An inverse ETF is an exchange-traded fund designed to seek the opposite daily return of a stated benchmark. If the benchmark falls by 1% in a single trading day, a -1x inverse ETF generally aims to rise by about 1% before fees, expenses, tracking effects, and market-price differences.

The inverse label does not describe the full investor experience. Reset frequency, compounding, derivative implementation, costs, liquidity, tracking difference, distributions, and tax or structure mechanics can all affect how the fund behaves after the headline exposure is understood.

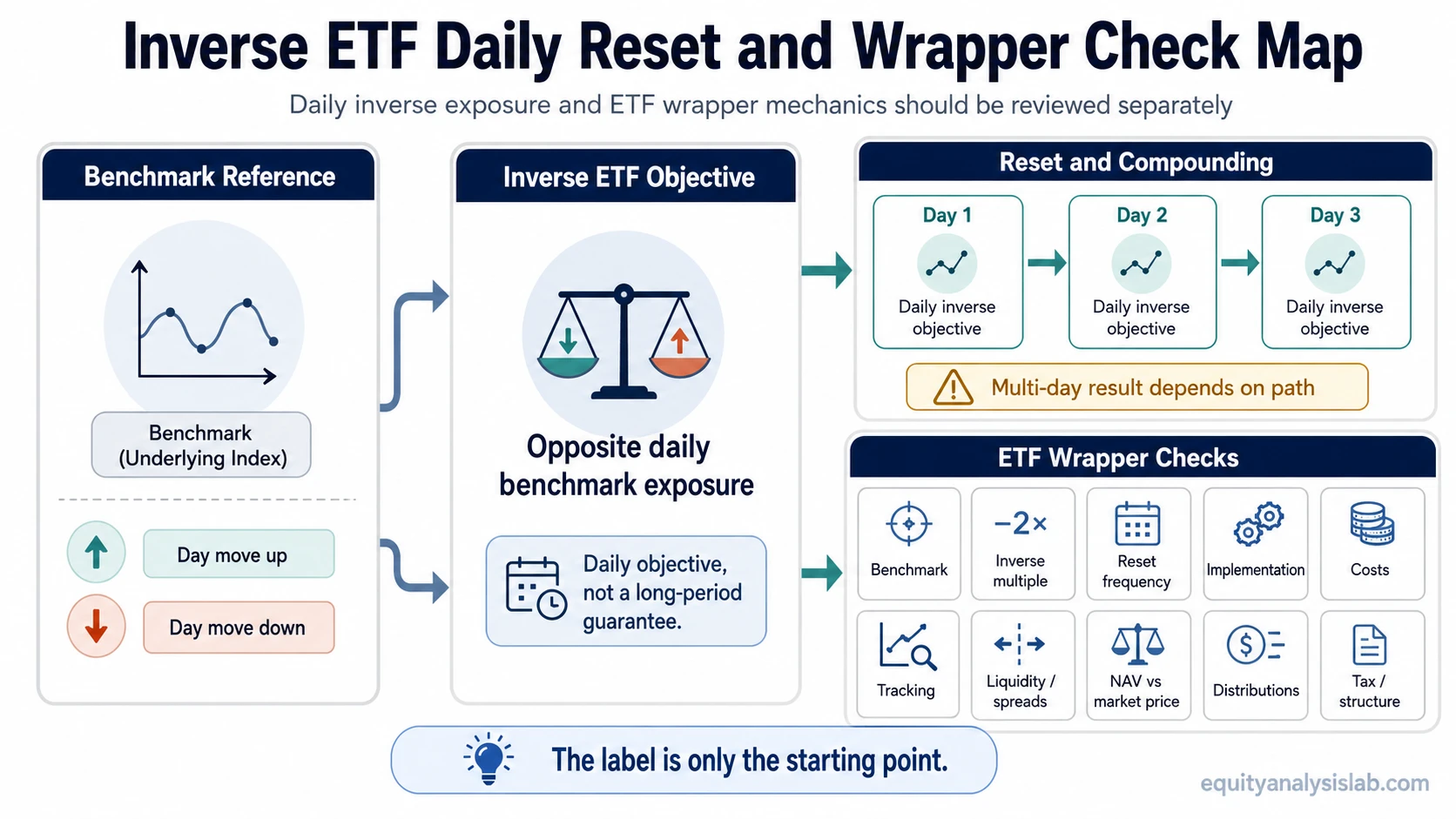

What Is an Inverse ETF?

