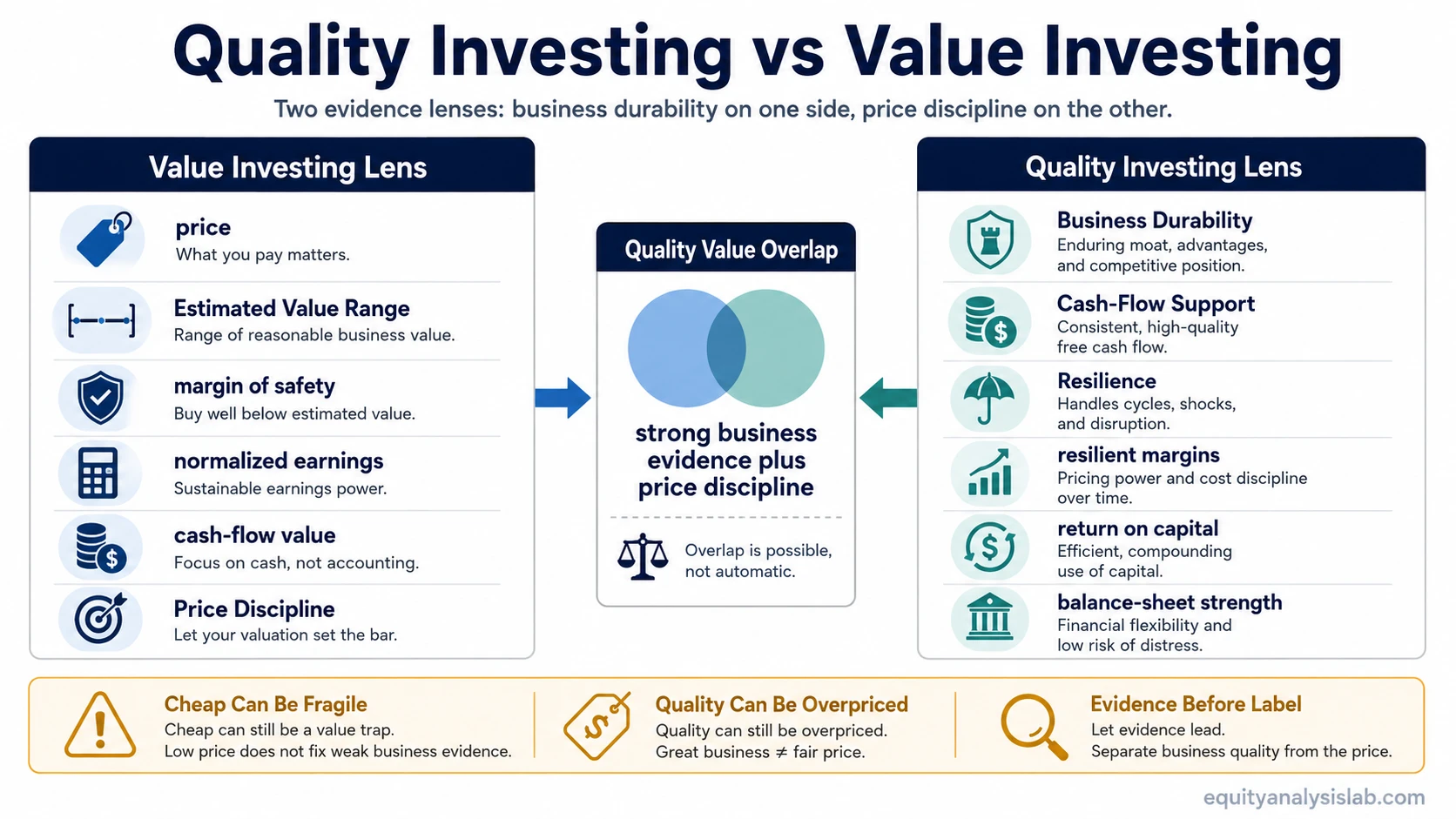

Quality investing and value investing both use fundamentals, but they ask different questions. Value investing asks whether the price is low enough relative to estimated business value. Quality investing asks whether the business is durable enough, cash-supported, and resilient enough to support deeper review even when the valuation is not obviously cheap.

