A leveraged ETF is an exchange-traded fund that seeks to deliver a multiple of the daily return of a benchmark, index, asset, or basket. The important word is daily: a 2x or 3x objective is usually measured over one trading day, not automatically over a month, year, or full holding period.

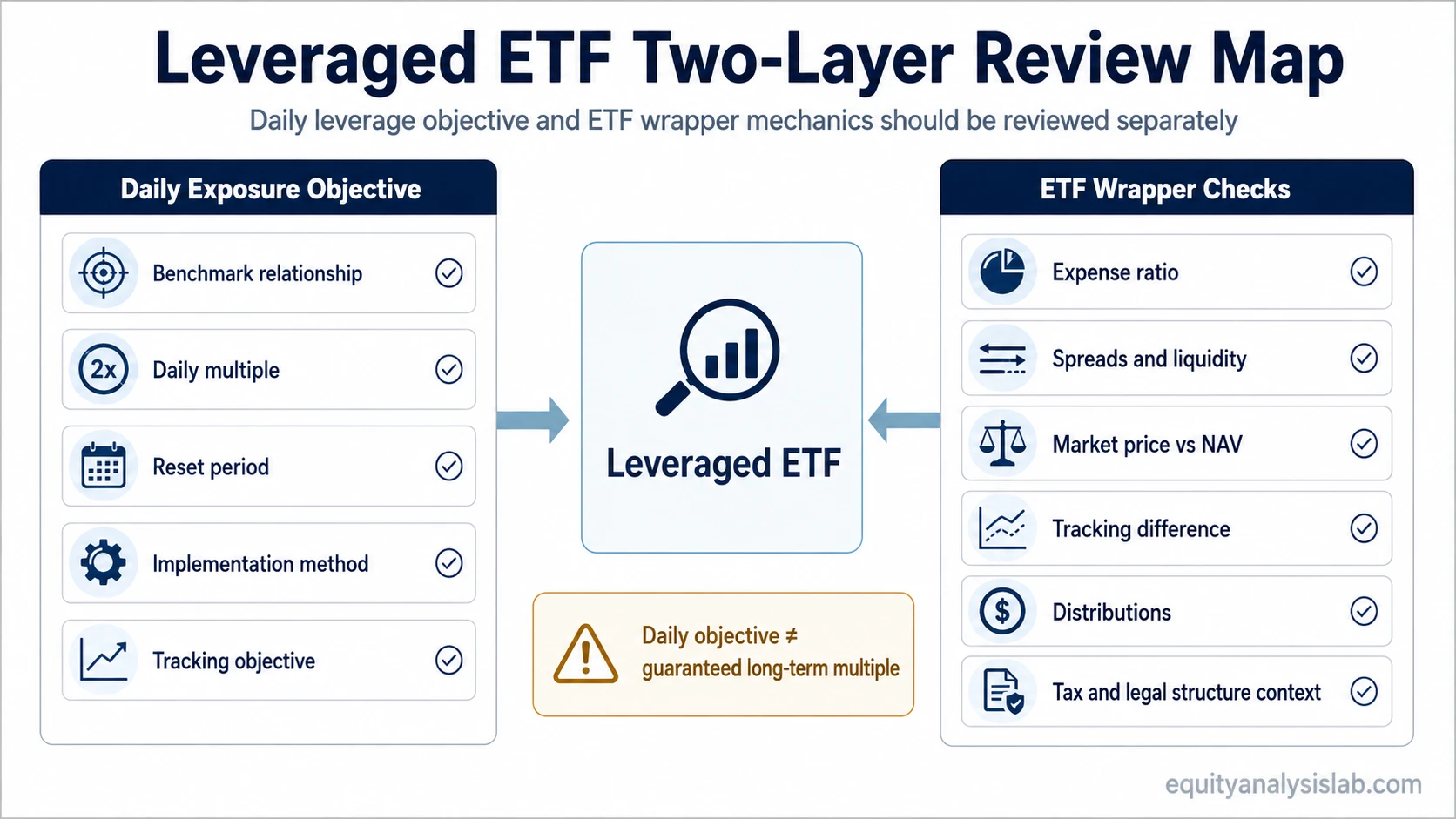

The leveraged label does not describe the whole fund. Before interpreting a leveraged ETF, investors need to separate the daily exposure objective from the ETF wrapper itself. The first layer is the benchmark relationship, leverage multiple, reset period, and implementation method. The second layer is the fund wrapper: cost, liquidity, market price versus NAV, tracking behavior, distributions, and tax or legal structure context.

