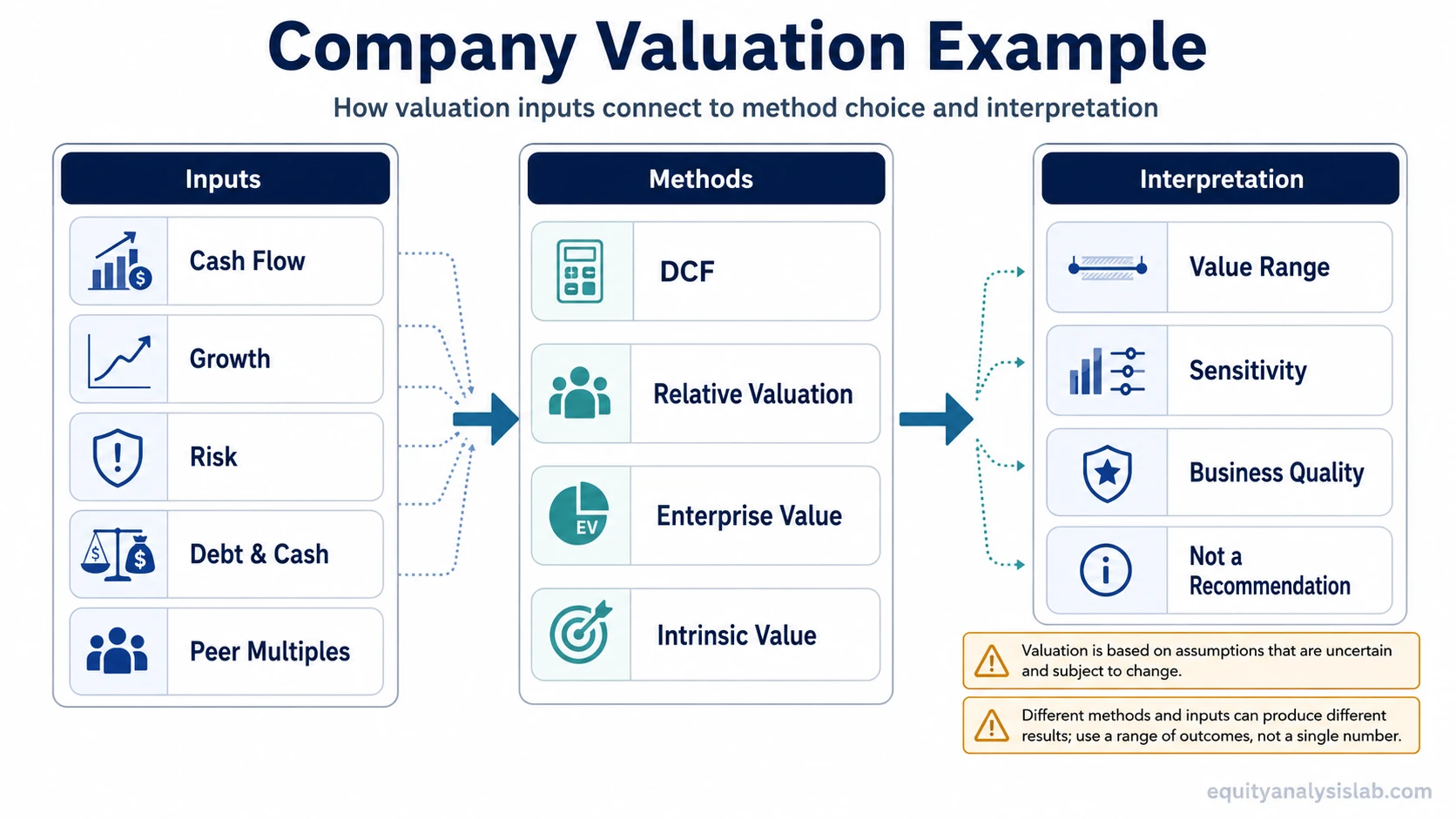

A company valuation example shows how an analyst turns cash flow, growth, risk, peer multiples, debt, and cash into an estimated company value. The useful part is not the final number by itself; it is seeing which inputs drive the result and when the conclusion becomes weaker.

Definition: A company valuation example is an educational model that shows how valuation inputs become an estimated company value. For a public-company investor, it is not sale advice, appraisal advice, a calculator output, or a stock recommendation. It is a structured way to examine value drivers and uncertainty.

Key Points

- A company valuation example converts inputs into an estimated value, not a guaranteed answer.

- Cash-flow-based examples focus on future cash flow, discount rate, and terminal value.

- Multiples-based examples compare a company with peers through valuation ratios.

- Capital structure matters because debt and cash can make operating value differ from equity value.

- The conclusion becomes weaker when the inputs are unsupported, overly precise, or disconnected from business quality.

What a Company Valuation Example Shows

A company valuation example connects business assumptions with estimated value. Instead of asking only whether a company looks cheap or expensive, it asks what must be true about revenue growth, margins, reinvestment, risk, peer comparison, debt, cash, and share count for the valuation to make sense.

