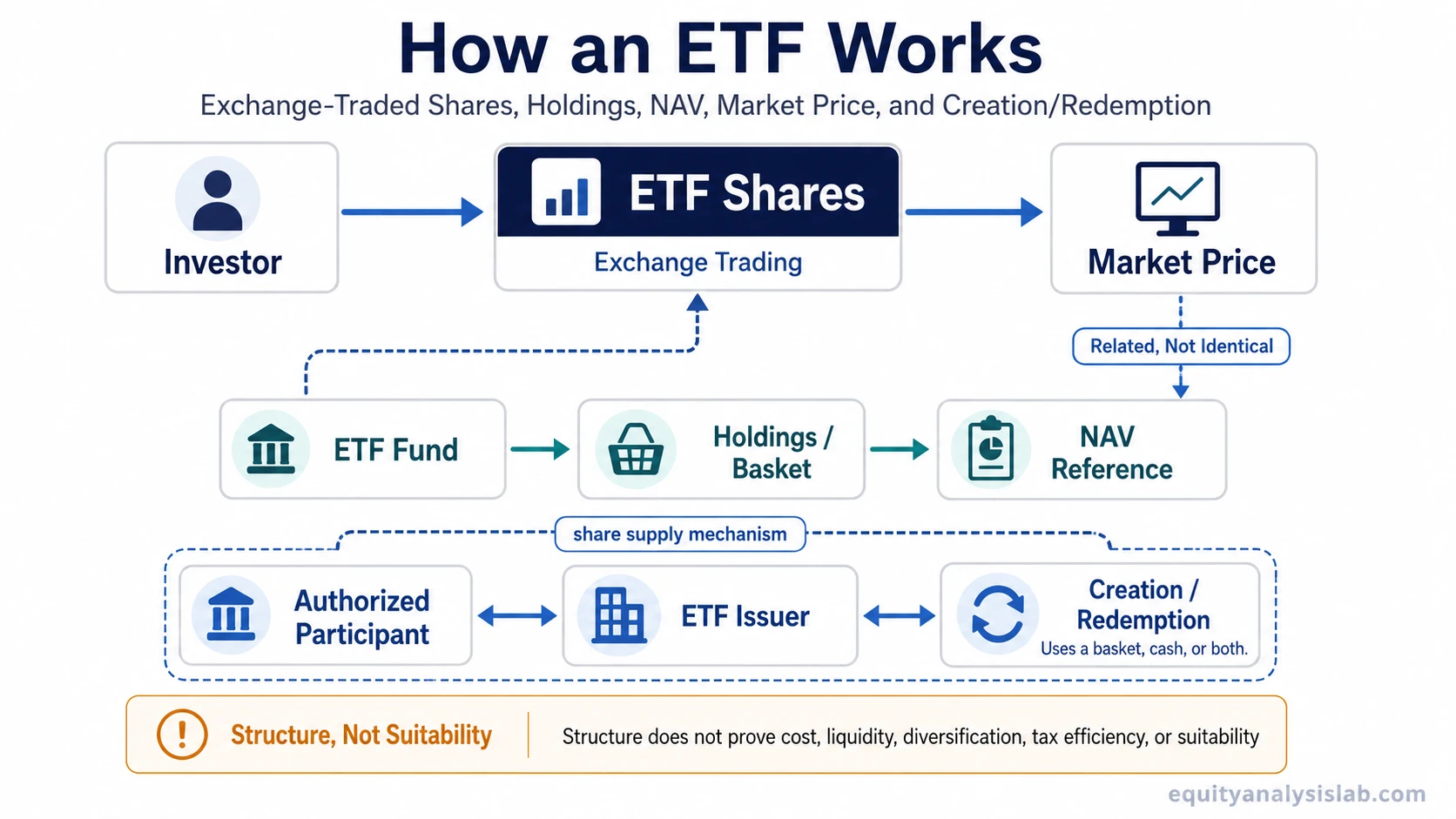

An ETF works by issuing shares that trade on an exchange while the fund holds a basket of securities or other assets. The ETF share price moves through market trading, while the fund’s holdings create the exposure and NAV reference behind the structure. Creation and redemption activity can help keep ETF share supply connected to the underlying basket, but the ETF label by itself does not prove low cost, liquidity, diversification, tax efficiency, return quality, or suitability.

