A debit spread is an options spread built for a net debit, where the option purchased costs more than the premium received from the option sold. In a common vertical debit spread, the two options use the same underlying asset, the same expiration, and the same option type, but different strike prices. That structure creates a strike-based payoff and risk boundary at expiration.

Definition: A debit spread is a multi-leg options position with an upfront net cost. The net debit, strike width, and final price of the underlying at expiration determine the simplified maximum loss, maximum profit, and breakeven boundary.

The main idea is not that a debit spread is automatically safe. The useful distinction is that the position has a defined expiration payoff shape when compared with an uncovered long option or a net-credit spread. Before expiration, its market value can still move with the underlying price, time decay, implied volatility, bid-ask spread, liquidity, and exercise or assignment conditions.

Key Points

- A debit spread starts with a net debit because the purchased option costs more than the sold option premium received.

- Most vertical debit spreads use the same underlying, same expiration, same option type, and different strikes.

- The strike width and net debit define the simplified expiration payoff boundary.

- A call debit spread and a put debit spread express different directional payoff shapes, but both are debit spreads when they begin with a net cost.

- Expiration payoff is only a simplified boundary. Before expiration, volatility, time decay, liquidity, and exercise or assignment risk can change the position value.

What Is a Debit Spread?

A debit spread is an options spread where the total premium paid is greater than the premium received. The result is a net debit, which is the initial cost of the spread before commissions, fees, and execution effects.

