A hedged ETF tries to reduce the effect of currency moves on an investor’s return, while an unhedged ETF leaves those currency moves in the return path. The underlying market exposure can be similar, but the investor’s final result can differ because the currency treatment is different.

The practical comparison is not “which wrapper is better.” It is whether the investor wants the foreign asset return to stand more on its own, or whether foreign currency movement is an intended part of the allocation.

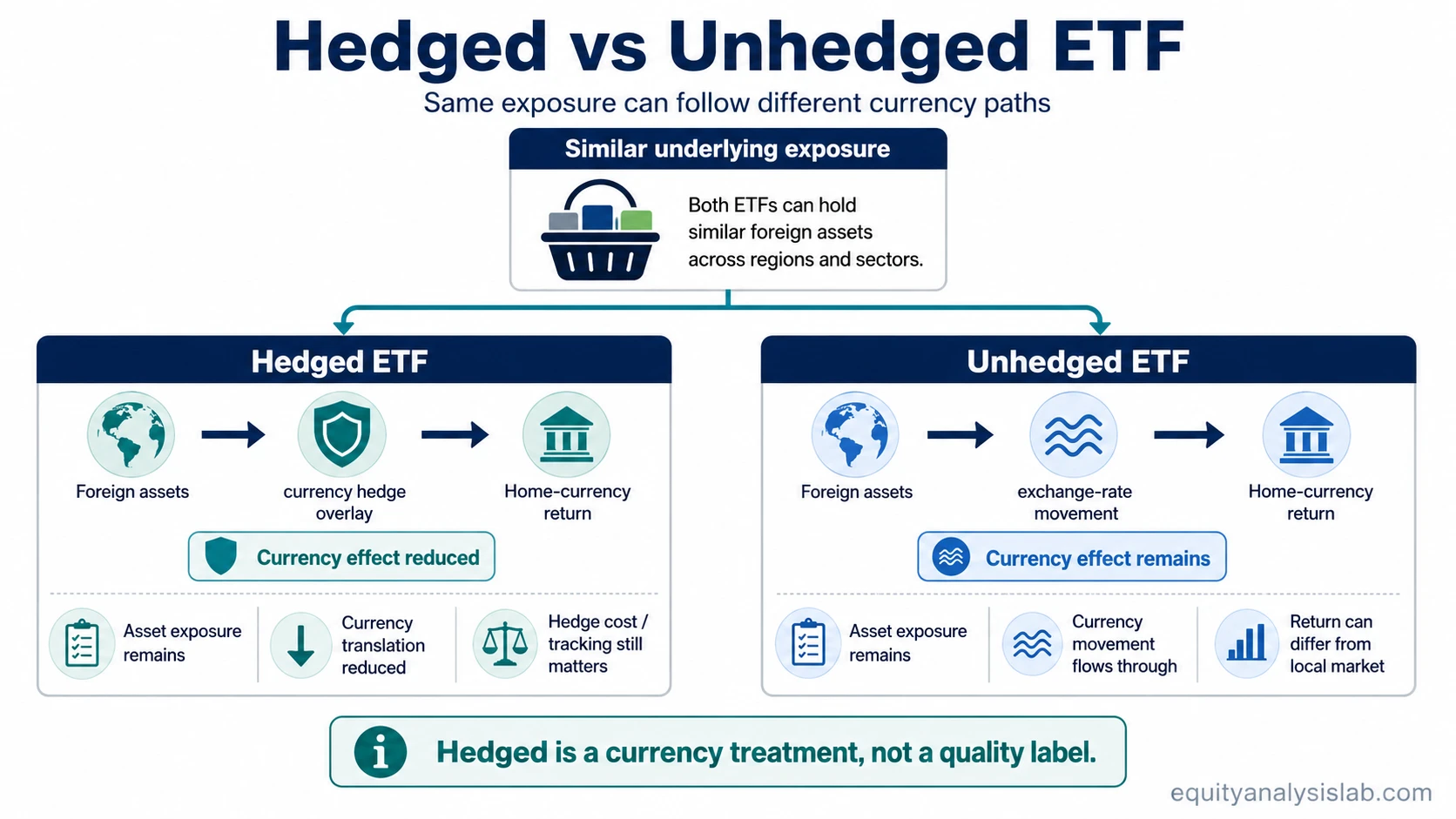

Hedged vs Unhedged ETF: Core Difference

- A hedged ETF uses a currency hedge overlay to reduce the effect of exchange-rate movement between the investor’s home currency and the foreign exposure.

- An unhedged ETF leaves that currency movement open, so the investor’s return reflects both the asset return and the currency translation effect.