The output is usually a value estimate or range. That range may be compared with market price, but the comparison is only one part of investor analysis. A valuation can look attractive and still be fragile if cash flow is uncertain, margins are cyclical, the balance sheet is stretched, or the peer group is poorly chosen.

The strongest valuation examples make the drivers visible. A precise-looking number can create false confidence when the model hides the inputs that produced it.

The Main Valuation Methods Used in Examples

Most company valuation examples use more than one method because each method emphasizes a different part of the business. One method may focus on internal cash-flow potential, while another may focus on how similar companies are priced in the market.

| Method bucket | What the example usually estimates | Main inputs | How it helps interpretation |

|---|---|---|---|

| Cash-flow valuation | Estimated value from future cash flows | Revenue, margins, reinvestment, discount rate, terminal value | Shows how future cash-flow assumptions, discount rate, and terminal value affect a discounted cash flow estimate. |

| Multiples valuation | Estimated value based on how comparable companies are priced | Peer group, revenue, earnings, EBITDA, growth, margins, risk | Shows how relative valuation depends on peer selection, growth, margins, and risk differences. |

| Capital-structure bridge | How operating value connects to equity value | Debt, cash, minority interests, preferred claims, share count | Shows why enterprise value can differ from the value left for common equity holders. |

| Investor value estimate | A reasoned estimate of what the business may be worth under stated assumptions | Cash-flow durability, risk, growth, capital allocation, uncertainty | Shows how intrinsic value can differ from market price while still depending on assumptions. |

A broad company valuation example should show how the methods differ and why they can produce different estimates. Full method detail belongs in the specific valuation method being analyzed.

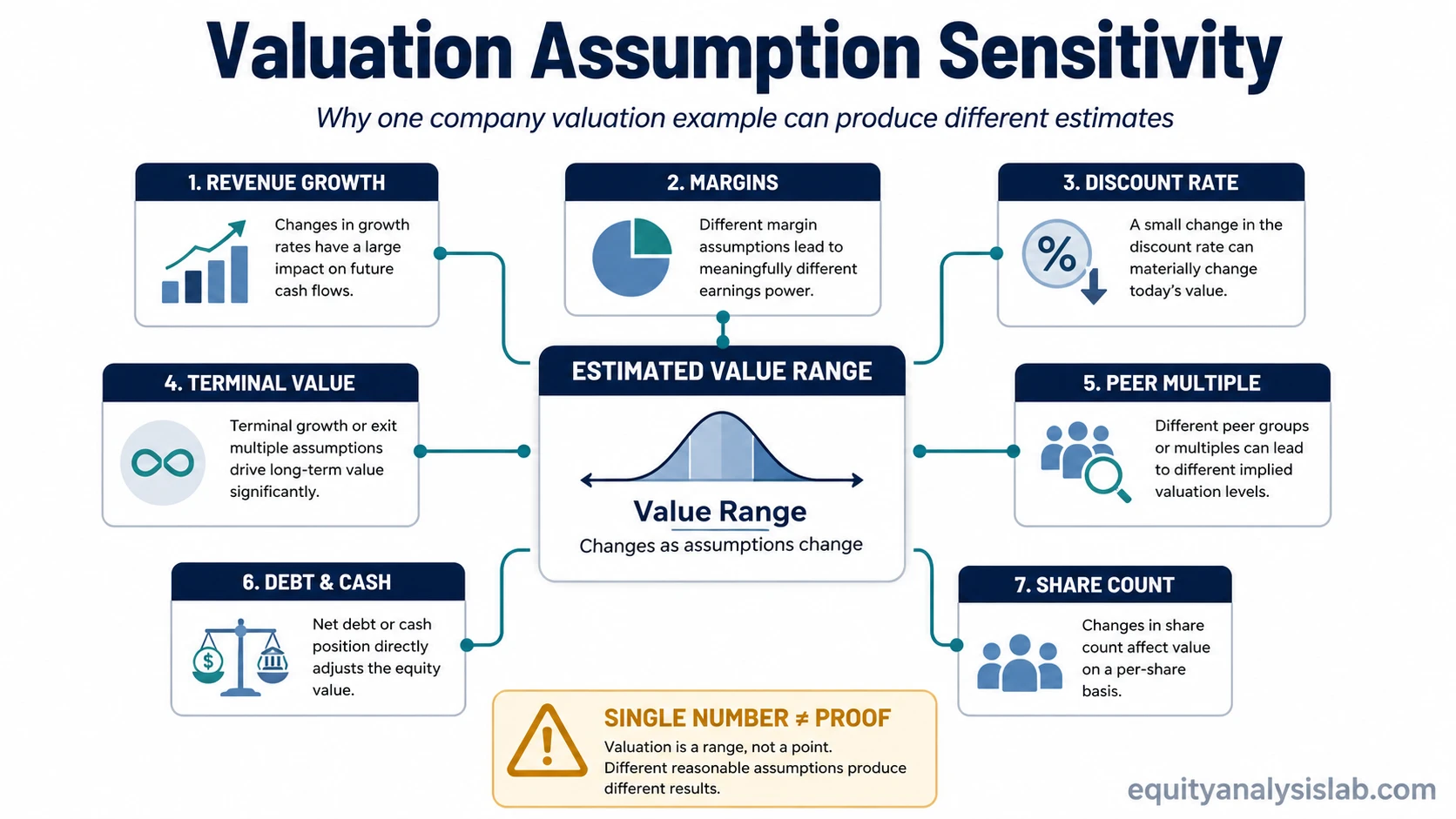

How Assumptions Change the Valuation Result

The same company can produce different valuation estimates when the inputs change. That does not make valuation useless. It means the result should be read as a sensitivity exercise, not as a fixed truth.