Definition: A leveraged ETF is an ETF designed to provide amplified daily exposure, such as 2x or 3x, to a benchmark or underlying exposure. Because the exposure is reset regularly, longer-period results can differ from simply multiplying the benchmark’s total return by the stated leverage factor.

Key Points

- A leveraged ETF targets a stated multiple of a benchmark’s daily return, commonly described with terms such as 2x or 3x.

- The daily reset is central. The fund’s objective is usually not a guaranteed multiple of the benchmark over longer holding periods.

- Compounding and path dependency can make longer-term results differ from a simple leverage calculation.

- Leveraged ETFs often use derivatives such as swaps and futures contracts, and some funds may use other financing or collateral arrangements disclosed in their fund documents.

- The ETF wrapper still matters: expenses, spreads, liquidity, NAV behavior, tracking, distributions, and tax structure can all affect interpretation.

What Is a Leveraged ETF?

A leveraged ETF is a fund wrapper built around an amplified exposure objective. Instead of seeking a one-for-one daily relationship with an index or asset, it seeks a multiple of that daily movement. A 2x leveraged ETF seeks about twice the daily move of its benchmark before costs and tracking effects. A 3x leveraged ETF seeks about three times the daily move.

The benchmark can vary. Some leveraged ETFs reference equity indexes, sectors, commodities, bonds, currencies, or other assets. The benchmark relationship should be identified before any cost, liquidity, or portfolio interpretation is made. The structure tied to a broad index is not the same exposure as one tied to a narrow sector, commodity, or single market segment.

A leveraged ETF is also different from a standard index ETF. A standard index ETF usually seeks to track the benchmark as closely as possible on a one-for-one basis. The daily objective seeks amplified exposure, so the benchmark relationship and reset mechanics become part of the basic definition.

How a Leveraged ETF Creates Leveraged Exposure

The fund usually does not create amplified exposure only by holding more of the underlying stocks or assets. Leveraged ETFs often use derivatives such as swaps and futures contracts, and some funds may use other financing or collateral arrangements disclosed in their fund documents. The exact implementation depends on the fund, its benchmark, its jurisdiction, and its prospectus.

The practical question is not only “what does the fund own?” but “what exposure is the fund designed to deliver each day?” Holdings, derivative positions, collateral, cash, and financing arrangements can all be part of the structure. For that reason, the holdings list should be read together with the stated investment objective and benchmark.

| Mechanic | What to identify | Why it matters |

|---|---|---|

| Benchmark relationship | The index, asset, sector, commodity, bond exposure, or basket the ETF references. | The leverage multiple only has meaning after the underlying exposure is clear. |

| Leverage multiple | The stated daily objective, such as 2x or 3x. | The multiple describes the target daily exposure, not a simple long-term promise. |

| Reset period | How frequently the fund resets its exposure, commonly daily. | The reset period affects compounding and longer-period interpretation. |

| Implementation tools | Derivatives such as swaps and futures contracts, plus any financing or collateral arrangements disclosed in fund documents. | The fund may behave differently from a simple basket of physical holdings. |

| Tracking objective | The return relationship the fund seeks before expenses and market frictions. | Tracking should be judged against the fund’s stated objective, not only against the benchmark headline. |

