An equity ETF is an exchange-traded fund that holds stocks or stock-based exposure. The label tells you the fund belongs to the equity category, but it does not tell you enough about the actual holdings, weighting method, costs, liquidity, distributions, tracking behavior, or tax context.

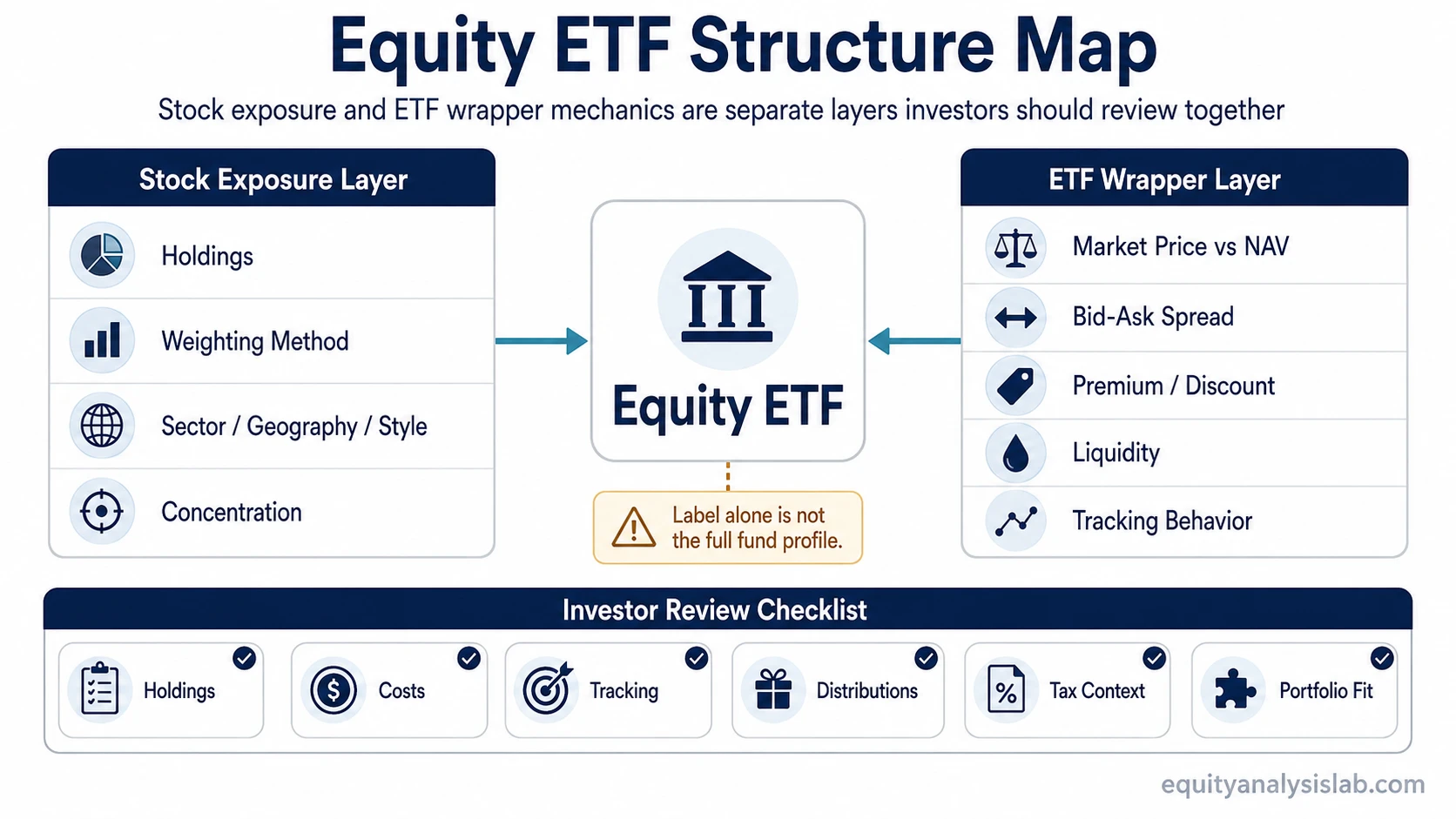

The useful way to read an equity ETF is to separate two layers. The first layer is the stock exposure: what the fund owns and how those holdings are weighted. The second layer is the ETF wrapper: how the fund trades on an exchange, how market price relates to net asset value, and how liquidity, spreads, tracking, and distributions can affect the investor’s experience.

What Is an Equity ETF?

An equity ETF is a fund that trades on an exchange and provides exposure to equities, usually through a basket of stocks. Some equity ETFs track an index, while others follow an active, factor, sector, dividend, thematic, style, or geographic strategy.

“Equity ETF” and “stock ETF” are often used to describe the same broad idea: an ETF whose main exposure comes from stocks rather than bonds, commodities, currencies, or cash-like instruments. The important point is that the equity label identifies the asset class, not the quality, risk, diversification, cost, or tax profile of the specific fund.