An inverse ETF is an ETF wrapper that seeks negative exposure to a benchmark, usually on a daily basis. The benchmark may be a stock index, sector index, bond benchmark, commodity reference, or another defined market measure.

The key word is daily. Most inverse ETFs are built to pursue the opposite of the benchmark’s daily move, not to guarantee the opposite return over a week, month, year, or full market cycle. Over longer periods, compounding can make the result differ from a simple inverse reading of the benchmark’s total move.

Key Points About Inverse ETFs

- An inverse ETF seeks opposite exposure to a benchmark, commonly at -1x of the benchmark’s daily return.

- The fund usually creates that exposure through derivatives, swaps, futures, short exposure, or a combination of instruments rather than by simply holding the benchmark backward.

- Daily reset and compounding can make multi-day results differ from the benchmark’s simple opposite return.

- Costs, tracking difference, bid-ask spreads, trading volume, NAV versus market price, and distribution mechanics can matter as much as the inverse label.

- An inverse ETF is not the same thing as a fund recommendation, a hedge instruction, or a prediction that a benchmark will fall.

How an Inverse ETF Creates Inverse Exposure

An ordinary ETF usually holds assets or instruments intended to move in the same direction as its benchmark. An inverse ETF is different because its objective is to move in the opposite direction of the benchmark for the stated reset period.

To create that exposure, the fund may use derivatives such as swaps, futures contracts, short positions, or other instruments described in its fund documents. The exact implementation matters because two inverse ETFs can share a similar label while using different instruments, collateral practices, costs, and tracking methods.

The benchmark relationship should be read before the fund name. “Inverse” only tells the direction of intended exposure. It does not tell the benchmark, the multiple, the reset period, the implementation method, the liquidity profile, or the expected tracking quality.

A Simple Daily Move Example

Suppose a benchmark declines by 1% during one trading day. A -1x inverse ETF linked to that benchmark would generally seek a gain of about 1% for that same day before fund expenses, financing costs, tracking effects, bid-ask spreads, and market-price differences.

If the benchmark rises by 1% during one trading day, the same -1x inverse ETF would generally seek a loss of about 1% before those same frictions. This example is only a simplified daily illustration. It is not a forecast, recommendation, or statement about any live fund.

Why Daily Reset and Compounding Matter

Daily reset means the fund’s exposure is generally recalibrated around a daily objective. That design creates a common misunderstanding: a daily inverse ETF is not simply the opposite of the benchmark’s total return over every longer period.

Compounding changes the path. If the benchmark moves down, up, down, and up across several sessions, the inverse ETF’s result depends on the sequence of those daily moves, not only on the final benchmark level. Volatile sideways markets can be especially confusing because daily gains and losses compound from changing starting values.

The longer the holding period and the more volatile the path, the more important this distinction becomes.

Inverse ETF vs Ordinary ETF

| Feature | Ordinary ETF | Inverse ETF |

|---|---|---|

| Main exposure direction | Usually seeks to move with the benchmark. | Seeks to move opposite the benchmark for the stated reset period. |

| Typical benchmark relationship | Positive benchmark exposure. | Negative benchmark exposure, commonly stated as -1x or another inverse multiple. |

| Implementation | May hold securities, bonds, commodities exposure, derivatives, or other instruments depending on fund type. | Often relies on derivatives, swaps, futures, short exposure, or similar tools to create inverse exposure. |

| Main interpretation risk | Assuming the label fully explains holdings, costs, liquidity, or tracking. | Assuming daily inverse exposure equals a simple opposite return over longer periods. |

Inverse ETF vs Leveraged ETF

An inverse ETF changes the direction of exposure. A leveraged ETF changes the magnitude of exposure. Some funds can be both inverse and leveraged, such as a fund that seeks -2x or -3x of a benchmark’s daily move.

This distinction matters because “inverse” and “leveraged” answer different questions. Inverse describes opposite direction. Leveraged describes amplified exposure. A plain -1x inverse ETF is not the same as a leveraged ETF, although both can involve reset mechanics, compounding effects, and derivative-based implementation.

What to Check Before Interpreting an Inverse ETF Label

The fund label is only the starting point. Before comparing or interpreting an inverse ETF, the investor should separate exposure design from ETF wrapper mechanics.

