A discount rate is the rate used to convert future cash flows into present value.

Weighted average cost of capital, or WACC, is one possible estimate for that rate when the valuation is built around company-wide, unlevered cash flows and the company’s capital structure is a reasonable match for the risk being valued.

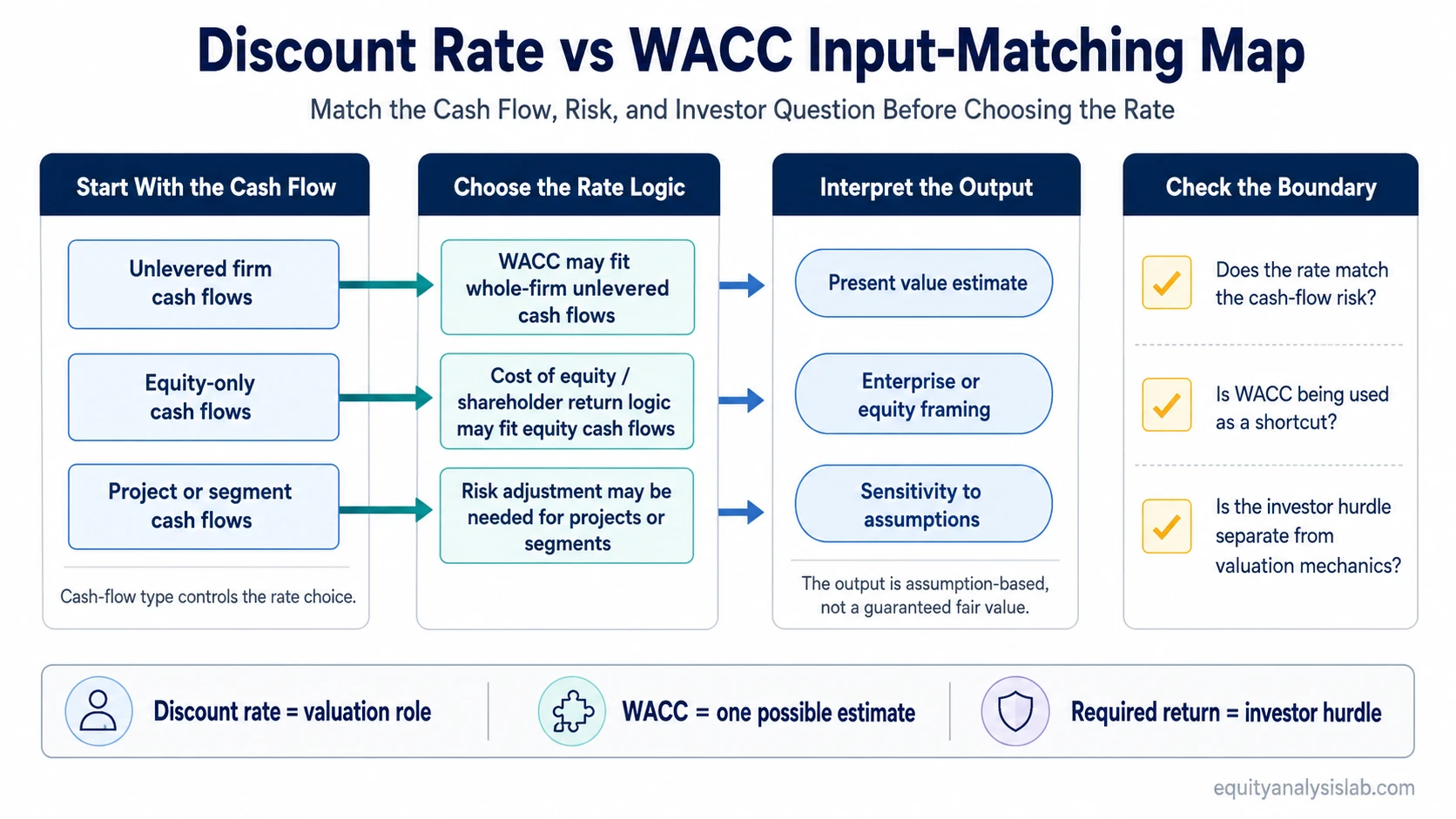

Discount rate describes the role inside the valuation model. WACC describes one way to estimate that role from the cost of debt, cost of equity, and capital structure. A valuation can use WACC as the discount rate, but WACC is not automatically the right discount rate for every cash flow, project, investor, or risk profile.

Discount Rate vs WACC: The Core Difference

- A discount rate is a valuation input. It turns expected future cash flows into present value.

- WACC is a company-level cost-of-capital estimate. It combines the cost of equity and after-tax cost of debt according to capital structure weights.

- WACC can be used as the discount rate when the cash flows and risk being valued match the whole firm.

- WACC can mislead when the cash flows are equity-only, project-specific, unusually risky, unusually stable, or disconnected from the company’s normal capital structure.

Discount Rate vs WACC Comparison Table

| Criteria | Discount rate | WACC |

|---|---|---|

| Core role | The rate used to discount future cash flows to present value. | A weighted estimate of the company’s blended cost of capital. |

| Category | Valuation input. | Cost-of-capital estimate. |

| Best fit | Any valuation where the rate is chosen to match the cash-flow risk. | Enterprise valuation using unlevered free cash flow when firm-level risk is appropriate. |

| Source | May come from WACC, cost of equity, project risk, market assumptions, or an investor hurdle. | Derived from the cost of equity, after-tax cost of debt, and capital structure weights. |

| Cash-flow match | Must match the cash flow being valued. | Usually matches unlevered cash flows to the firm, not equity-only cash flows by default. |

| Main risk | Choosing a rate that does not reflect the cash-flow risk. | Treating a company-wide average as correct for every project, segment, or investor objective. |

When WACC Can Be Used as the Discount Rate

WACC is most defensible as the discount rate when the valuation is estimating the value of the whole operating business. In that case, the cash flows are usually unlevered free cash flows, meaning they are available to both debt and equity providers before financing flows. The resulting valuation typically points toward enterprise value rather than equity value alone.