- The same broad market exposure can produce different investor-level results if one version is hedged and another is unhedged.

- Hedging is an exposure choice, not a fund-quality label. Costs, tracking, liquidity, tax treatment, and portfolio role still need to be checked.

What a Hedged ETF Changes

A hedged ETF adds a currency overlay to the portfolio. In simple terms, the fund or share class tries to offset part of the movement between the investor’s reference currency and the currency exposure of the assets it holds.

That hedge is usually implemented with currency instruments such as forwards or similar derivatives. The investor does not normally manage those contracts directly; the hedge is part of the fund’s structure or share-class design.

The intended result is less exposure to currency translation. If a foreign equity market rises but the foreign currency weakens against the investor’s home currency, the hedge may reduce the currency drag. If the foreign currency strengthens, the hedge may also reduce the benefit that an unhedged investor would have received.

Hedging is not free from trade-offs. The hedge can add operating cost, create tracking difference, and work imperfectly when markets are volatile, liquidity is thin, or the hedge does not match the exposure exactly.

What an Unhedged ETF Leaves Exposed

An unhedged ETF leaves the currency translation effect in place. A home-currency investor who buys foreign assets is not only exposed to the securities inside the fund; the investor is also exposed to how the foreign currency moves against the investor’s reference currency.

This can help or hurt. If the underlying market rises and the foreign currency strengthens, the currency movement can add to the home-currency return. If the underlying market rises but the foreign currency weakens, part of the market gain can be reduced or even offset after translation.

The unhedged version avoids the specific hedge overlay, but it does not remove risk. It simply keeps currency movement as one of the drivers. For some investors, that exposure is acceptable or even desired. For others, it can make the fund behave differently from the asset exposure they thought they were buying.

Hedged vs Unhedged ETF Comparison Criteria

| Criterion | Hedged ETF | Unhedged ETF | Investor interpretation |

|---|---|---|---|

| Currency exposure | Attempts to reduce currency translation exposure. | Leaves currency movement in the return path. | Start by identifying whether the currency effect is intended or unwanted. |

| Return drivers | Designed to make the asset return more dominant, though not perfectly isolated. | Combines asset return and currency translation effect. | Two funds with similar holdings can still deliver different home-currency results. |

| Cost effect | May have additional hedge-related cost or drag. | Does not carry the same hedge overlay, though normal fund costs still apply. | Compare the stated expense ratio and any available tracking data rather than assuming the cheaper-looking version is better. |

| Tracking behavior | May differ from the unhedged index or from the asset market because the hedge changes the return calculation. | May track the unhedged reference more directly, depending on the fund and index design. | Review tracking error and tracking difference when available. |

| Volatility pattern | Can reduce currency-driven volatility, but it does not remove market volatility from the assets. | Can have more home-currency variability when exchange rates move sharply. | The smoother-looking version depends on both the asset class and the currency environment. |

| Liquidity and spreads | The hedged share class or fund version may have different trading volume and spreads. | The unhedged version may be more liquid, less liquid, or similar depending on the market. | Check fund-level trading conditions and ETF liquidity, not only the label. |

| Portfolio role | Often used when the investor wants foreign asset exposure with less currency translation impact. | Often used when the investor accepts foreign currency exposure as part of diversification or return variability. | Match the fund version to the role the allocation is meant to play. |

| Time horizon | May appeal when currency movement is not part of the intended long-term exposure. | May appeal when the investor wants the currency exposure or accepts it across the holding period. | The right comparison depends on the portfolio objective, not only on recent currency moves. |

Same Portfolio Example

Suppose two ETFs hold similar foreign equities. One version is hedged to the investor’s home currency and the other is unhedged. If the foreign equity market rises by the same amount in local terms, the investor can still see different home-currency results because one version tries to reduce currency translation while the other leaves it open.

The same logic works in the other direction. If the underlying foreign market falls, currency movement can either soften or worsen the home-currency result for the unhedged version. The hedged version may reduce that currency effect, but it still remains exposed to the assets and to the costs and imperfections of the hedge.

