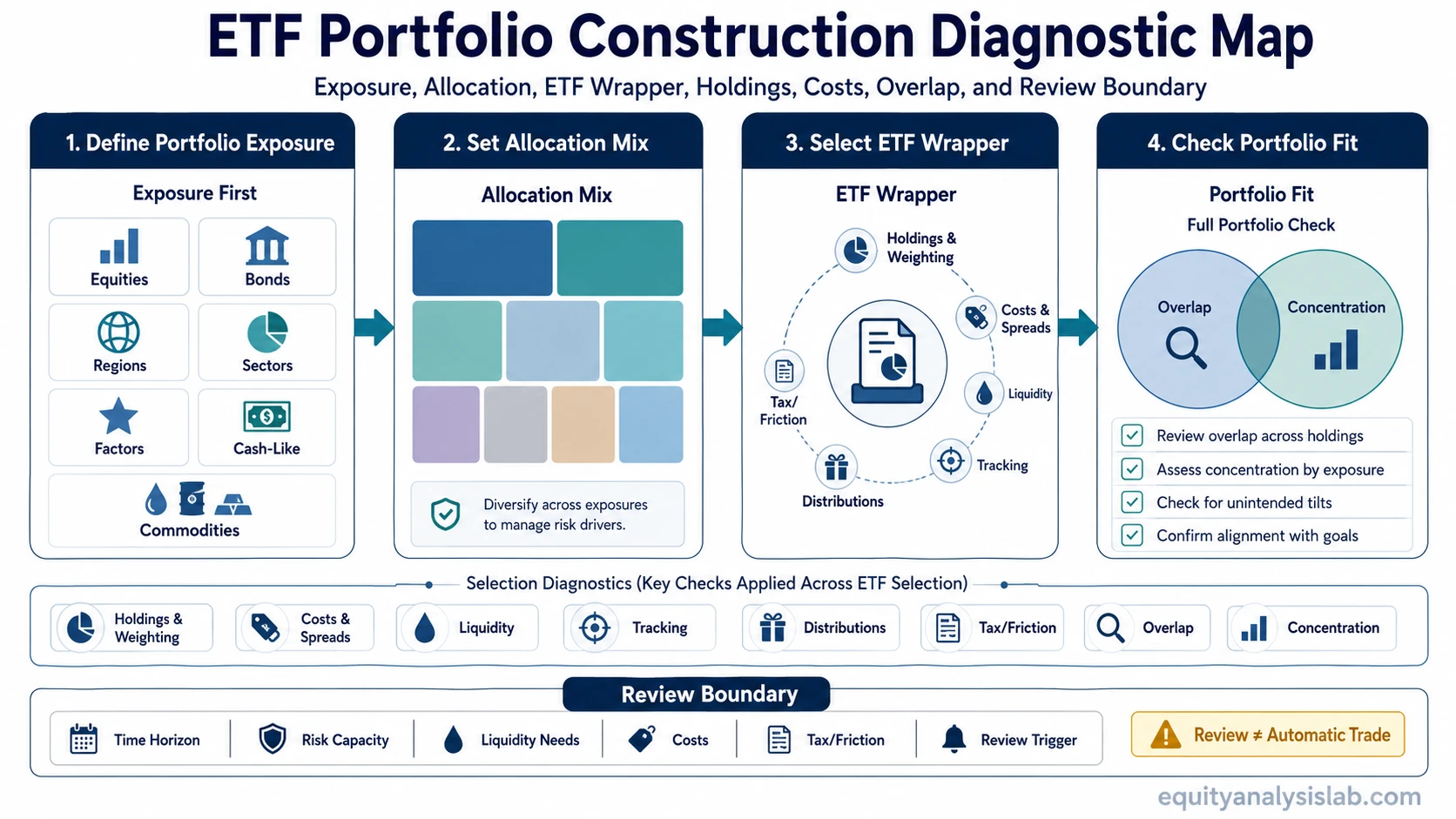

Building an ETF portfolio means defining the portfolio exposure first, then choosing ETF wrappers that match the desired allocation, holdings, costs, liquidity, tax/friction profile, and review rules. The fund label is only the starting point. The real portfolio is shaped by what the ETFs own, how those holdings are weighted, how much the structure costs to hold or trade, and how the mix will be reviewed later.

An ETF portfolio can be simple or complex, but the construction logic should stay the same: decide what the portfolio needs to own, then test whether each ETF actually delivers that exposure without hidden duplication, unnecessary friction, or a review problem that appears only after the portfolio is already built.

Key Points

- Exposure comes before ETF selection. The first decision is what the portfolio should represent, not which fund looks attractive.