The confusion appears because a strong business can also be undervalued, and a cheap stock can sometimes belong to a durable company. The two lenses can overlap, but they are not interchangeable. One starts with price discipline. The other starts with business durability. A complete investment view often needs both checks, but each check can reject a company for a different reason.

Key Points

- Value investing starts with price versus estimated business value.

- Quality investing starts with durability, cash-flow support, resilience, and business economics.

- A cheap stock can still be a value trap if the business evidence is weak.

- A high-quality company can still offer poor value if expectations already price in too much strength.

- Quality value combines the lenses, but the two tests still ask different questions.

The Core Difference

The value test begins with market price and a reasonable estimate of business value. That estimate may use normalized earnings, free cash flow, assets, comparable multiples, or a valuation range. The central discipline is price: a business can be interesting, but the value case weakens when the price leaves little room for error.

The quality test begins with whether the business has enough durability to make its earnings and cash flows meaningful. That durability may come from strong margins, recurring demand, pricing power, return on invested capital, balance-sheet resilience, or consistent cash conversion. The central discipline is evidence quality: a low price is less useful when the underlying business cannot support the valuation case.

Working distinction: Value investing judges the gap between price and estimated value. Quality investing judges whether the business deserves confidence in its economics, cash generation, and resilience.

Quality vs Value Comparison Table

| Criterion | Value investing lens | Quality investing lens |

|---|---|---|

| Main question | Is the price low enough relative to estimated business value? | Is the business durable enough to support deeper review or a premium valuation? |

| Evidence focus | Valuation range, intrinsic value estimate, normalized earnings, margin of safety, asset value, or cash-flow value. | Cash flow, margins, returns on capital, debt resilience, reinvestment quality, competitive position, and durability. |

| Role of valuation | Valuation is the starting filter. The price must create enough discount against estimated value. | Valuation is a restraint. Quality does not remove the need to check price and expectations. |

| Role of business quality | Business quality improves the value case when it makes estimated value more durable. | Business quality is the first screen, but it must be supported by financial evidence rather than labels. |

| Main risk | The stock is cheap for a reason, and the low valuation reflects deteriorating economics. | The company is strong, but the price already assumes too much future success. |

| Failure mode | Value trap. | Quality at any price. |

| Overlap | Quality can strengthen value evidence by making estimated value less fragile. | Valuation still matters because business strength can be overcapitalized into the price. |

| Useful context | Useful when price looks disconnected from conservative business value estimates. | Useful when business durability, cash generation, and resilience need to be tested before valuation confidence rises. |

Where the Two Lenses Overlap

Quality value combines both ideas. The value side tests whether the price offers enough discipline. The quality side tests whether the business evidence makes the valuation estimate more durable. A company can pass both screens when a strong business trades below a reasonable estimate of value.

Confusion trap: Overlap does not make the concepts identical. Quality can reduce some value-trap risk, but it cannot erase valuation risk. A high-quality company can still disappoint a value lens when expectations, multiples, or cash-flow assumptions leave little room for adverse outcomes.

The same distinction works in reverse. A low multiple can make a company look like a value candidate, but weak cash conversion, fragile margins, high debt, or declining reinvestment returns can weaken the business-quality evidence. Cheapness begins the valuation question. It does not complete the business-quality question.

Same-Company Scenario

Scenario A: A fictional company has high margins, low debt, steady free cash flow, and a long record of reinvesting at attractive returns. The quality lens may view the business as strong because the economics are supported by cash, resilience, and durability. The value lens may still hesitate if the current price already assumes years of flawless execution, margin stability, and continued premium growth.

