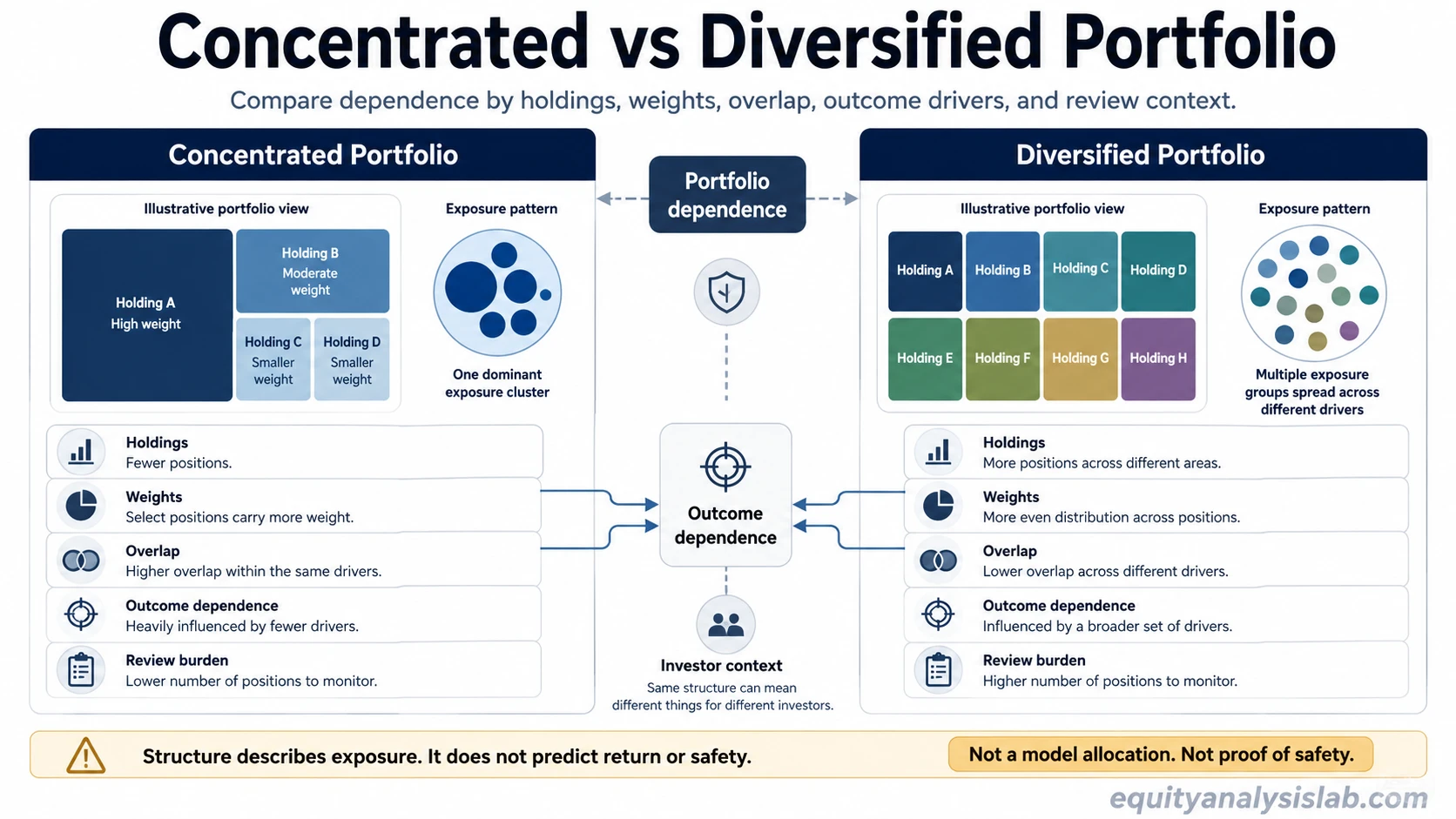

A concentrated portfolio depends more on a smaller number of positions, sectors, themes, or risk drivers. A diversified portfolio spreads dependence across more holdings, sectors, asset classes, or exposures. The difference is not only the number of holdings. Weights, overlap, and review discipline can change how concentrated or diversified a portfolio really is.