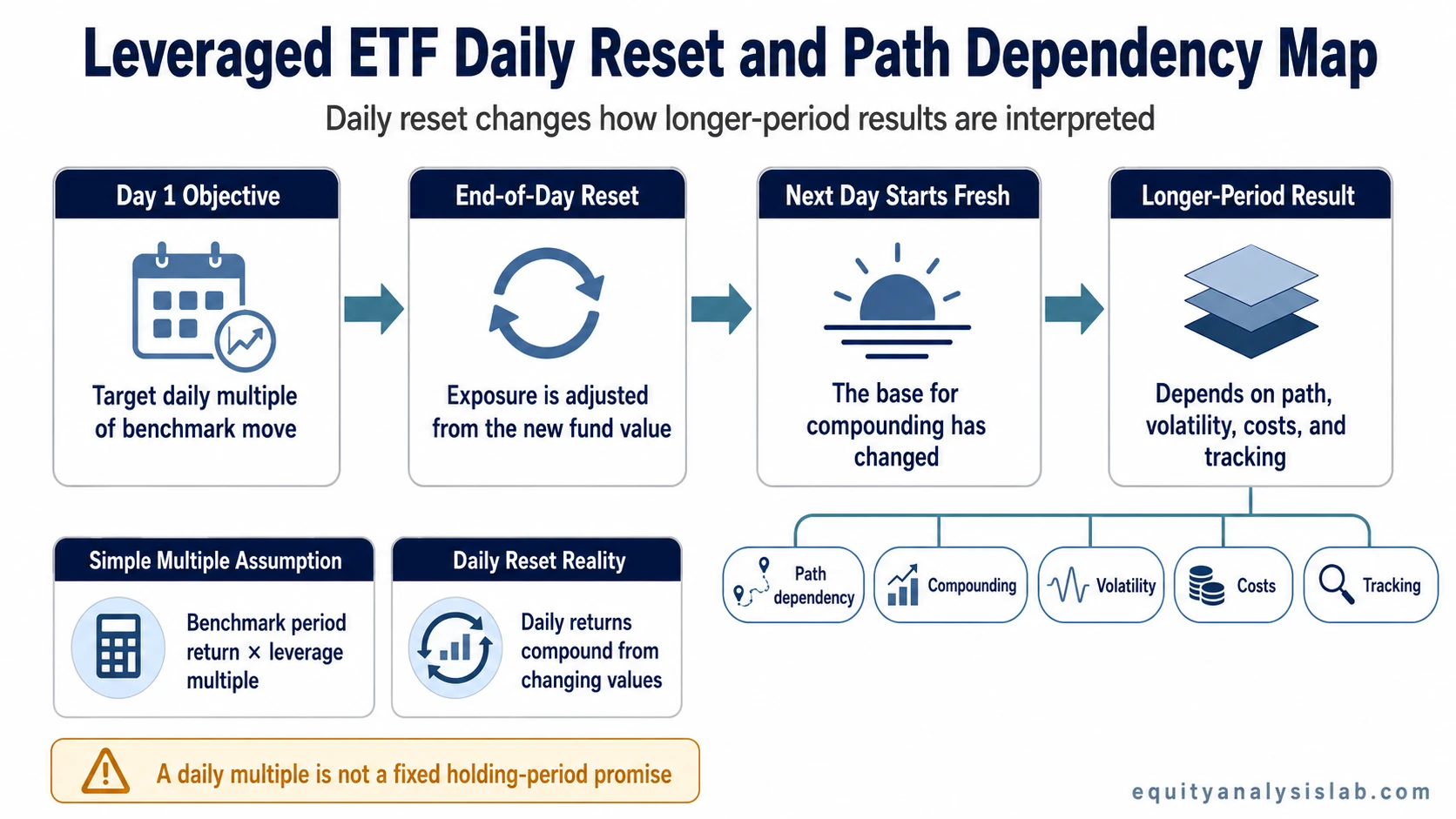

How Daily Reset Changes the Interpretation

The daily reset is the main reason leveraged ETFs can behave differently from a simple long-term leverage calculation. If a fund targets 2x the daily return of a benchmark, the exposure is adjusted after each day. The next day begins from a new fund value and a newly targeted exposure level.

This creates path dependency. The order of daily returns matters. A benchmark that moves up and down across several days can leave a leveraged ETF with a result that differs from multiplying the benchmark’s total period return by two or three. The effect can be favorable in a persistent trend and unfavorable in a choppy path, but the result depends on the sequence of returns, volatility, costs, and tracking quality.

