracting capital expenditures from operating cash flow.

The difference matters for capital-intensive companies. A business can produce healthy OCF but still have limited free cash flow if it must reinvest heavily just to maintain or expand its asset base.

| Metric | What it includes | What it does not prove |

|---|---|---|

| Operating cash flow | Cash from core operations. | It does not show how much cash remains after capital expenditures. |

| Free cash flow | Operating cash flow after capital expenditures. | It does not automatically prove valuation attractiveness or future returns. |

Simple operating cash flow calculation

Assume a company reports $100 million of net income, records $25 million of depreciation, and has a $15 million increase in working capital during the period.

| Step | Amount | OCF effect |

|---|---|---|

| Net income | $100 million | Starting point |

| Add back depreciation | $25 million | Non-cash expense added back |

| Subtract increase in working capital | $15 million | Cash tied up in operations |

| Operating cash flow | $110 million | $100 million + $25 million − $15 million |

The result is higher than net income because the non-cash depreciation add-back is larger than the working-capital cash use. The interpretation would change if working capital kept rising faster than revenue, if receivables were not being collected, or if capital expenditures consumed most of the cash afterward.

How investors can interpret operating cash flow

Operating cash flow is most useful when it is compared across periods and against the rest of the financial statements. A single strong OCF number can reflect better cash conversion, but it can also reflect timing effects such as slower supplier payments or customer prepayments.

| OCF observation | Possible interpretation | Follow-up check |

|---|---|---|

| OCF rises faster than net income | Cash conversion may be improving. | Check receivables, payables, deferred revenue, and unusual working-capital movements. |

| Net income rises but OCF weakens | Profit may not be converting into cash yet. | Check receivables, inventory, revenue quality, and collection timing. |

| OCF is positive but free cash flow is weak | Operations generate cash, but reinvestment needs may be high. | Check capital expenditures and maintenance investment needs. |

| OCF supports debt obligations | Operating cash may provide capacity for interest or principal payments. | Compare cash generation with maturities, interest costs, and cash flow available for debt analysis. |

Common mistake: treating OCF as a standalone verdict

Strong operating cash flow is useful evidence, but it is not proof of business quality. Weak OCF is a warning sign to examine, but it is not automatically proof that the business is failing.

OCF can be affected by working-capital timing, accounting classification, seasonality, customer payment patterns, supplier terms, and non-cash adjustments. It also does not include capital expenditures, so it cannot answer how much cash remains after reinvestment needs.

A stronger read comes from comparing OCF with net income, free cash flow, the balance sheet, debt obligations, and several reporting periods. The useful question is not only whether OCF is positive, but why it changed and whether the change is repeatable.

What to check next

- Cash flow statement: confirm how operating, investing, and financing cash flows are separated.

- Free cash flow: check whether capital expenditures leave cash available after operating cash flow.

- Balance sheet: review receivables, inventory, payables, accrued expenses, and deferred revenue.

- Debt obligations: compare operating cash generation with interest costs, maturities, and refinancing needs.

FAQ

Is operating cash flow the same as profit?

No. Profit is based on accrual accounting, while operating cash flow adjusts for non-cash items and working-capital movements to show cash from operations.

Can operating cash flow be positive when net income is negative?

Yes. Non-cash expenses, working-capital movements, and other operating adjustments can make OCF positive even when net income is negative.

Why can operating cash flow fall when sales rise?

Sales can rise before cash is collected. If receivables or inventory grow quickly, more cash may be tied up in operations, reducing OCF for the period.

Does high operating cash flow mean a stock is attractive?

No. OCF is one financial-statement input. Valuation, reinvestment needs, debt, earnings quality, competitive position, and future business risk still need separate analysis.