Direct answer: Concentration asks how much one exposure can affect the portfolio. Diversification asks how broadly portfolio dependence is spread across different exposures.

Both concepts describe the distribution of portfolio exposure. A portfolio with ten holdings can still be concentrated if one position dominates the weight, if several holdings depend on the same sector, or if the same economic risk driver affects most of the portfolio at the same time.

A portfolio with fewer holdings is not automatically careless, and a portfolio with more holdings is not automatically well diversified. The practical distinction depends on position sizing, exposure overlap, the independence of risk drivers, and whether the portfolio can still be reviewed with discipline.

Key Points

- A concentrated portfolio is driven more by fewer holdings, sectors, themes, issuers, or risk drivers.

- A diversified portfolio spreads dependence across more exposures, but only if those exposures are meaningfully different.

- Holding count alone can mislead because weights and overlap may create hidden concentration.

- Concentration can increase the impact of correct or incorrect security selection, while diversification can reduce dependence on any single outcome.

- Neither structure is universally better; interpretation depends on objectives, time horizon, risk capacity, review discipline, and portfolio role.

What Separates Concentrated and Diversified Portfolios?

The cleanest distinction is outcome dependence. A concentrated portfolio relies more heavily on a smaller set of outcomes. A diversified portfolio reduces reliance on any one outcome by spreading exposure across multiple holdings, sectors, asset classes, or risk drivers.

Portfolio concentration is not only a count of positions. It can come from one large holding, several holdings in the same industry, exposure to one factor such as interest-rate sensitivity, or a portfolio where the same thesis drives many positions at once.

Portfolio diversification is more meaningful when different holdings do not all depend on the same event, sector, earnings driver, liquidity condition, or valuation assumption. Adding more names helps less when those names behave like variations of the same exposure.

Key Differences by Holdings, Weights, and Dependence

| Comparison point | Concentrated portfolio | Diversified portfolio |

|---|---|---|

| Core question | How much can a smaller set of exposures drive results? | How broadly is dependence spread across different exposures? |

| Holdings count | Usually fewer holdings, though the number alone is not enough. | Usually more holdings, but more names do not guarantee true diversification. |

| Weight distribution | One or several positions may carry a large share of total portfolio weight. | Weights are spread more evenly or intentionally across different exposures. |

| Outcome dependence | Results may depend heavily on a few company, sector, theme, or factor outcomes. | Results depend less on any single company, sector, theme, or factor outcome. |

| Overlap risk | Overlap can be obvious when top holdings dominate. | Overlap can be hidden if many holdings share the same risk driver. |

| Volatility and drawdown exposure | Single-position or single-theme setbacks can have a larger portfolio effect. | Losses in one area may be partly offset by exposure elsewhere, but losses can still occur. |

| Monitoring burden | Fewer positions may be easier to review deeply, but each decision matters more. | More positions can reduce single-name dependence, but the review burden can rise. |

| Rebalancing drift | Winners or laggards can quickly change the portfolio’s exposure profile. | Diversification can weaken if drift turns one exposure into a dominant weight. |

| Investor context | Requires capacity to tolerate larger swings from fewer exposures. | Requires enough structure to avoid spreading capital into holdings that cannot be followed. |

Same Holdings, Different Exposure: A Simple Example

Example scenario: Two portfolios can own the same ten stocks and still have different concentration profiles. Portfolio A puts half of its value into two holdings and spreads the rest across the other eight. Portfolio B spreads the ten holdings more evenly. The holdings count is identical, but Portfolio A depends more on the two largest positions.

The same logic applies to sector and theme overlap. A portfolio may hold many companies, but if most of them depend on the same industry cycle, commodity price, interest-rate sensitivity, or valuation factor, the portfolio can remain concentrated beneath the surface.

This is where asset allocation can change the interpretation. A portfolio may look diversified by stock count while still being narrow by asset class, sector exposure, currency exposure, or economic sensitivity.