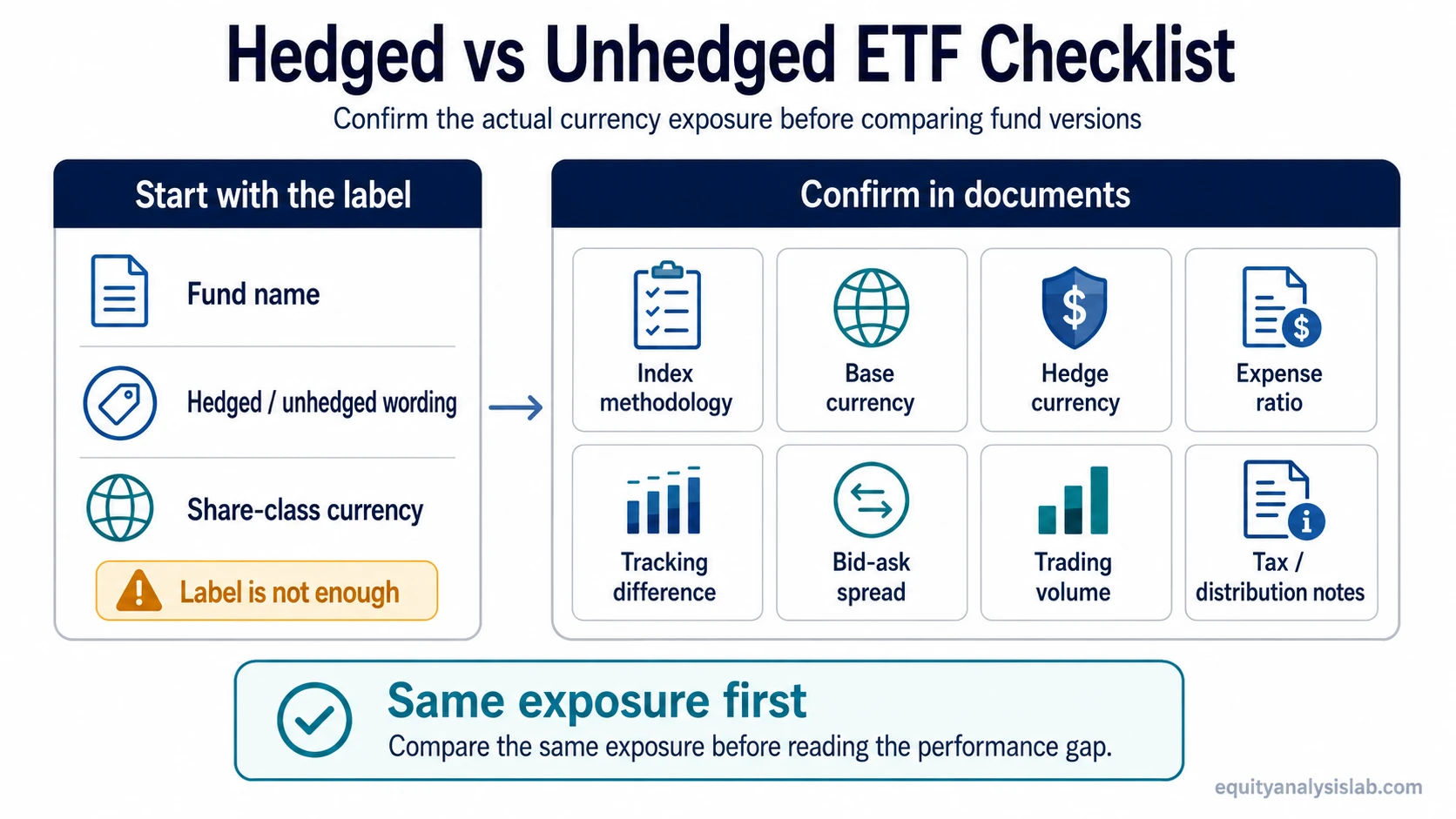

How to Check Which Exposure a Fund Gives You

The fund name is only a starting point. A fund can use words such as “hedged,” “currency hedged,” or a share-class currency label, but the actual exposure depends on the prospectus, index methodology, share-class details, and portfolio implementation.

| Check | Why it matters |

|---|---|

| Fund or share-class label | Identifies whether the product is marketed as hedged, unhedged, or currency-specific. |

| Index methodology | Shows whether the benchmark itself is hedged or unhedged. |

| Fund base currency | Shows the accounting or reporting currency, but it does not always equal the economic currency exposure. |

| Hedge currency | Shows which currency relationship the fund is trying to hedge. |

| Expense ratio and hedge costs | Helps identify whether the hedge changes the cost profile. |

| Tracking difference | Shows how the fund actually behaved against its reference exposure after fees and implementation effects. |

| Bid-ask spread and trading volume | Shows whether the version you choose is practical to trade at the expected size. |

| Tax and distribution notes | May affect after-tax results depending on jurisdiction and investor type. |

Common Confusion: Hedged Does Not Mean Higher Quality

A hedged ETF is not automatically better than an unhedged ETF. It is a different currency treatment. The hedge may reduce one source of return variability, but it can also reduce currency gains, add cost, and create tracking differences.