Illustrative example: Suppose a benchmark starts at 100, rises 10% on day one, and then falls about 9.09% on day two. The benchmark ends close to where it started. A 2x daily leveraged ETF would rise about 20% on day one, then fall about 18.18% from the higher day-one value on day two, before costs and tracking effects. The two-day result is not zero, even though the benchmark is roughly flat.

The example is simplified, but it shows why the daily objective and longer-period result are separate ideas. The fund can match its daily objective reasonably well and still produce a longer-period result that surprises investors who expected a fixed multiple over the full holding period.

Compounding, Path Dependency, and Volatility Drag

Compounding means each day’s return is applied to the value left by previous days. In a leveraged ETF, the daily return is amplified, so the compounding effect can become more visible. A smooth directional path can produce a different outcome from a volatile path, even when the benchmark’s start and end points look similar.

Path dependency means the sequence of daily returns affects the final result. Two benchmarks can have the same total return over a period but different daily paths. This wrapper can produce different results because exposure resets along the way.

Volatility drag is a common way to describe the adverse effect that repeated up-and-down moves can have on compounded returns. The term should not be treated as a prediction that every leveraged ETF must lose value over every period. It is a warning that volatility, reset mechanics, and holding period interact in ways that a simple leverage multiple does not capture.

Traditional ETF vs Leveraged ETF

A traditional ETF and a leveraged ETF can both trade on an exchange, publish a market price, and operate through a fund wrapper. The difference is the exposure objective. A traditional ETF usually seeks ordinary exposure to its benchmark. A leveraged ETF seeks amplified daily exposure and therefore requires a separate check of reset mechanics and compounding behavior.

| Feature | Traditional ETF | Leveraged ETF |

|---|---|---|

| Exposure objective | Usually seeks one-for-one benchmark exposure. | Seeks a multiple of benchmark daily exposure. |

| Reset mechanics | Reset mechanics are usually less central to the basic return objective. | Daily reset is central to how results are interpreted. |

| Use of derivatives | May use derivatives, but many broad ETFs hold physical securities directly. | Often uses derivatives such as swaps and futures contracts; some funds may also use disclosed financing or collateral arrangements. |

| Longer-period interpretation | Usually compared against benchmark tracking over time. | Must account for daily compounding and path dependency. |

| Primary review question | How closely does the ETF track its benchmark after costs? | What daily exposure is targeted, and how do reset mechanics affect longer-period results? |

Leveraged ETF Two-Layer Check

The leveraged label should be separated into two layers. The first layer is the daily exposure objective. The second layer is the ETF wrapper. A fund can have a clear leverage objective while still requiring careful review of its costs, liquidity, tracking behavior, distributions, and structure.

| Layer | What to check | Interpretation question |

|---|---|---|

| Daily Exposure Objective | Benchmark or underlying asset | What exposure is being amplified? |

| Daily Exposure Objective | Leverage multiple | Is the fund targeting 2x, 3x, or another daily multiple? |

| Daily Exposure Objective | Reset period | Is the objective measured daily or over another reset period? |

| Daily Exposure Objective | Derivatives, financing, and collateral mechanism | How is the leveraged exposure created? |

| Daily Exposure Objective | Compounding and path dependency | How could the daily path change longer-period results? |

| ETF Wrapper Observables | Expense ratio and fund costs | What explicit cost is charged by the fund, and what other frictions may matter? |

| ETF Wrapper Observables | Holdings and derivative exposure | Do the holdings, derivative positions, collateral, or cash positions match the stated objective? |

| ETF Wrapper Observables | Liquidity and spread | How easily can shares trade, and how wide is the bid-ask spread? |

| ETF Wrapper Observables | NAV vs market price | Does the market price stay close to the fund’s net asset value? |

| ETF Wrapper Observables | Tracking difference | How closely does the fund deliver its stated daily objective after costs and frictions? |

| ETF Wrapper Observables | Distributions and tax / legal structure context | Could income, capital gains, jurisdiction, or fund structure affect after-tax interpretation? |

What to Check Before Interpreting a Leveraged ETF

The fund name is only the starting point. A leveraged ETF should be read through its stated objective, benchmark, reset period, holdings, derivatives, and wrapper details. Without those checks, the label can create a false sense of simplicity.