| Assumption | What it changes | Why it can weaken the estimate |

|---|---|---|

| Revenue growth | Future cash-flow base | Growth may slow, require more capital, or depend on a market that is less durable than the model assumes. |

| Margins | Profit and cash-flow conversion | Margins may not hold if costs, competition, pricing power, or product mix change. |

| Discount rate | Present value of future cash flows | Small changes can move long-duration estimates materially, especially when much of the value sits far in the future. |

| Terminal value | Long-term value beyond the forecast period | Long-range assumptions can dominate the output even when near-term forecasts look reasonable. |

| Peer multiple | Relative valuation estimate | The peer group may not match the company’s growth, margins, risk, capital intensity, or business quality. |

| Debt and cash | Enterprise-to-equity value bridge | Capital structure can make equity value differ from operating value, especially for companies with material debt or cash balances. |

| Share count | Per-share value | Dilution or repurchases can change the per-share conclusion even when the business-level estimate is unchanged. |

A strong valuation example does not hide sensitivity. It shows which inputs matter most and where the valuation would break if those inputs are wrong.

A Simple Company Valuation Example

Illustrative example: Imagine a public company with steady revenue, improving margins, moderate debt, and a peer group that trades at different multiples. Under a conservative cash-flow forecast, the company may look fairly valued. Under a more optimistic margin scenario, the same company may look undervalued. Against a lower-risk peer group, it may look expensive.

For example, the optimistic case may depend mostly on margin expansion, while the lower-risk peer comparison may penalize the company for higher leverage or less durable cash flow.

The lesson is not that one answer is automatically correct. The useful question is which scenario is most defensible, which inputs are most uncertain, and whether the business quality supports the valuation range.

This is why method, assumptions, and sensitivity should be read together. A final estimate without the inputs behind it is hard to interpret.

Common Mistakes When Reading Valuation Examples

Valuation examples are easy to misread when the model output looks more precise than it really is. The main risk is not that a model uses assumptions. The main risk is forgetting that assumptions are the model.

| Mistake | Why it is a problem | Better interpretation |

|---|---|---|

| Treating one estimate as the true value | A single number can hide a wide range of possible outcomes. | Read the estimate as one scenario inside a valuation range. |

| Ignoring business quality | Similar earnings can deserve different valuations if durability, reinvestment needs, or competitive position differ. | Connect the valuation to cash-flow quality, margins, and business risk. |

| Copying peer multiples mechanically | A peer group can be misleading if the companies differ in growth, margins, leverage, or cyclicality. | Use peers as context, not as automatic proof of value. |

| Overweighting terminal value | Long-term assumptions may dominate the estimate even though they are the least certain part of the model. | Check whether the conclusion still holds under more conservative terminal assumptions. |

| Forgetting debt, cash, and share count | Operating value and per-share equity value can differ materially after capital structure adjustments. | Separate business value, equity value, and per-share value before drawing conclusions. |

| Reading valuation as a decision by itself | A valuation estimate does not resolve risk, timing, portfolio fit, or uncertainty. | Use valuation as one input in a broader investor decision process. |

Which Valuation Question Are You Trying to Answer?

Once the broad example is clear, the next question depends on which part of the estimate is still unclear: cash flows, peer multiples, capital structure, or the gap between estimated value and market price.

| Reader question | Best next concept | Why it helps |

|---|---|---|

| How do future cash flows become today’s value? | Discounted cash flow | It explains the cash-flow forecast, discount rate, and terminal value logic behind many valuation examples. |

| How do peer multiples shape the estimate? | Relative valuation | It explains how investors compare companies using valuation multiples and why peer selection matters. |

| Why do debt and cash change the conclusion? | Enterprise value | It separates the value of the operating business from the value left for common equity holders. |

| How is estimated value different from market price? | Intrinsic value | It explains why an investor’s estimate can differ from the current market price while still depending on assumptions. |

The useful next step is to isolate the part of the valuation that changes the conclusion most.

What a Company Valuation Example Cannot Prove

A company valuation example cannot prove that a stock is mispriced, safe, or attractive. It cannot guarantee that a market price will move toward an estimate. It also cannot remove uncertainty from business quality, competition, capital allocation, interest rates, or future cash-flow durability.

What it can do is make the valuation argument easier to inspect. If the estimate only works under aggressive growth, stable margins, a generous terminal value, or a weak peer comparison, the example reveals that fragility. If the estimate remains reasonable under several disciplined assumptions, the investor has a stronger basis for further analysis.

The strongest use of a company valuation example is not to find a single perfect number. It is to understand the assumptions behind the number, test how sensitive the conclusion is, and decide which valuation method needs deeper work.