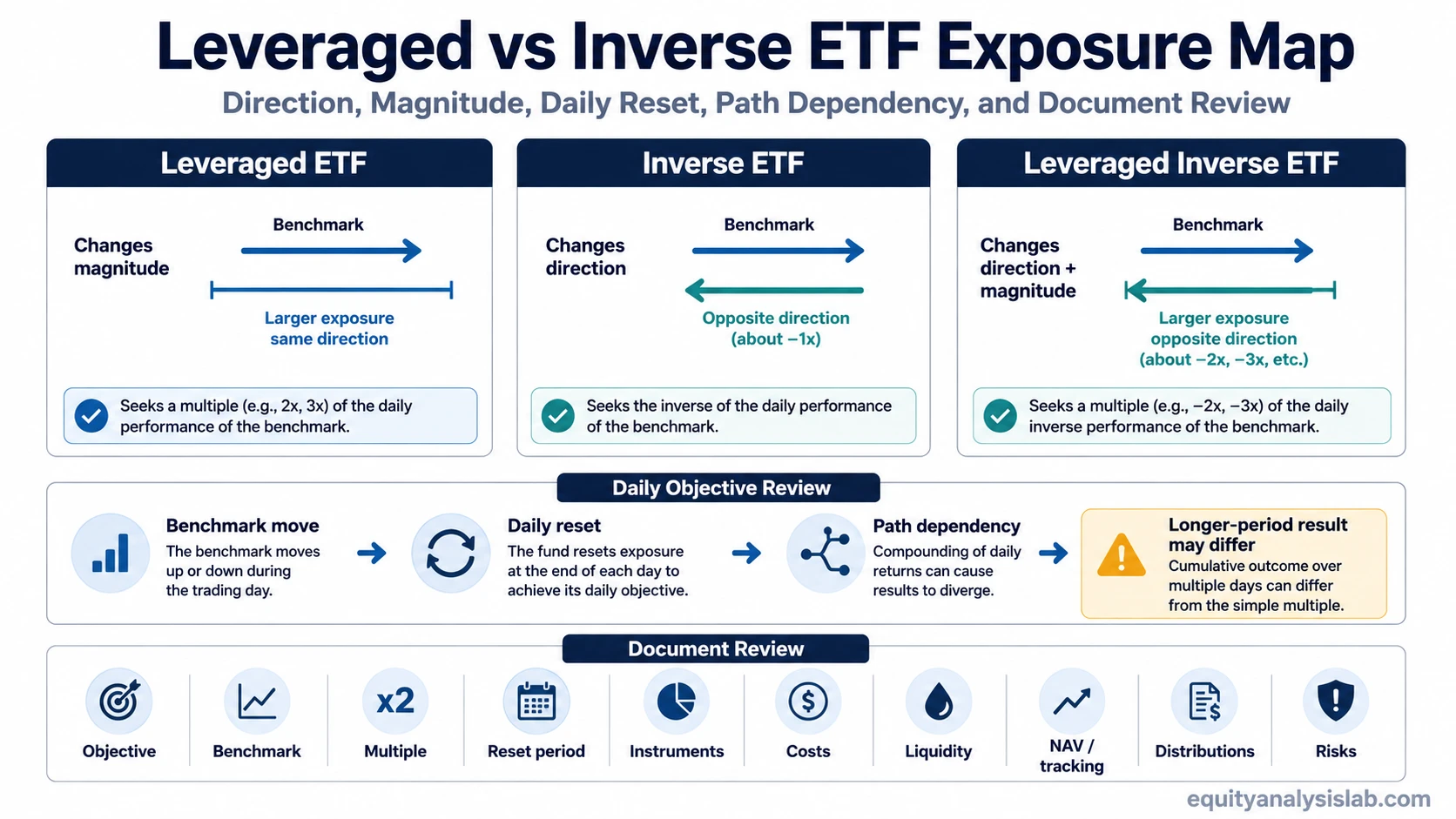

A leveraged ETF changes the size of benchmark exposure, usually by seeking a multiple of daily benchmark movement. An inverse ETF changes the direction of benchmark exposure, usually by seeking the opposite of daily benchmark movement.

The practical distinction is simple: leveraged asks “how much exposure?” while inverse asks “which direction?” A fund can be leveraged, inverse, both, or neither, so the label needs to be read against the stated objective, reset period, exposure method, costs, liquidity, and fund documents.

One-line distinction: leveraged exposure magnifies the benchmark move a fund seeks to track, while inverse exposure flips the direction of the benchmark move a fund seeks to track.

Key Points

- A leveraged fund usually seeks a multiple of a benchmark’s daily movement, such as exposure greater than one-to-one.

- An inverse fund usually seeks the opposite of a benchmark’s daily movement, so its objective moves against the benchmark direction.

- A leveraged inverse fund can seek a leveraged multiple of the opposite daily benchmark movement.

- Daily reset and compounding can make multi-day results differ from a simple multiple or inverse of the benchmark’s cumulative move.

- Fund documents control the actual objective, reset period, instruments, costs, risks, and exposure method.

