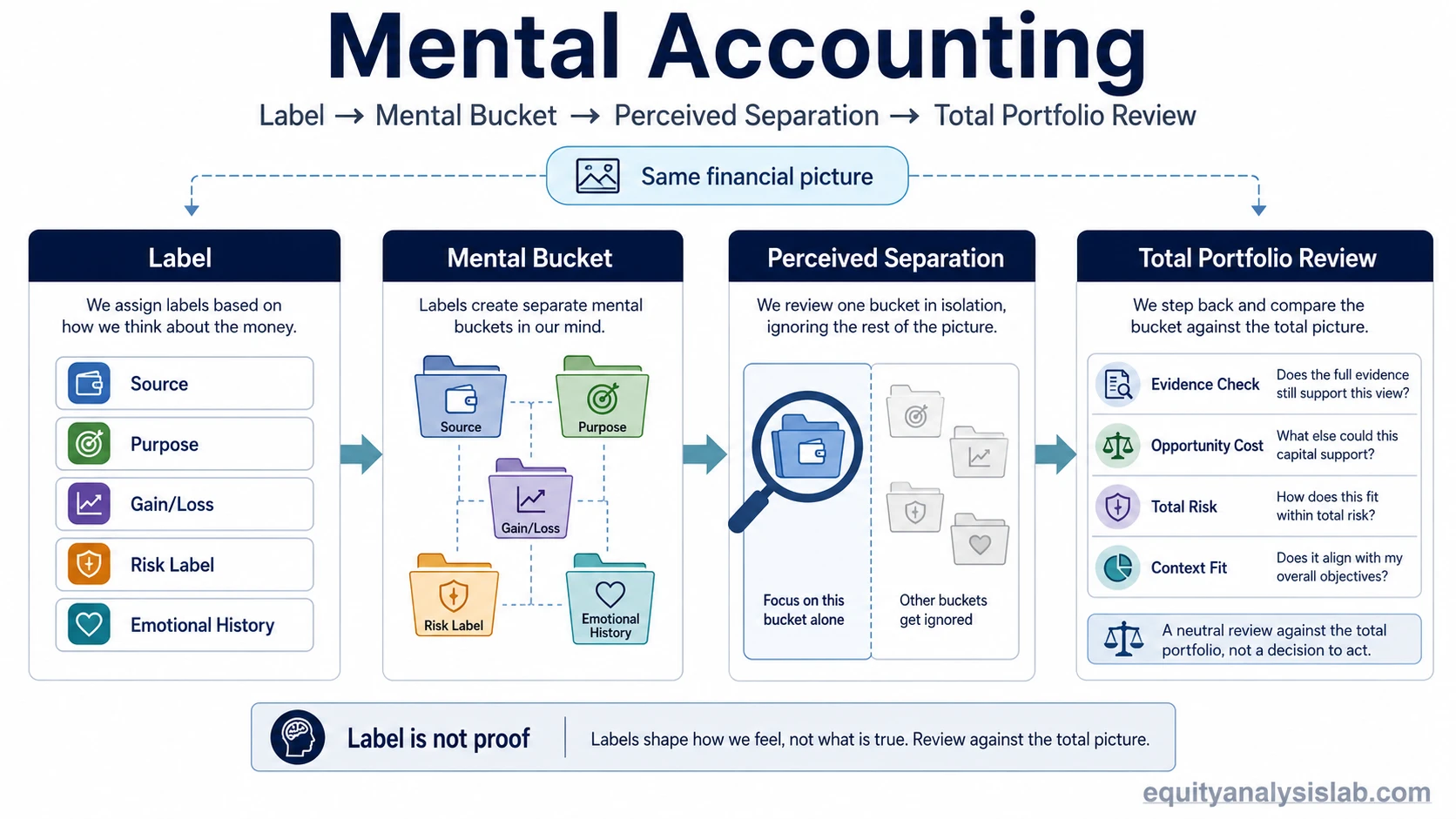

Mental accounting is a behavioral finance bias where money, gains, losses, or investments are separated into mental buckets even though they belong to the same total financial picture.