Scenario B: Another fictional company trades at a low earnings multiple after several disappointing periods. The value lens may start with the possible discount and test whether normalized earnings are being undervalued. The quality lens may reject the same evidence if cash flow is weak, debt flexibility is limited, margins are falling, or the business model no longer supports durable returns.

The difference is not optimism versus pessimism. The difference is the order of proof. Value investing pressures the price and valuation assumptions first. Quality investing pressures durability and cash-support evidence first. When the same company receives different readings, the disagreement usually comes from which risk is more visible: overpayment risk or business-quality risk.

Common Confusion and Failure Modes

| Confusion | Why it happens | Cleaner interpretation |

|---|---|---|

| Cheap means value | A low multiple can look attractive before the business evidence is tested. | Value requires a gap between price and estimated value, not only a low headline ratio. |

| Quality means safe | Strong companies can look more reliable than weaker companies. | Quality can still be priced too richly, and valuation risk can remain high. |

| Metrics prove the style | ROE, ROIC, margins, debt ratios, and valuation multiples can look decisive in isolation. | Metrics need context: accounting quality, cash conversion, cyclicality, reinvestment needs, and expectations can change the interpretation. |

| Quality value is one automatic category | Investors often combine the terms when a strong business appears discounted. | The combined label still needs two separate checks: business durability and price discipline. |

| Style labels create portfolio answers | Comparison language can drift into allocation framing. | The labels are analytical lenses. They do not create a portfolio recommendation by themselves. |

When Each Lens Is More Useful

Quality and value lenses are most useful when they answer different weaknesses in the evidence. The value lens is stronger when price discipline is the missing check. The quality lens is stronger when business durability is the missing check.

| Situation | Value lens helps by asking | Quality lens helps by asking |

|---|---|---|

| A company looks excellent but expensive | How much future strength is already reflected in the price? | Is the strength real, durable, and supported by cash? |

| A stock looks statistically cheap | Is there a reasonable estimate of value above the current price? | Is the cheapness explained by weak economics, leverage, or deteriorating cash flow? |

| Margins and returns look unusually strong | Does the valuation assume those margins continue? | Are returns supported by durable advantages, not temporary conditions? |

| Earnings look temporarily depressed | Are normalized earnings materially higher than current earnings? | Can the business recover without weakening the balance sheet or competitive position? |

| A combined quality-value case appears | Is the discount still present after conservative assumptions? | Does the business evidence support confidence in the valuation range? |

Balanced limitation: Value investing can fail when cheapness reflects permanent business deterioration. Quality investing can fail when strong business evidence is already priced for perfection. Neither lens removes the need for valuation context, cash-flow review, balance-sheet analysis, and expectation risk.

How to Keep the Comparison Clear

A clean comparison separates price, durability, expectation risk, and cash-flow support before style labels are applied. A low price belongs to the value question only after estimated value is tested. High returns on capital belong to the quality question only after durability, accounting quality, cash conversion, and reinvestment needs are checked.

Business strength and valuation discipline can support each other, but they can also conflict. A strong company at an overextended valuation and a weak company at a low multiple both require caution for different reasons. The useful comparison is not which label sounds better. The useful comparison is which uncertainty still needs the most evidence.

FAQ

What is the main difference between quality investing and value investing?

Value investing focuses on price versus estimated business value. Quality investing focuses on business durability, cash-flow support, resilience, and the strength of the company’s economics.

Can a stock be both high quality and value?

Yes. A company can have durable business economics and still trade below a reasonable estimate of value. The overlap is often called quality value, but both tests still need to be checked separately.

Why can a cheap stock fail a quality investing screen?

A cheap stock can fail a quality screen when low valuation reflects weak cash flow, high debt, declining margins, poor reinvestment economics, or a business model that no longer looks durable.

Why can a quality company still fail a value investing screen?

A quality company can fail a value screen when the price already assumes too much future strength. Strong margins, cash flow, and returns on capital do not remove overpayment risk.