The same caution applies to unhedged funds. An unhedged ETF is not automatically more authentic, cheaper in all cases, or more diversified in a useful way. It simply leaves currency movement in the investor’s return path.

Limits of Currency Hedging

- Hedging may reduce currency translation effects, but it does not remove the market risk of the securities inside the ETF.

- The hedge may not perfectly match the portfolio exposure, especially if the holdings, weights, or underlying currencies shift.

- Hedge costs can change over time as interest-rate differentials and currency-market conditions change.

- Tracking difference can appear because the fund must implement the hedge in real markets rather than in a frictionless model.

- Tax treatment, distributions, and fund domicile can affect the investor’s after-tax result and should be checked separately.

When a Hedged ETF May Fit the Exposure Question

A hedged ETF may fit when the investor wants exposure to the foreign asset class but does not want currency movement to dominate the home-currency result. This can be especially relevant when the allocation is meant to express a view on the asset market rather than on the currency pair.

That does not make the hedged version a default choice. The investor still needs to compare costs, tracking behavior, liquidity, and the specific hedge design. A hedge that looks attractive in theory can be less useful if the share class is thinly traded, expensive, or poorly aligned with the actual exposure.

When an Unhedged ETF May Fit the Exposure Question

An unhedged ETF may fit when the investor accepts foreign currency movement as part of the allocation. The currency exposure may be part of the diversification logic, or the investor may prefer a simpler structure without a hedge overlay.

The trade-off is that home-currency returns can differ from the local-market return. A strong foreign equity market can look weaker to the investor if the foreign currency falls, while a weaker local-market result can be softened if the currency moves favorably.

Bond ETF and Equity ETF Nuance

Currency hedging can matter differently across asset classes. In a foreign equity ETF, equity-market movement may be large enough that currency is one important driver among several. In a foreign bond ETF, currency movement can sometimes dominate the home-currency return because the bond return itself may be lower or more rate-sensitive.

This does not mean bond ETFs should always be hedged or equity ETFs should always be unhedged. It means the investor should compare the currency exposure against the asset’s expected role, volatility pattern, income profile, and portfolio purpose.

Hedged vs Unhedged ETF Decision Matrix

| Investor question | Hedged version may be more relevant when… | Unhedged version may be more relevant when… |

|---|---|---|

| Do I want currency movement in the return? | The investor mainly wants asset exposure and wants less currency translation impact. | The investor accepts currency exposure as part of the allocation. |

| Is the fund used for stability or diversification? | The fund is meant to reduce one source of home-currency variability. | The fund is meant to include foreign-currency diversification or natural FX exposure. |

| Are hedge costs meaningful? | The investor accepts the cost and tracking trade-off for reduced currency effect. | The investor prefers to avoid hedge overlay costs and accepts currency variability. |

| Is the share class liquid enough? | The hedged version has acceptable spreads, volume, and fund depth. | The unhedged version has better trading conditions or a cleaner implementation profile. |

| Does the label match the documents? | The documents clearly confirm the hedge currency, method, benchmark, and share-class design. | The documents clearly show currency exposure is intentionally left open. |

Hedged vs Unhedged ETF FAQ

Is a hedged ETF better than an unhedged ETF?

No. A hedged ETF is not automatically better. It changes the currency exposure. The better fit depends on whether the investor wants to reduce currency translation effects, accepts the hedge cost and tracking behavior, and understands the fund’s role in the portfolio.

Can a hedged ETF still lose money?

Yes. Currency hedging does not remove the risk of the securities inside the fund. A hedged ETF can still lose value if the underlying market falls, if rates or credit conditions move against the holdings, or if fund-specific costs and tracking effects matter.

Does unhedged mean the fund is riskier?

Unhedged means currency movement remains in the return path. That can increase home-currency variability, but risk also depends on the underlying assets, fund structure, liquidity, costs, and the investor’s portfolio context.

Is fund base currency the same as currency exposure?

Not necessarily. Fund base currency is an accounting or reporting currency. Currency exposure depends on the assets, index methodology, share class, and any hedge overlay. The fund documents should clarify the actual exposure.

Related ETF Concepts

An ETF can hold similar underlying exposure while using a different currency treatment, so the wrapper label alone is not enough to understand the investor’s actual return drivers.

Currency hedging also connects to tracking, liquidity, and international fund design. Tracking behavior shows whether the fund is following its reference exposure closely, liquidity affects implementation, and international exposure explains why currency translation enters the return path in the first place.