The useful test is not “how many line items are on the statement?” The useful test is “what could go wrong, and how much of the portfolio depends on that same thing not going wrong?”

Common Confusion Traps

| Confusion trap | Why it misleads | Cleaner interpretation |

|---|---|---|

| “More holdings means diversified.” | Many holdings can still share the same sector, factor, or economic driver. | Check whether the exposures are meaningfully different. |

| “Fewer holdings means reckless.” | A smaller portfolio can be intentional if the investor understands the exposures and can tolerate the dependency. | Assess position size, thesis quality, and risk capacity rather than count alone. |

| “Conviction reduces risk.” | High conviction can increase concentration if it leads to oversized exposure. | Separate confidence in a thesis from the portfolio impact if the thesis is wrong. |

| “Diversification removes risk.” | Diversification can reduce single-outcome dependence, but it cannot remove market, liquidity, valuation, or behavioral risk. | Treat diversification as risk distribution, not risk elimination. |

| “Rebalancing is only maintenance.” | Portfolio drift can quietly turn a diversified portfolio into a more concentrated one. | Review whether current weights still match the intended exposure profile. |

When the Distinction Changes in Practice

The same portfolio can become more concentrated over time even if no new holdings are added. A few positions may grow faster than the rest, or several unrelated-looking holdings may become tied to the same earnings, rates, credit, or liquidity condition.

Time horizon also changes interpretation. A long time horizon may make an investor more willing to tolerate temporary volatility, but it does not make concentration harmless. A short time horizon can make even moderate concentration harder to manage if the portfolio must absorb withdrawals or near-term cash needs.

Risk capacity matters because concentration changes the size of possible portfolio damage from a small number of decisions. Risk tolerance describes comfort with volatility, but risk capacity describes whether the investor can financially absorb the consequences if the concentrated exposure performs poorly.

Review discipline matters because diversification has a management cost. A portfolio with many small holdings may reduce single-name exposure, but it can also become difficult to monitor if the investor cannot review business quality, valuation, thesis deterioration, position overlap, and rebalancing drift with enough attention.

What the Difference Does and Does Not Tell You

A concentrated portfolio is not automatically better because it is focused. A diversified portfolio is not automatically better because it is broader. The correct interpretation depends on what the portfolio is supposed to do and how much dependence the investor can knowingly accept.

Limitation: The concentrated-versus-diversified distinction does not predict returns, identify a safer portfolio, or recommend a model allocation. It only describes how portfolio dependence is distributed.

The practical question is whether the exposure profile matches the investor’s objectives, review capacity, time horizon, and risk capacity. A portfolio can be too concentrated for one investor and too diluted for another, even if both portfolios contain the same number of holdings.

Quick Decision Frame

| Question to ask | What it reveals |

|---|---|

| What are the largest holdings by weight? | Whether a few positions dominate portfolio outcomes. |

| Do multiple holdings depend on the same sector or theme? | Whether diversification is weaker than the holdings count suggests. |

| What risk driver would hurt several positions at once? | Whether hidden concentration exists across apparently different holdings. |

| Has portfolio drift changed the original exposure mix? | Whether rebalancing review is needed to keep the intended structure visible. |

| Can each holding still be reviewed with discipline? | Whether diversification has become too broad to monitor properly. |

FAQ

Is a concentrated portfolio the same as a risky portfolio?

No. Concentration describes dependence on fewer exposures. Risk depends on position size, business quality, valuation, liquidity, time horizon, risk capacity, and how the exposures interact.

Can a diversified portfolio still be concentrated?

Yes. A portfolio can hold many positions and still be concentrated if the holdings share the same sector, theme, asset class, factor, or economic sensitivity.

Is diversification always better than concentration?

No. Diversification can reduce dependence on any single outcome, but it can also create a portfolio that is too broad to review well. Concentration can be intentional, but it increases the impact of fewer decisions.

What is the biggest difference between concentration and diversification?

The biggest difference is outcome dependence. Concentration means fewer exposures can drive more of the result. Diversification means dependence is spread across more meaningfully different exposures.