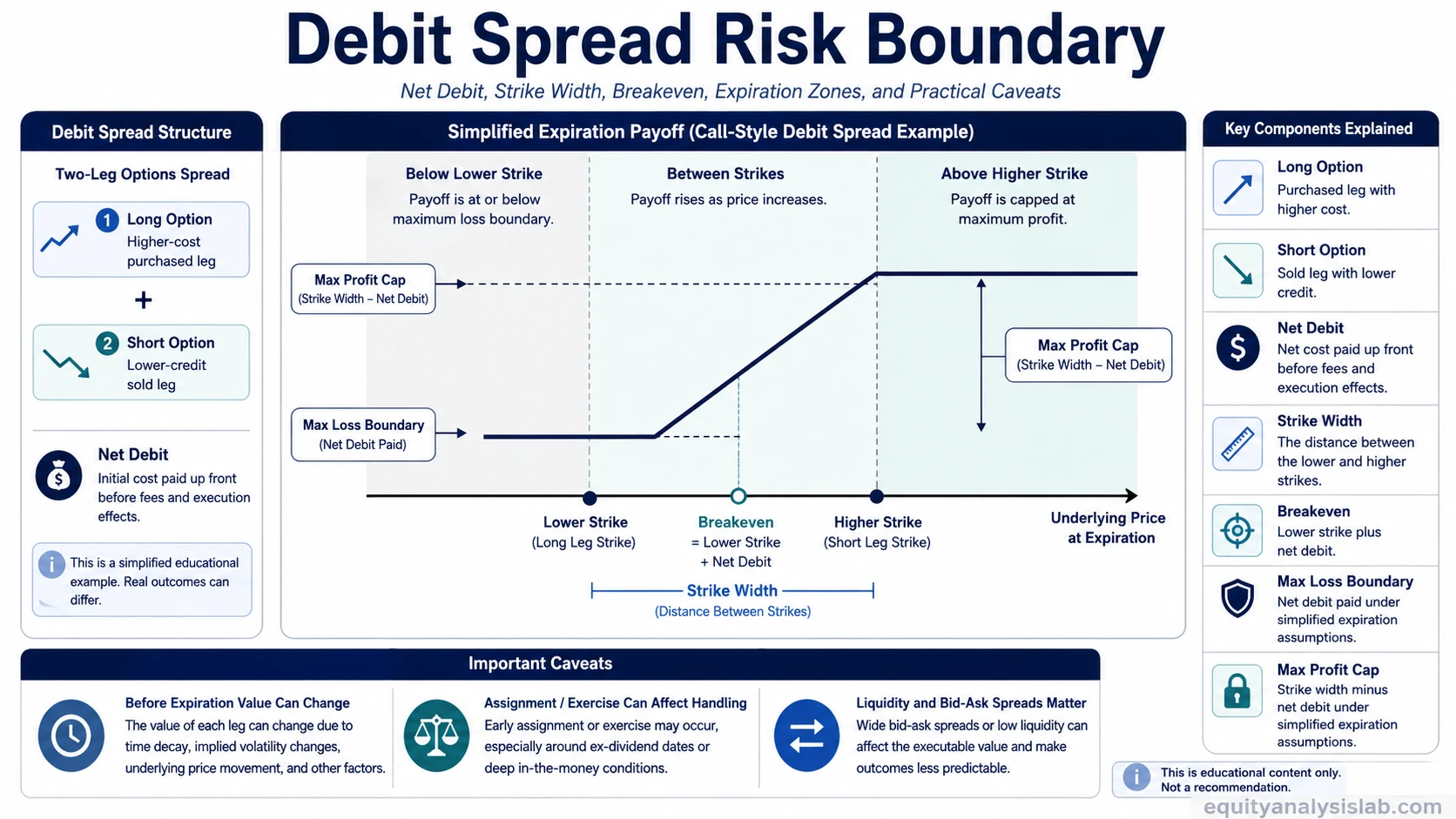

In a standard vertical debit spread, one option is bought and another option is sold on the same underlying asset and expiration date. The options are usually both calls or both puts, but they use different strike prices. This creates a bounded payoff range at expiration instead of the open-ended payoff of a single long option.

The net debit is central because it is part of the breakeven calculation and the simplified maximum loss at expiration. The sold option offsets part of the cost of the purchased option, but it also caps part of the potential payoff beyond the short strike.

How a Debit Spread Is Structured

A debit spread combines a higher-cost long option with a lower-credit short option. The purchased leg creates the main exposure. The sold leg reduces the upfront debit but also creates the payoff cap.

| Structure element | What it means | Why it matters |

|---|---|---|

| Long option | The option bought for a premium | Creates the main directional exposure and defines one side of the spread |

| Short option | The option sold for a lower premium | Offsets part of the cost but caps part of the expiration payoff |

| Net debit | Premium paid minus premium received | Forms the initial cost and simplified maximum loss at expiration |

| Strike width | The distance between the two strike prices | Sets the gross payoff range before subtracting the net debit |

| Expiration date | The date both options expire in a vertical debit spread | Defines the simplified payoff boundary used in standard diagrams |

Because the two legs interact, a debit spread should not be read as two unrelated options. The spread value depends on the combined position, not only on whether the long option gains value.

Debit Call Spread vs Debit Put Spread

A debit call spread uses call options. A common form is a lower-strike long call paired with a higher-strike short call on the same expiration. This is often described as a call debit spread, and the more specific subtype is a bull call spread.

A debit put spread uses put options. A common form is a higher-strike long put paired with a lower-strike short put on the same expiration. The more specific subtype is a bear put spread.

Core distinction: A call debit spread and a put debit spread are both net-debit spread structures. The call version uses calls and has a payoff shape associated with upside movement through the strikes. The put version uses puts and has a payoff shape associated with downside movement through the strikes.

The umbrella debit-spread concept is useful for understanding net debit, strike width, breakeven, and capped expiration boundaries. The exact strike-by-strike mechanics become more specific once the structure is separated into call debit and put debit variants.

Net Debit, Breakeven, and Expiration Payoff

The simplified expiration payoff of a debit spread depends on three linked variables: the net debit, the distance between the strikes, and the underlying price at expiration. The exact breakeven formula depends on whether the spread uses calls or puts.

| Payoff variable | Call debit spread | Put debit spread |

|---|---|---|

| Net debit | Long call premium minus short call premium | Long put premium minus short put premium |

| Strike width | Higher call strike minus lower call strike | Higher put strike minus lower put strike |

| Breakeven at expiration | Lower strike plus net debit | Higher strike minus net debit |

| Simplified maximum loss at expiration | Net debit paid, if the spread expires below the lower strike | Net debit paid, if the spread expires above the higher strike |

| Simplified maximum profit at expiration | Strike width minus net debit, if the spread expires above the higher strike | Strike width minus net debit, if the spread expires below the lower strike |

For example, if a vertical debit spread has a $5 strike width and a $2 net debit, the simplified maximum profit at expiration is $3 before commissions, fees, and execution effects. The simplified maximum loss at expiration is the $2 net debit. This example is only a structure illustration, not a statement about suitability, probability, or expected outcome.