This is why WACC is common in discounted cash flow models for established companies with relatively stable financing structures. The analyst is not valuing only the common equity cash flows. The analyst is valuing operating cash flows before financing decisions, so a blended capital-cost estimate can be a reasonable match.

The match still depends on assumptions. If the business has changing leverage, unusual financing risk, major segment differences, or a project with a risk profile far away from the existing company, the company-wide WACC may become a weak shortcut rather than a clean discount-rate estimate.

When WACC Is Not the Right Discount Rate

WACC is not automatically appropriate when the cash flow being valued belongs to a narrower or different risk category than the whole firm. A high-risk new project, a regulated low-risk asset, a foreign segment, or a business line with different operating cyclicality may require a project-specific adjustment.

WACC is also not the default rate for equity cash flows. If the model discounts cash flows available only to common shareholders, the discount rate should usually reflect the cost of equity or a shareholder-required return logic, not the company’s blended debt-and-equity capital cost.

A separate issue appears when investors use a personal hurdle rate. A required return can help an investor decide whether an opportunity clears their own threshold, but it does not become “the correct valuation discount rate” simply because the investor wants that return. The cash-flow risk, valuation purpose, and comparison set still matter.

Same Cash Flow, Different Discount-Rate Assumptions

Consider a hypothetical company expected to produce the same operating cash-flow forecast under three different valuation assumptions. The cash-flow forecast does not change. Only the discount-rate logic changes.

| Assumption path | Discount-rate logic | What it is trying to answer | Main caution |

|---|---|---|---|

| Company-wide WACC | Use the firm’s blended cost of capital. | What are the operating cash flows worth under a whole-company capital-cost estimate? | Works only if the cash flows resemble the firm’s normal risk and capital structure. |

| Project-specific adjustment | Add a risk premium or use a different rate for a riskier segment. | What are the same cash flows worth if their risk is above the company average? | The premium must be justified by risk, not added mechanically. |

| Investor hurdle comparison | Compare the valuation output against the investor’s own required return threshold. | Does the opportunity clear the investor’s hurdle after valuation assumptions are reviewed? | A personal hurdle does not prove fair value or replace cash-flow risk analysis. |

The useful lesson is that the discount rate is an assumption bridge between cash flows and present value. WACC can supply that bridge in the right setting, but the bridge changes when the risk, cash-flow type, or investor question changes.

WACC, Required Return, and Project Risk

The most common confusion is treating WACC, discount rate, and required return as interchangeable labels. They can overlap, but they answer different questions. WACC asks what the company’s capital providers require on a weighted basis. A discount rate asks what rate should convert a specific cash-flow stream into present value. A required return hurdle asks what return threshold an investor or capital allocator wants before accepting the risk.

Those three ideas can point to the same number in a simple model. They can also diverge. A mature company’s base operating cash flows may fit WACC. A speculative expansion project may require a higher discount rate. A conservative investor may require an even higher hurdle before considering the valuation attractive enough for their own process.

The cleaner workflow is to identify the cash flow first, then match the rate. Unlevered firm cash flows usually point toward WACC. Equity cash flows point toward equity return logic. Project-specific cash flows may need their own risk adjustment. Investor hurdle rates belong in the interpretation layer, not as an automatic replacement for risk-matched valuation work.

Common Mistakes When Comparing Discount Rate and WACC

- Treating WACC as universal: WACC is a useful estimate, not a universal valuation rate for every asset, project, or cash-flow stream.

- Ignoring cash-flow type: The discount rate should match whether the model uses unlevered firm cash flows, equity cash flows, or project-specific cash flows.

- Using a hurdle rate as proof: An investor’s required return can shape decision discipline, but it does not prove that a valuation is objectively right.

- Forgetting sensitivity: Small changes in discount-rate assumptions can materially change present value, especially for long-duration cash flows.

- Turning valuation into certainty: A DCF output is an assumption-based estimate, not a guaranteed fair value or investment recommendation.

Discount Rate and WACC Limitations

WACC is an estimate built from market inputs, capital structure assumptions, tax assumptions, and cost-of-equity estimates. Each part can change. That makes WACC useful, but not precise in the way a fixed contractual rate is precise.

The discount rate also does more than perform a calculation. It carries a judgment about risk. If the rate is too low for the cash-flow risk, present value may look too high. If the rate is too high, the same forecast may look too conservative. The valuation result is only as reliable as the cash-flow forecast and discount-rate match behind it.

For that reason, the strongest use of discount rate vs WACC is not choosing one label and applying it everywhere. The stronger use is checking whether the chosen rate fits the cash flows, capital structure, business risk, and investor question being analyzed.

FAQ

Is WACC the same as the discount rate?

No. WACC can be used as a discount rate in the right valuation context, but it is not a synonym. Discount rate is the role in the valuation model. WACC is one possible estimate for that role.

Why is WACC often used as the discount rate?

WACC is often used when valuing a company’s unlevered free cash flows because those cash flows belong to both debt and equity providers. A blended cost-of-capital estimate can match that whole-firm framing.

When should WACC not be used as the discount rate?

WACC may be a poor fit when the cash flows are equity-only, project-specific, unusually risky, unusually stable, or based on a capital structure that differs from the company’s current or expected financing mix.

Is required return the same as WACC?

Not necessarily. Required return may reflect an investor’s hurdle or the return demanded for a specific risk. WACC reflects a company’s blended capital cost. The two can overlap, but they answer different questions.