Benchmark: Identify the exact index, asset, sector, commodity, bond exposure, or basket being referenced. A leveraged broad-market fund and a leveraged narrow-sector fund can carry very different exposure profiles.

Daily multiple: Check whether the fund targets 2x, 3x, or another multiple. The multiple should be tied to the stated reset period, not assumed to apply automatically over any holding period.

Reset period: Confirm how the fund resets exposure. Daily reset language changes how compounding and longer-period results should be interpreted.

Implementation: Review whether the fund uses derivatives such as swaps and futures contracts, physical holdings, cash, or fund-document-specific financing or collateral arrangements. The exposure mechanism can affect tracking and risk behavior.

Costs and trading frictions: The expense ratio is not the only cost lens. Spreads, tracking differences, financing costs, and market price deviations can also matter.

Wrapper structure: Distributions, tax treatment, legal domicile, and fund structure may affect interpretation. Product-specific tax or distribution conclusions require the fund’s own documents and the investor’s jurisdiction.

Common Misunderstanding About Leveraged ETFs

Limitation: A leveraged ETF’s daily multiple is not the same thing as a guaranteed long-term multiple. A 2x daily objective does not mean the fund must deliver exactly twice the benchmark’s return over every month, year, or investor-selected holding period.

The misunderstanding usually comes from reading the leverage number without reading the reset period. Daily reset creates a moving base. Each day’s gain or loss changes the value from which the next day’s amplified return is calculated.

Another mistake is assuming the leveraged label answers questions about diversification, liquidity, cost, tracking, or tax treatment. It does not. Those features belong to the wrapper layer and must be checked separately.

Leveraged ETF vs Inverse ETF

A leveraged ETF and an inverse ETF are related but not identical. A leveraged ETF refers to amplified exposure. An inverse ETF refers to opposite-direction exposure. Some funds can be both leveraged and inverse, but the two labels answer different questions.

The cleaner distinction is direction versus multiple. Leveraged exposure asks how much daily exposure the fund seeks relative to a benchmark. Inverse exposure asks whether the fund seeks to move opposite to the benchmark. A full comparison belongs in leveraged vs inverse ETF, because the overlap can otherwise distract from the daily reset mechanics of leveraged funds.

Nearby ETF Types

Leveraged ETFs can reference many kinds of underlying exposures. Some are tied to broad indexes, while others reference sectors, commodities, bonds, currencies, or other assets. The underlying exposure should be understood before the leverage multiple is interpreted.

An actively managed ETF is different because the defining feature is manager discretion rather than a daily leverage multiple. A bond ETF is defined by fixed-income exposure, while a commodity ETF is defined by commodity-linked exposure. Those categories can have their own wrapper mechanics, but leverage should be analyzed as a separate exposure feature.

FAQ

Is a leveraged ETF designed for long-term multiple returns?

A leveraged ETF is usually designed around a daily multiple objective. Longer-term results can differ from a simple multiple of the benchmark’s total return because daily reset, compounding, volatility, costs, and tracking effects all matter.

Is a leveraged ETF the same as an inverse ETF?

No. Leveraged exposure refers to amplified exposure, while inverse exposure refers to opposite-direction exposure. A fund can be both leveraged and inverse, but the two labels describe different mechanics.

Does the expense ratio show the full cost of a leveraged ETF?

No. The expense ratio is only one visible cost measure. Spreads, financing costs, tracking difference, market price versus NAV behavior, and trading frictions can also affect the investor’s result.

Does a leveraged ETF always hold the underlying stocks or assets directly?

Not always. Many leveraged ETFs use derivatives such as swaps and futures contracts, and some funds may use other financing or collateral arrangements disclosed in their fund documents. The stated objective, holdings disclosure, and prospectus should be reviewed for the specific structure.