- An ETF name does not define the actual portfolio exposure. Holdings, weighting, index method, distributions, and tracking behavior can change the result.

- Costs include more than the expense ratio. Spreads, liquidity, tax/friction, and trading behavior can also affect the investor’s experience.

- Several ETFs can still create concentration if they hold the same companies, sectors, countries, factors, or index family.

- Review rules matter because ETF portfolio construction is not a one-time fund-picking exercise.

How to Build an ETF Portfolio Starts With Exposure

To build an ETF portfolio, start by defining the exposure the portfolio needs: equities, bonds, regions, sectors, factors, cash-like holdings, commodities, or other asset classes where relevant. Only after that exposure map is clear does ETF selection become useful.

This order prevents a common mistake. A fund can sound diversified because it has a broad name, but the portfolio may still depend heavily on a small number of holdings, one region, one sector, or one market-cap segment. The construction question is not “which ETF is popular?” It is “what exposure is being added, and what does it change inside the full portfolio?”

A provider-neutral ETF portfolio framework separates three layers: the desired exposure, the ETF wrapper used to deliver that exposure, and the portfolio-level result after the fund is combined with everything else already owned.

Define Allocation Before Selecting ETFs

Allocation comes before fund choice because ETF selection should serve the portfolio structure. A reader building an ETF portfolio needs to decide how much weight belongs to broad equity exposure, defensive assets, regional exposure, sector tilts, income-oriented holdings, or other categories before comparing individual funds.

The allocation mix should reflect the portfolio’s purpose, time horizon, risk capacity, and need for liquidity. That does not mean the same percentage mix works for every investor. It means the ETF list should not be allowed to create the allocation by accident.

For example, an investor may think the portfolio is balanced because it owns five ETFs. If three of them are broad equity ETFs with similar top holdings, the real allocation may be more concentrated than the fund count suggests. The number of ETFs is less important than the exposure each ETF adds or duplicates.

Choose ETF Wrappers After You Know the Exposure

Once the desired exposure is clear, the next step is to decide which ETF wrapper best represents it. A broad market ETF, sector ETF, bond ETF, dividend ETF, factor ETF, commodity-linked ETF, or active ETF may behave differently even when the name sounds similar to another fund category.

An index ETF structure usually tracks a stated benchmark, but the benchmark rules still matter. Market-cap weighting, equal weighting, factor screening, sector classification, country classification, reconstitution schedules, and concentration limits can all affect the exposure an ETF delivers.

The practical check is simple: do not stop at the fund label. Review the holdings, weighting method, benchmark or strategy, distribution behavior, and role in the full portfolio. A broad-name ETF can still be concentrated. A niche ETF can add useful exposure or unnecessary complexity depending on what is already owned.

Check Costs, Holdings, and Tracking Before You Add a Fund

The expense ratio is an important cost input, but it is not the full cost picture. A low annual fee does not automatically make an ETF the better portfolio choice if the fund has weak liquidity, wider spreads, unwanted overlap, poor fit with the intended exposure, or tax/friction issues that matter for the account type.

Holdings and weighting are usually the first place to look. Two ETFs can both describe themselves as broad equity funds, but one may be market-cap weighted with heavy concentration in large companies while another may use a different weighting or screening method. The difference can change the portfolio’s risk exposure even when both funds appear to belong to the same broad category.

Tracking behavior also matters. An ETF does not need to match its benchmark perfectly every moment, but persistent tracking differences, large spreads, thin liquidity, or unusual distribution behavior may change the investor’s experience. These checks are part of portfolio construction because they determine whether the ETF wrapper is an efficient way to hold the desired exposure.

What to Check Before Adding an ETF

| Portfolio check | Question to ask | Why it matters |

|---|---|---|

| Exposure | What asset class, region, sector, factor, or theme is being added? | Prevents fund selection from driving the portfolio by accident. |

| Allocation | How much of the total portfolio should this exposure represent? | Keeps the fund list aligned with the intended portfolio structure. |

| Holdings | What does the ETF actually own? | Reveals concentration, overlap, and exposure that the fund name may hide. |

| Weighting method | How are the holdings weighted? | Changes the real influence of large holdings, sectors, countries, or factors. |

| Costs and spreads | What are the visible and trading-related costs? | Expense ratio, bid-ask spread, liquidity, and trading friction can all matter. |

| Tracking | How closely does the ETF deliver the intended exposure? | Benchmark, strategy, and tracking differences can alter portfolio behavior. |

| Tax/friction | Does the structure create account-specific friction? | Distributions, turnover, and account type may affect the holding experience. |

| Overlap | Does this ETF repeat what the portfolio already owns? | Multiple funds can still create hidden concentration. |

| Review rule | When should this ETF or allocation be reviewed? | Prevents the portfolio from becoming unmanaged after the initial build. |

Review Overlap, Concentration, and Portfolio Fit

ETF portfolio construction should be checked at the portfolio level, not only fund by fund. A single ETF may look reasonable on its own while still adding little new exposure because the portfolio already owns similar companies, sectors, countries, or factors through other funds.