Core limitation: ETF mechanics explain how the wrapper is traded and organized. They do not tell an investor whether the holdings, strategy, cost structure, liquidity profile, tracking behavior, distribution policy, or tax treatment fit a specific objective.

How ETF Shares and Holdings Work Together

An ETF has two connected layers. The first layer is the share that investors buy or sell on an exchange. The second layer is the fund portfolio behind that share, which may hold stocks, bonds, commodities exposure, derivatives, cash instruments, or another defined basket depending on the fund’s mandate.

This distinction matters because the investor does not directly buy every security inside the portfolio when placing an ETF order. The investor buys or sells ETF shares in the secondary market, while the fund structure holds the assets that create the economic exposure. That distinction separates the trading mechanism from the broader fund wrapper concept, where the question is what an ETF is as a category rather than how its shares and holdings interact.

The mechanism is therefore not just “a ticker trades.” The ticker is the tradable share. The holdings, index, active strategy, basket rules, cost structure, and creation/redemption process explain what sits behind that share.

How ETF Shares Trade on an Exchange

ETF shares trade during the market day through exchange quotes. Buyers and sellers transact at market prices that can move as demand, supply, underlying asset values, and market liquidity change. This makes the ETF share look similar to a stock at the point of execution, even though the structure behind it is a pooled fund.

The quoted price is not the only cost signal. Investors also need to check the bid-ask spread, because the difference between the buying quote and selling quote can become part of the practical trading cost. A narrower spread can reduce visible trading friction, while a wider spread can increase the practical cost of trading the ETF even when the expense ratio looks low.

Trading volume can help describe visible market activity, but it does not fully explain ETF liquidity by itself. The liquidity of the underlying holdings, the presence of market makers, and the creation/redemption process can also matter.

How ETF Holdings Create Exposure

The holdings determine what the ETF actually gives exposure to. A fund may track a broad index, focus on one sector, hold bonds with a defined maturity profile, follow an active strategy, or use a more specialized exposure method. The ETF label alone does not reveal whether the portfolio is broad, concentrated, simple, complex, physical, synthetic, actively managed, or passively indexed.

This is where a common mistake appears. An investor may see “ETF” and assume diversification, low cost, or broad market exposure. Those are not automatic. A narrow sector ETF, a leveraged ETF, an active ETF, and a broad-market index ETF can all use the ETF wrapper while having very different risk, cost, tracking, and tax characteristics.

How the Creation and Redemption Process Supports ETF Structure

The creation and redemption process is the mechanism that connects ETF share supply to the fund’s underlying basket. Authorized participants can work with the ETF issuer to create or redeem large blocks of ETF shares, often called creation units. This activity usually happens in the primary market, not through ordinary small investor trades.

When ETF shares are created, the authorized participant generally delivers a defined basket of securities, cash, or both to the ETF. In return, the ETF issuer provides a block of ETF shares. When shares are redeemed, the process works in the opposite direction: the authorized participant returns ETF shares and receives the basket, cash, or both.

This process matters because it can help align ETF share supply with demand and support the relationship between market price and underlying value. The exact mechanics vary by fund, asset class, market condition, and structure, so creation and redemption mechanics should be reviewed separately when the creation unit process is central to the analysis.

Market Price, NAV, and ETF Value

An ETF has a market price and a net asset value. The market price is the price at which ETF shares trade on an exchange. NAV is an estimate of the value of the fund’s assets minus liabilities, usually expressed per share.

These two values are related, but they are not identical. ETF shares can trade close to NAV, above NAV, or below NAV. The gap can widen when the underlying assets are hard to price, when markets are volatile, when foreign markets are closed, or when liquidity is thin.

The creation and redemption process can help reduce persistent gaps, but it does not guarantee permanent alignment. Market price and NAV should be read together, especially for ETFs that hold less liquid assets, international securities, bonds, derivatives, or specialized exposures.

ETF Costs, Tracking, and Distributions

ETF mechanics also include cost and tracking checks. The expense ratio is the ongoing fund-level operating cost, but it is not the only cost an investor may face. Trading commissions where applicable, bid-ask spread, premium or discount behavior, tax treatment, and tracking difference can all affect the practical result.

Tracking describes how closely the ETF follows its intended exposure. A passive ETF may try to track an index, while an active ETF may follow a discretionary or rules-based investment process. Tracking can differ because of fees, sampling, cash drag, rebalancing, securities lending, market conditions, or structural choices.