Leveraged vs Inverse ETF: The Core Difference

The comparison starts with two separate questions. A leveraged ETF focuses on exposure size. It typically seeks a stated multiple of a benchmark’s daily performance, before fees, expenses, trading frictions, and tracking effects.

An inverse ETF focuses on exposure direction. It typically seeks performance that is opposite to a benchmark over the fund’s stated objective period, often one day unless the prospectus says otherwise.

| Comparison point | Leveraged ETF | Inverse ETF |

|---|---|---|

| Main question | How much benchmark exposure is targeted? | Which direction of benchmark exposure is targeted? |

| Typical objective | Seeks a multiple of daily benchmark movement. | Seeks the opposite of daily benchmark movement. |

| Direction | Usually same direction as the benchmark unless the fund is also inverse. | Opposite direction from the benchmark objective. |

| Exposure size | May target exposure greater than one-to-one. | May be one-to-one inverse or leveraged inverse, depending on the fund. |

| Common structure | Often uses derivatives or other instruments to pursue the stated multiple. | Often uses derivatives or short exposure mechanics to pursue opposite exposure. |

| Main confusion | Investors may assume the stated multiple applies cleanly over long periods. | Investors may assume inverse exposure is always unleveraged. |

| Document check | Read the objective, reset period, benchmark, instruments, risks, and fees. | Read the objective, reset period, benchmark, instruments, risks, and fees. |

The two ideas are related but not interchangeable. A fund can magnify exposure without reversing it, reverse exposure without magnifying it, or combine both features in a leveraged inverse structure.

How Daily Reset Changes the Comparison

Many leveraged and inverse ETFs are built around a daily objective. That means the fund’s target exposure is usually measured against one day of benchmark movement, not against the benchmark’s cumulative movement across a week, month, or year.

Daily reset matters because compounding changes the path. If a benchmark rises and falls across several sessions, the fund’s multi-day result can diverge from the simple arithmetic result a reader might expect from multiplying the benchmark’s total move by the stated exposure target.

Important limitation: a daily objective does not guarantee that a fund will deliver the stated multiple or opposite return over longer holding periods. Volatility, compounding, fees, spreads, tracking behavior, and the benchmark path can all change the realized result.

This is why the reset period belongs near the top of the review. If the fund’s documents define a daily target, the fund should not be interpreted as a simple long-term multiple of the benchmark unless the documents support that interpretation.

Same Benchmark, Different Exposure Objective

Consider a benchmark that moves up on one day and down on another. A standard benchmark ETF may seek one-to-one exposure. A leveraged fund may seek a multiple of that same benchmark’s daily move. An inverse fund may seek the opposite daily move. A leveraged inverse fund may seek a multiple of the opposite daily move.

Illustrative scenario: a benchmark gains during the first session, then gives back part of the move during the next session. The leveraged version is not only larger; it is exposed to the sequence of daily benchmark changes. The inverse version is not only bearish; it is designed around opposite daily exposure. The leveraged inverse version combines both features, so both direction and magnitude need to be checked.

| Fund objective type | What changes | What the investor must check |

|---|---|---|

| Standard benchmark exposure | Usually seeks one-to-one benchmark exposure. | Benchmark, holdings, costs, liquidity, and tracking behavior. |

| Leveraged exposure | Changes the size of benchmark exposure. | Stated multiple, reset period, instruments, fees, and compounding risk. |

| Inverse exposure | Changes the direction of benchmark exposure. | Opposite exposure target, reset period, tracking behavior, and volatility effects. |

| Leveraged inverse exposure | Changes both direction and size. | Opposite multiple, daily objective, path dependency, costs, and liquidity. |

The same benchmark can produce different investor experiences depending on whether the fund changes exposure size, exposure direction, or both. The benchmark name alone is not enough to define what the investor is actually holding.

Can an ETF Be Both Leveraged and Inverse?

Yes. Leveraged and inverse are not mutually exclusive labels. A fund can seek opposite exposure and also seek more than one-to-one exposure to that opposite daily move. That structure is often described as leveraged inverse exposure.

Confusion trap: “inverse” does not automatically mean unleveraged, and “leveraged” does not automatically mean same-direction exposure. The fund objective must answer both questions: direction and magnitude.

| Label combination | Direction question | Magnitude question |

|---|---|---|

| Neither leveraged nor inverse | Usually same direction as benchmark. | Usually one-to-one exposure objective. |

| Leveraged but not inverse | Usually same direction as benchmark. | Exposure multiple is greater than one-to-one. |

| Inverse but not leveraged | Opposite direction from benchmark. | May seek one-to-one opposite exposure. |

| Leveraged and inverse | Opposite direction from benchmark. | May seek a multiple of opposite exposure. |

The distinction matters because a fund label can compress several mechanics into one phrase. Direction, magnitude, reset period, and fund-document review need to be separated before the exposure can be understood clearly.

Exposure Mechanics Behind the Label

The exposure label describes the target, not the full mechanics. Leveraged and inverse funds may use swaps, futures, options, short exposure methods, cash instruments, or other derivatives and portfolio techniques, depending on the fund. The exact mix is controlled by the prospectus and related fund documents.