The core problem is fungibility. Cash, portfolio value, and investment capital can usually be compared across the same overall decision framework, but mental accounting makes one dollar feel different from another because of its source, label, purpose, or emotional history. In investor review, that can cause a position, gain, loss, or cash balance to be judged inside a narrow bucket instead of against total portfolio evidence.

Within behavioral finance, mental accounting is useful because it explains how a clean spreadsheet category can hide a weaker decision process. A label such as “safe money,” “house money,” “long-term holding,” or “speculative bucket” may be convenient for organization, but it can distort judgment when the label starts overriding evidence.

Key Points

- Mental accounting separates money or investments into subjective mental buckets.

- The bias matters because money and portfolio risk are often more connected than the labels make them appear.

- Investor review should compare each bucket against total portfolio evidence, not only against the story attached to the bucket.

- A review checklist helps slow the error before a label turns into an automatic decision.

What Mental Accounting Means

Definition: Mental accounting is the tendency to treat equivalent money or investment value differently because it has been assigned to a separate mental category.

A mental account can be based on source, purpose, timing, gain or loss history, emotional attachment, or an earlier decision label. A bonus may feel different from salary. A realized gain may feel different from original capital. A losing position may feel different from unused cash. A speculative holding may feel separate from a retirement account even when both affect the investor’s total risk exposure.

The concept does not mean that categories are always bad. Separate accounts, budgets, watchlists, and portfolio sleeves can improve organization. The bias appears when the category becomes the decision rule. The question is not whether the label is convenient. The question is whether the label blocks a full review of evidence, risk, opportunity cost, and portfolio fit.

Mental Accounting Categories and Review Questions

Mental accounting is easier to identify when the label, the perceived difference, and the actual portfolio question are separated.

| Review area | How mental accounting appears | Portfolio-level question |

|---|---|---|

| Source of money | A windfall, bonus, dividend, or prior gain is treated as less serious than earned capital. | Does this capital carry the same opportunity cost and risk exposure as the rest of the portfolio? |

| Purpose label | A holding is protected because it sits in a “long-term” or “income” bucket. | Does the current evidence still support the role assigned to that holding? |

| Gain or loss status | A position is reviewed differently because it is currently above or below the purchase price. | Would the same position be justified if it were evaluated from today’s information only? |

| Risk bucket | A speculative bucket feels isolated from the rest of the portfolio. | How does the bucket affect total concentration, downside exposure, and liquidity needs? |

| Emotional history | A past success or mistake changes how current evidence is weighted. | Is the decision being made from current evidence or from the emotional memory of the prior outcome? |

How Mental Accounting Affects Investor Decisions

Mental accounting affects investor decisions by narrowing the review frame. Instead of asking whether a holding still fits the total portfolio, the investor may ask whether it still fits the mental bucket. That smaller question can feel more comfortable, but it may leave out risk overlap, valuation change, business quality, liquidity needs, and opportunity cost.

A common distortion occurs when gains are treated as “house money.” The gain may feel separate from original capital, so the investor may accept a weaker evidence standard for the next decision. The portfolio does not separate the gain in the same emotional way. If the capital is exposed to market risk, it still belongs to the total decision set.

Another distortion appears when a losing position is placed in a “already lost money” bucket. The original purchase price can become the emotional reference point, while the current business evidence, valuation, balance-sheet risk, and portfolio concentration receive less attention. The issue is not whether the position should be kept or sold. The issue is whether the review is being controlled by the bucket rather than by current evidence.

Common mistake: Treating a mental bucket as objective evidence. A label can organize a portfolio, but it does not prove that the investment still fits the investor’s thesis, risk tolerance, time horizon, or research standard.

Where Mental Accounting Shows Up in Portfolio Review

Mental accounting often appears during review moments, not only during the original investment decision. The bias can be quiet because the category sounds rational. “This is my speculative sleeve” or “this is a long-term holding” may be a valid organizational statement, but it becomes weaker when it prevents the same evidence review used elsewhere in the portfolio.