Fund comparison should begin with the stated objective and structure before moving to fund-level data such as cost, liquidity, tracking, and distributions.

| Check | Why it matters |

|---|---|

| Benchmark | The inverse exposure is tied to a specific benchmark, not to “the market” in general. |

| Inverse multiple | A -1x, -2x, or -3x objective can create very different exposure and risk characteristics. |

| Reset frequency | Daily reset can make longer-period results path-dependent. |

| Implementation method | Swaps, futures, short exposure, and collateral practices can affect tracking and risk. |

| Expense ratio and financing costs | Costs reduce realized results and may matter more over longer holding periods. |

| Tracking difference | The fund may not match its stated objective perfectly after fees, market conditions, and implementation effects. |

| Liquidity and bid-ask spread | Trading costs can widen the gap between the intended exposure and the investor’s actual entry or exit result. |

| NAV versus market price | The exchange-traded price may differ from net asset value, especially when markets are stressed or trading is thin. |

| Distribution policy | Distributions can affect total-return interpretation and tax reporting. |

| Tax and structure mechanics | Tax treatment, domicile, instrument structure, and ETF versus ETN differences may change the investor experience. |

Common Misunderstanding: The Label Is Not the Outcome

The most common mistake is treating an inverse ETF as a simple long-term mirror image of its benchmark. That reading ignores daily reset, compounding, costs, spreads, tracking difference, and the gap between fund NAV and market price.

An inverse ETF may be designed around short-term inverse benchmark exposure, but that does not make it a universal hedge, a long-term accumulation vehicle, or a substitute for reading the fund documents. The stated objective should be interpreted together with the wrapper mechanics and the investor’s own risk, tax, and time-horizon constraints.

Inverse ETF vs Short Selling

An inverse ETF and short selling can both create exposure that benefits from a benchmark or asset declining, but they are not the same structure. Short selling involves borrowing and selling a security directly, with its own margin, borrowing, recall, and risk mechanics. An inverse ETF packages negative exposure inside an exchange-traded fund wrapper.

The wrapper can make the exposure easier to access through a brokerage account, but it does not remove the need to understand reset mechanics, costs, liquidity, tracking, and fund structure. The ETF format changes the vehicle; it does not make inverse exposure simple.

ETF vs ETN Boundary

Some inverse products may be exchange-traded notes rather than ETFs. An ETN is typically a debt obligation of an issuer, while an ETF is a fund structure. That difference can introduce issuer-credit, structure, tax, and document-review considerations.

An inverse ETF and an inverse ETN should not be treated as the same vehicle. If a product is an ETN, ETF mechanics should not be assumed without checking the product’s legal structure and issuer documents.

Related ETF Type Boundaries

Inverse ETFs sit inside a broader ETF type map. An index ETF usually helps explain benchmark-following exposure, while inverse ETFs explain the opposite-direction version of benchmark exposure. An actively managed ETF raises a different question: who or what decides the portfolio rather than whether the exposure is inverse.

Other ETF types have separate exposure questions. A bond ETF may center on duration, credit, yield, and interest-rate sensitivity. A fund with commodity-linked exposure may require a separate review of futures, rolls, collateral, and physical or derivative structure, which is why a commodity ETF should not be interpreted through the inverse ETF label alone.

FAQ

Is an inverse ETF the same as short selling?

No. Both can create negative exposure, but short selling involves borrowing and selling a security directly, while an inverse ETF packages negative exposure inside an ETF wrapper with its own reset, tracking, cost, and liquidity mechanics.

Why do inverse ETFs reset daily?

Many inverse ETFs are designed around a daily objective, so exposure is recalibrated around daily benchmark movement. That daily reset is why longer-period results can differ from a simple opposite reading of the benchmark’s total move.

Is every inverse ETF leveraged?

No. A -1x inverse ETF seeks the opposite of the benchmark’s daily move without additional leverage beyond the inverse direction. A -2x or -3x product is both inverse and leveraged because it seeks opposite exposure with amplified magnitude.

Can an inverse ETF be held long term?

The answer depends on the fund objective, reset period, compounding path, costs, tracking, liquidity, tax context, and the investor’s purpose. Many inverse ETFs are designed for short-term daily objectives, so long-term interpretation requires extra caution and document review.