Distributions are another part of the wrapper. Some ETFs distribute dividends, interest, or other income. The amount, timing, and tax treatment depend on the holdings, jurisdiction, fund structure, and investor situation.

ETF Mechanics and What Each Part Tells You

| ETF part | What it does | What it does not prove |

|---|---|---|

| Exchange-traded share | Allows investors to buy and sell ETF shares during the market day. | It does not prove the trade will be cheap, liquid, or close to NAV. |

| Underlying holdings | Create the economic exposure behind the ETF share. | They do not automatically create diversification or low risk. |

| NAV | Provides a reference value based on fund assets and liabilities. | It is not always the same as the market price at a specific trade time. |

| Creation and redemption | Connects large ETF share supply changes to the underlying basket. | It does not guarantee perfect price alignment in every market condition. |

| Expense ratio | Shows ongoing fund-level operating cost. | It does not include every practical trading, tax, spread, or tracking effect. |

| Tracking method | Explains how the fund seeks to follow its target exposure. | It does not guarantee identical performance to the index or strategy target. |

A Simple ETF Structure Scenario

Consider an ETF designed to follow a basket of large public companies. During the market day, an investor buys ETF shares on an exchange from another market participant. The investor now owns ETF shares, not the individual stocks directly.

Behind those shares, the fund holds or obtains exposure to the basket defined by its rules or strategy. If demand for ETF shares rises materially, authorized participants may create additional shares through the issuer by delivering the required basket or cash. If demand falls, shares may be redeemed in large blocks through the same institutional mechanism.

The investor’s actual experience still depends on more than the wrapper. The market price paid, the bid-ask spread, the fund holdings, the expense ratio, tracking behavior, distribution policy, liquidity, tax treatment, and premium or discount all affect interpretation.

What ETF Mechanics Do Not Tell You

ETF mechanics explain how the structure works, but they do not answer every investor question. The wrapper does not prove that the fund is diversified, suitable, tax efficient, low risk, low cost in practice, or likely to meet a specific objective.

Common mistake: treating ETF structure as a quality label. The better question is what the ETF holds, how it trades, how it tracks, what it costs, how liquid the exposure is, and what risks remain after the wrapper is understood.

The structure is a starting point for analysis, not a conclusion. A broad index ETF, a bond ETF, a commodity-linked ETF, a leveraged ETF, and an active ETF may all trade through the same general wrapper while behaving very differently.

What to Check Before Interpreting an ETF

| Check | Question to ask | Why it matters |

|---|---|---|

| Holdings | What does the ETF actually own or reference? | The holdings define the real exposure. |

| Market price and NAV | Is the ETF trading near, above, or below NAV? | Premiums and discounts can affect trade interpretation. |

| Spread and liquidity | How wide is the bid-ask spread and how liquid are the underlying assets? | Visible volume alone may not describe practical trading cost. |

| Expense ratio | What ongoing fund-level cost is charged? | The expense ratio is only one part of total cost review. |

| Tracking method | How does the fund seek to follow its target exposure? | Tracking behavior can vary by method, cost, and market conditions. |

| Distribution policy | Does the ETF distribute income or handle it differently? | Income handling can affect investor expectations and tax review. |

| Tax structure | What tax treatment applies to this ETF structure and investor location? | Tax outcomes vary and should not be assumed from the ETF wrapper alone. |

FAQ

Does an ETF always trade at NAV?

No. ETF market price and NAV are related, but they are not the same thing. ETF shares can trade at a premium or discount to NAV, especially when underlying markets are illiquid, closed, volatile, or difficult to price.

Who creates ETF shares?

ETF shares are created and redeemed in large blocks through authorized participants and the ETF issuer. Ordinary investors usually buy and sell existing ETF shares on an exchange in the secondary market.

Does the ETF wrapper make a fund diversified?

No. Diversification depends on the holdings and strategy. An ETF can be broad, narrow, concentrated, leveraged, actively managed, or specialized, so the wrapper alone does not prove diversification.

How does an active ETF work?

An active ETF still uses the exchange-traded fund wrapper, but its holdings are selected through an active investment process rather than simply tracking a fixed index. The basic trading layer is similar, while the portfolio decision process differs.