Key Points About Equity ETFs

- An equity ETF gives investors stock-market exposure through an exchange-traded fund wrapper.

- The fund may hold broad-market stocks, sector stocks, international stocks, dividend stocks, factor stocks, or a more concentrated equity strategy.

- The holdings and weighting method determine much of the real exposure, not the label alone.

- The ETF wrapper adds trading considerations such as market price, NAV, bid-ask spread, premium or discount, and secondary-market liquidity.

- Costs include more than the headline fee; tracking difference, trading spreads, and tax/distribution effects can also matter.

- Equity ETFs can diversify stock exposure, but they can also be concentrated by sector, theme, geography, factor, or market capitalization.

- An equity ETF is not a fund recommendation. It is a structure that still requires holdings, cost, liquidity, distribution, and risk review.

How an Equity ETF Creates Stock Exposure

The equity exposure layer starts with the fund’s holdings. A broad-market equity ETF may hold many companies across sectors, while a sector or thematic equity ETF may hold a narrower group of stocks tied to one industry, theme, region, or factor.

Weighting matters as much as the number of holdings. A market-cap-weighted fund can be heavily influenced by the largest companies in the portfolio. An equal-weighted, factor-weighted, dividend-weighted, or actively selected fund can produce a different risk profile even when it still belongs to the equity ETF category.

Investors usually need to look at several exposure questions together: which companies are held, how concentrated the top holdings are, which sectors dominate, whether the fund is domestic or international, and whether the strategy tilts toward value, growth, quality, dividends, momentum, low volatility, or another factor.

ETF Wrapper Mechanics: Market Price, NAV, and Liquidity

An equity ETF trades on an exchange during the trading day, so investors see a market price. The fund also has a net asset value, or NAV, based on the value of the underlying portfolio. The market price and NAV are usually connected, but they are not the same thing.

When reviewing an equity ETF, the wrapper layer includes the bid-ask spread, trading volume, underlying holdings liquidity, premium or discount behavior, and how efficiently the fund tracks its stated strategy. For a deeper explanation of the trading layer, see ETF liquidity.

The wrapper does not remove stock-market risk. It changes how the exposure is packaged and traded. A fund can be easy to buy and sell on an exchange while still holding equities that move sharply, concentrate in a narrow theme, or behave differently from the broad market.

Types of Equity ETF Exposure

Equity ETFs can be grouped by the kind of stock exposure they provide. The same wrapper can hold very different portfolios, so the type of equity exposure should be reviewed before comparing costs or recent returns.

| Equity ETF type | What it usually emphasizes | Main review point |

|---|---|---|

| Broad-market equity ETF | Large segments of the stock market | Index coverage, concentration, and market-cap weighting |

| Sector equity ETF | One sector such as technology, healthcare, energy, or financials | Sector concentration and cycle sensitivity |

| Style equity ETF | Value, growth, blend, large-cap, mid-cap, or small-cap exposure | Style definition and how holdings are selected |

| Dividend equity ETF | Stocks selected or weighted around dividends | Dividend quality, distribution policy, and sector concentration |

| International equity ETF | Stocks outside the investor’s home market | Country exposure, currency effects, and market structure |

| Factor or thematic equity ETF | A factor screen or investment theme | Rules, concentration, turnover, and whether the theme is narrow |

| Active equity ETF | Manager-selected stock exposure rather than pure index tracking | Process, disclosure, cost, and manager discretion |

An actively managed ETF may still be an equity ETF if its main portfolio exposure is stocks. The difference is that the active process adds manager discretion to the stock selection and portfolio-management layer.

What to Check Before Comparing Equity ETFs

Two equity ETFs can share the same category label and still behave differently. A useful comparison starts with the exposure, then moves to the wrapper mechanics and costs.

| Checklist item | Why it matters | Question to ask |

|---|---|---|

| Holdings | Shows what the fund actually owns | Are the holdings broad, narrow, diversified, or concentrated? |

| Weighting method | Determines which stocks drive the fund most | Is the fund market-cap weighted, equal weighted, factor weighted, or actively selected? |

| Index or strategy | Defines the rules or process behind the portfolio | Is the fund tracking an index, following a screen, or using active management? |

| Expense ratio | Directly reduces the investor’s fund-level return before other effects | Is the fee reasonable for the exposure and process being offered? |

| Tracking behavior | Shows how closely the fund follows its intended benchmark or strategy | Does the fund’s return pattern match the exposure it claims to deliver? |

| Trading liquidity | Affects transaction costs and execution quality | Are bid-ask spreads and trading conditions appropriate for the investor’s order size? |

| Distributions | Shapes the cash income pattern and taxable reporting context | What kinds of distributions does the fund make, and how consistent are they? |

| Tax context | Tax treatment can depend on account type, distribution classification, turnover, fund reporting, and the investor’s circumstances. | Could dividends, capital gains distributions, or trading activity create taxable events? |

The expense ratio is important, but it should not be the only comparison point. A lower-fee fund can still be less suitable for a specific investor if the holdings, concentration, tracking behavior, or liquidity profile do not match the intended exposure.