Overlap is not always bad. A broad equity ETF and a sector ETF may intentionally overlap if the investor wants that sector to carry more weight. The risk appears when overlap is accidental and the portfolio becomes more concentrated than the investor realizes.

Concentration can come from several places: repeated top holdings, similar index families, overlapping regional exposure, sector-heavy funds, factor screens that select the same kinds of companies, or bond funds with similar duration and credit exposure. The review should ask what the combined portfolio owns after all funds are added.

Generic ETF Selection Scenario

Suppose an investor wants a simple ETF portfolio with broad equity exposure and a defensive allocation. The first step is not to search for the most popular ETF. The first step is to define the exposure mix: how much should be broad equity, how much should be defensive, and whether any regional, sector, factor, income, or cash-like exposure is needed.

After that, the investor can compare ETF wrappers against the desired role. A broad equity ETF may fit the core equity role if its holdings and weighting match the intended exposure. A bond ETF may fit the defensive role if its duration, credit exposure, liquidity, and distribution behavior match the portfolio’s purpose. A sector or factor ETF may be unnecessary if it mostly repeats what the broad equity fund already owns.

The useful decision is not whether one ETF is “better” in isolation. It is whether each ETF improves the full portfolio after costs, overlap, concentration, tax/friction, and review rules are considered.

Set Review Rules Before Rebalancing Becomes Necessary

An ETF portfolio needs review rules because weights, market values, costs, fund structures, tax/friction, and investor objectives can change over time. Review rules define when the portfolio should be checked, not when a trade must automatically happen.

A review may be triggered by large allocation drift, new overlap, changes in liquidity needs, a change in time horizon, a fund methodology change, tax/friction considerations, or a shift in the original portfolio objective. The rebalancing decision comes only after the review shows that the current weights no longer fit the intended portfolio structure.

This boundary matters because portfolio maintenance is not the same as constant activity. A disciplined ETF portfolio can be reviewed without forcing unnecessary trades, especially when the current mix remains aligned with the investor’s exposure map and risk capacity.

When the ETF Portfolio Framework Breaks Down

The framework breaks down when fund selection replaces portfolio design. That can happen when the investor starts with fund rankings, recent performance, provider marketing, low expense ratios, or thematic labels before defining the portfolio’s desired exposure and allocation.

It also breaks down when ETF count is confused with diversification. Ten ETFs can still create a concentrated portfolio if they hold the same large companies or repeat the same sector, factor, region, duration, or credit exposure. A smaller number of ETFs can be more diversified if the underlying holdings and weights are genuinely broad.

The safest interpretation is that ETF portfolio construction is a diagnostic process. It defines exposure, selects wrappers, checks holdings and costs, reviews overlap and concentration, and sets review rules. It does not require named ETF recommendations, model percentages, return forecasts, or automatic trading decisions.

FAQ

How many ETFs do I need in a diversified ETF portfolio?

There is no universal number. A small number of broad ETFs can create diversified exposure if the holdings, weights, and asset mix are truly broad. A larger number of ETFs can still be concentrated if they repeat the same companies, sectors, countries, or factors.

Is an ETF-only portfolio enough?

An ETF-only portfolio can be enough for some portfolio designs, but the answer depends on the desired exposure, account context, costs, liquidity needs, tax/friction, and review rules. The important question is not whether the portfolio uses only ETFs, but whether the ETFs create the intended exposure without hidden duplication.

How do I build an index ETF portfolio?

To build an index ETF portfolio, define the target allocation first, then choose index ETFs whose benchmarks, holdings, weighting methods, costs, liquidity, and overlap match that allocation. The index label should be checked against the fund’s actual holdings and methodology.

Why is low expense ratio not enough to choose an ETF?

A low expense ratio can be useful, but it does not capture the whole decision. Holdings, weighting, spreads, liquidity, tracking behavior, distributions, tax/friction, and overlap with the rest of the portfolio can all affect whether an ETF fits the portfolio.

When should an ETF portfolio be reviewed?

An ETF portfolio should be reviewed when weights, overlap, concentration, time horizon, liquidity needs, costs, tax/friction, or the investor’s original objective have changed enough to question the current mix. A review does not automatically mean a trade is required.