Illustrative scenario: An investor holds three positions with similar business risk, but one position is labeled as a small speculative bucket because it was funded from a prior gain. During review, the investor gives that position more room to deteriorate because it feels separate from core capital. A portfolio-level review would ask whether the exposure, thesis quality, valuation, and downside risk still make sense compared with the full portfolio, not whether the money originally came from a prior gain.

The same pattern can appear with cash. A cash reserve for taxes, living needs, or known obligations may have a real purpose and should not be treated casually. A separate “cash waiting for an idea” bucket is different. That label can still hide opportunity cost if the cash remains unused because the investor is waiting for a perfect opportunity, or it can hide risk if the cash is moved into a position simply because the bucket was meant to be invested.

The useful test is whether the category clarifies the decision or excuses a weaker review. A category clarifies when it makes constraints visible. It distorts when it makes evidence optional.

Mental Accounting Review Checklist

A checklist helps convert mental accounting from a vague bias label into a practical review guardrail. The goal is not to remove every category. The goal is to prevent the category from becoming the decision.

| Checklist question | What it tests | Warning sign |

|---|---|---|

| Would the same decision look reasonable if the source of the money were removed? | Source-label distortion | The decision depends heavily on whether the money came from salary, a gain, a dividend, or a windfall. |

| Would the position still qualify if reviewed as a new investment today? | Purchase-price attachment | The main reason for holding is the original cost, not current evidence. |

| Does the bucket change total portfolio risk? | Portfolio-level exposure | The position is called small or separate, but it overlaps with other risks already held. |

| Is the label describing a constraint or defending an exception? | Category discipline | The label is used to avoid the standard review process. |

| Is the decision being compared with alternatives? | Opportunity cost | The bucket is reviewed in isolation instead of against other uses of capital. |

The checklist does not determine the correct portfolio action. It only checks whether the review process is being narrowed by a mental category.

Mental Accounting vs Nearby Behavioral Biases

Mental accounting is closely related to other investor psychology errors, but the mechanism is specific. It is about separating money, gains, losses, or investments into subjective accounts and then allowing those accounts to change the review standard.

Mental accounting vs anchoring: Mental accounting separates the investment into a bucket. Anchoring bias attaches judgment to a reference point, such as an original purchase price, prior high, target value, or previous estimate.

Mental accounting vs availability bias: Mental accounting changes the category used for review. An availability bias pattern changes the evidence that feels most important because recent, vivid, or memorable information is easier to recall.

Mental accounting vs loss aversion: Mental accounting can separate losses into a special emotional bucket, while loss aversion focuses on the stronger discomfort of losses compared with gains. The two can appear together, but they are not the same mechanism.

Limits of Mental Accounting as an Investor Bias

Mental accounting should not be used as a shortcut for judging every separate account, portfolio sleeve, or investment category as flawed. Real constraints matter. Taxes, time horizon, liquidity needs, account rules, and risk limits can justify separate treatment when the distinction is grounded in an actual constraint.

Limit: The presence of buckets does not prove poor decision-making. The risk appears when the bucket changes the evidence standard, hides total portfolio exposure, or protects a decision from normal review.

The concept also does not prove that any investment should be bought, sold, resized, or avoided. A position can sit inside a mental bucket and still be supported by current evidence. Another position can be reviewed without obvious mental accounting and still be weak for other reasons. Mental accounting is a review lens, not a portfolio instruction.

The strongest use of the concept is procedural. It asks whether the investor is comparing evidence consistently across the portfolio. If the answer is no, the label should be challenged before the decision is treated as clean.

FAQ

What is mental accounting in investing?

Mental accounting in investing is the tendency to treat money, gains, losses, or holdings differently because they sit in separate mental categories. The risk is that the category may override total portfolio evidence.

Is mental accounting always bad?

No. Categories can help organize money and portfolio decisions. Mental accounting becomes a bias when the category changes the evidence standard or hides the connection between one bucket and the full portfolio.

How can investors check for mental accounting?

A useful check is to remove the label and review the decision again. If the conclusion depends mainly on the source of the money, the original purchase price, or the emotional bucket, the review may be distorted.