Tracking also deserves a separate review. A fund can have a clear benchmark or strategy but still differ from it because of fees, sampling, turnover, cash drag, trading costs, or portfolio implementation. That is why tracking difference belongs in the comparison process rather than being treated as a technical afterthought.

Common Misunderstandings About Equity ETFs

The equity ETF label does not automatically mean broad diversification. Some equity ETFs hold hundreds or thousands of stocks, while others focus on one sector, theme, geography, factor, or narrow portfolio segment.

The ETF wrapper does not eliminate stock-market risk. The fund can still decline if the underlying equities fall, if the dominant sector weakens, or if the strategy is concentrated in a fragile area of the market.

A lower fee is not the whole decision. Fees matter, but so do holdings, tracking behavior, liquidity, distribution policy, tax context, and how the fund fits with the investor’s broader portfolio.

Equity ETF dividends are not automatically stable or tax-free. Distributions depend on the underlying stocks, fund policy, turnover, reporting, account type, and investor circumstances. The equity ETF structure may influence tax mechanics, but it does not remove tax considerations.

Liquidity needs more than one number. Trading volume can be useful, but the underlying holdings, bid-ask spread, market conditions, and order size can also affect the trading experience.

Illustrative Scenario: Same Label, Different Exposure

Consider two hypothetical equity ETFs. The first holds a broad basket of large and mid-sized companies across many sectors and weights them mostly by market capitalization. The second holds a smaller group of companies tied to one fast-growing theme and has a large portion of its portfolio in a few names.

Both funds can correctly be called equity ETFs because both provide stock exposure through an ETF wrapper. But they do not offer the same investor experience. The broad fund may behave more like diversified stock-market exposure, while the concentrated thematic fund may be driven by a narrower set of companies, sector conditions, valuation changes, and investor sentiment around that theme.

The lesson is that the label identifies the category. The holdings, weights, strategy, costs, trading conditions, distributions, and tax context determine what the investor actually owns.

Equity ETFs Compared With Other ETF Types

An equity ETF is defined by stock exposure, but other ETF types use the same exchange-traded wrapper for different kinds of exposure. A bond ETF focuses on fixed-income exposure, where interest-rate sensitivity, credit quality, maturity, and yield mechanics become central review points.

A commodity ETF is different again because the exposure may relate to commodities, futures, or commodity-linked structures rather than operating companies. That can create different risks around roll mechanics, storage-linked economics, commodity cycles, or structure-specific tax treatment.

Index ETFs and actively managed ETFs can overlap with equity ETFs. An equity ETF may track a stock index, or it may use active management. The category tells you the asset class, while the strategy tells you how the portfolio is built.

Where Equity ETF Review Fits in an Investor Process

A practical review usually moves in this order: identify the stock exposure, understand the portfolio construction rules, review the ETF wrapper mechanics, compare costs and tracking behavior, then consider distributions, taxes, and portfolio fit.

| Review layer | What it answers | Why it matters before comparison |

|---|---|---|

| Exposure | What stocks does the fund own? | It defines the core risk and return drivers. |

| Construction | How are holdings selected and weighted? | It explains why two equity ETFs can behave differently. |

| Wrapper | How does the fund trade and track its portfolio? | It affects execution, spread, premium/discount, and tracking review. |

| Costs and distributions | What costs and cash flows may affect the investor? | It connects the fund structure to the investor’s after-cost and taxable-account context. |

| Portfolio fit | What role would the exposure play? | It prevents the investor from treating every equity ETF as interchangeable. |

FAQ

Is an equity ETF the same as a stock ETF?

In most investor education contexts, equity ETF and stock ETF refer to the same broad category: an ETF whose main exposure comes from stocks. The exact risk profile still depends on the holdings, weighting method, strategy, liquidity, costs, and distributions.

Are equity ETFs automatically diversified?

No. Some equity ETFs are broad and diversified, while others are concentrated in one sector, theme, factor, geography, or small group of holdings. The number of holdings and the weighting method should be reviewed before assuming diversification.

Do equity ETFs pay dividends?

Many equity ETFs distribute dividends received from underlying stocks, but the amount, timing, and classification of distributions depend on the fund’s holdings, policy, turnover, reporting, account type, and investor circumstances. A dividend label is not enough to determine income quality or tax treatment.

How is an equity ETF different from a bond ETF?

An equity ETF mainly holds stocks or stock-based exposure. A bond ETF focuses on fixed-income exposure, where interest-rate sensitivity, credit quality, maturity profile, and income mechanics become more important review points.