Two funds can reference similar markets while using different exposure engines. One may emphasize swaps. Another may use futures. Another may combine instruments. The important review is not whether derivatives appear in the abstract, but how the fund defines its benchmark, exposure target, reset period, counterparty or instrument risk, costs, and tracking process.

ETN note: some search results discuss ETFs and ETNs together. An ETN is a different wrapper with issuer credit considerations. The ETF comparison should not assume that every leveraged or inverse exchange-traded product has the same legal structure.

Costs, Liquidity, Tracking, and Fund Documents

The difference between leveraged and inverse exposure is only the first layer. The investor experience can also be shaped by expense ratios, financing costs embedded in the strategy, bid-ask spreads, trading volume, market depth, premium or discount to NAV, tracking difference, benchmark volatility, and distribution mechanics where relevant.

| Review factor | Why it matters | What to check |

|---|---|---|

| Fund objective | Defines whether exposure is leveraged, inverse, both, or neither. | Benchmark, direction, multiple, and stated objective period. |

| Reset period | Controls how the target exposure is measured. | Daily, monthly, or another period stated in the documents. |

| Compounding | Can make longer-period results differ from a simple multiple or inverse. | Benchmark path, volatility, and holding-period sensitivity. |

| Costs | Fees and strategy costs can reduce realized performance. | Expense ratio, financing costs, and transaction-related costs where disclosed. |

| Liquidity and spreads | Trading costs can change the price an investor actually receives. | Bid-ask spread, average volume, market depth, and order execution conditions. |

| NAV and market price | ETF shares trade in the market and may differ from NAV. | Premiums, discounts, creation/redemption conditions, and intraday behavior. |

| Tracking behavior | The fund may not perfectly match the stated objective after costs and frictions. | Tracking difference, benchmark methodology, and disclosed risk factors. |

These factors matter because the visible label can be too compressed. “Leveraged,” “inverse,” or “leveraged inverse” identifies the exposure target, but the fund documents explain how that target is pursued and what can cause actual results to differ.

Fund-Document Checklist

The fund documents are the controlling source for the exact exposure design. A short checklist keeps the review focused without turning the comparison into product ranking or personalized suitability advice.

- Objective: Does the fund seek same-direction, inverse, leveraged, or leveraged inverse exposure?

- Benchmark: Which index, asset, basket, sector, commodity, currency, or other reference exposure is used?

- Multiple: Is the target one-to-one, greater than one-to-one, opposite one-to-one, or opposite leveraged exposure?

- Reset period: Is the objective daily or based on another period?

- Exposure method: Which instruments may be used, such as swaps, futures, options, or other derivatives?

- Risk factors: What does the prospectus say about compounding, volatility, tracking difference, liquidity, and market-price behavior?

- Costs: What expenses, spreads, financing costs, or transaction effects can affect realized results?

- Distributions: Are distributions relevant to the fund structure, and how are they described?

This checklist does not decide whether a fund is appropriate for a specific investor. It narrows the review to the exposure mechanics that define what the fund is trying to do.

Common Mistakes When Comparing Leveraged and Inverse ETFs

- Mistake 1: Treating leveraged and inverse as the same thing. Leveraged changes size. Inverse changes direction. Some funds combine both, but the labels are not identical.

- Mistake 2: Ignoring the reset period. A daily objective can produce longer-period results that differ from a simple cumulative benchmark multiple.

- Mistake 3: Assuming the benchmark name defines the whole exposure. The benchmark matters, but the objective, instruments, costs, liquidity, and tracking behavior also shape the outcome.

- Mistake 4: Reading inverse as automatically lower risk. Opposite exposure can still involve volatility, compounding effects, tracking difference, liquidity risk, and product-specific risks.

- Mistake 5: Using product labels as a substitute for fund documents. The prospectus and related documents define the actual objective and mechanics.

The clean comparison is direction first, magnitude second, reset period third, and fund-document details after that. Skipping any of those layers can make two very different products look more similar than they are.

FAQ

What is the main difference between a leveraged ETF and an inverse ETF?

A leveraged ETF usually seeks a multiple of a benchmark’s daily movement, while an inverse ETF usually seeks the opposite of a benchmark’s daily movement. Leveraged describes exposure size. Inverse describes exposure direction.

Can an ETF be both leveraged and inverse?

Yes. A leveraged inverse ETF can seek a leveraged multiple of the opposite daily movement of a benchmark. The fund objective and prospectus should be checked to confirm the exact direction, multiple, and reset period.

Does a daily leveraged or inverse objective apply over long periods?

Not automatically. If the objective is daily, results over longer periods can differ from a simple multiple or inverse of the benchmark’s cumulative movement because of compounding, volatility, fees, tracking behavior, and the path of returns.

Do all leveraged and inverse ETFs use the same instruments?

No. Funds may use swaps, futures, options, short exposure methods, cash instruments, or other techniques depending on the fund. The prospectus controls the specific exposure method and risk disclosures.

Is the ETF label enough to understand the exposure?

No. The label is only a starting point. The benchmark, objective, reset period, instruments, costs, liquidity, NAV and market price behavior, tracking risk, and fund documents all affect the exposure review.