What Can Change Before Expiration?

Expiration payoff tables are useful because they show the final boundary if the options are held to expiration and the simplified assumptions apply. They do not describe every value change that can happen before expiration.

Limitation: A debit spread can gain or lose market value before expiration even when its expiration maximum loss and maximum profit look clearly defined. The spread value can change with the underlying price, remaining time, implied volatility, bid-ask spread, liquidity, early exercise risk, and assignment risk. The net debit is an important boundary, but it is not the only practical variable a reader should understand.

Time decay can affect the long and short option legs differently. Implied volatility can also change the value of both legs before expiration. These effects may be more noticeable when the underlying price is near the strikes, when expiration is close, or when the option market is less liquid.

Assignment, Exercise, and Liquidity Caveats

A debit spread includes a short option. That means assignment can be possible under certain conditions, depending on contract terms, moneyness, expiration timing, exercise incentives, and account-level handling. A debit call spread can still involve assignment risk on the short call, even though the overall position began with a net debit.

Exercise can also create confusion because the long option and short option may not be treated the same way in every scenario. The spread’s simplified payoff diagram assumes clean expiration behavior, but real option handling may involve exercise decisions, assignment notices, settlement rules, and account-level requirements.

Liquidity matters because a debit spread has two legs. Wide bid-ask spreads can make the displayed theoretical value different from the executable price. The spread may also be harder to exit or adjust at a fair price when volume and open interest are thin.

Debit Spread vs Credit Spread

A debit spread and a credit spread are both multi-leg options spreads, but they start from opposite premium structures. A debit spread begins with premium paid. A credit spread begins with premium received.

| Feature | Debit spread | Credit spread |

|---|---|---|

| Opening cash flow | Net premium paid | Net premium received |

| Basic premium logic | Long option costs more than short option premium received | Short option premium received is greater than long option cost |

| Expiration payoff focus | Net debit, strike width, breakeven, and capped payoff | Net credit, strike width, breakeven, and bounded risk |

| Typical concept focus | Paying for a bounded payoff range | Receiving premium while accepting a bounded risk range |

A bull put credit spread is a bullish net-credit structure, not a debit spread. That distinction matters because a bullish directional label does not determine whether the structure is debit or credit. The opening net cash flow and leg construction determine the category.

Related Spread Structures

Debit spread is the umbrella concept for net-debit spread structures. The more specific variants matter when the reader needs to understand the exact strike order, option type, and expiration payoff of a subtype.

Debit-spread structure: net debit, strike width, breakeven, and capped expiration boundaries define the umbrella concept.

Call debit subtype: call-based debit spreads build the payoff boundary between a lower call strike and a higher call strike.

Put debit subtype: put-based debit spreads build the payoff boundary between a higher put strike and a lower put strike.

Credit-spread contrast: the key distinction is whether the spread begins with premium paid or premium received.

FAQ

What is a debit spread?

A debit spread is an options spread that starts with a net debit because the purchased option costs more than the premium received from the sold option. In a common vertical debit spread, the options use the same underlying, same expiration, same option type, and different strikes.

How does a debit spread work?

A debit spread works by combining a long option with a short option. The short option reduces the upfront cost, while the difference between the strikes and the net debit define the simplified expiration payoff boundary.

What is the breakeven on a debit spread?

For a call debit spread, the expiration breakeven is usually the lower strike plus the net debit. For a put debit spread, the expiration breakeven is usually the higher strike minus the net debit.

Can you get assigned on a debit call spread?

Assignment can be possible because a debit call spread includes a short call. The risk depends on the option terms, moneyness, expiration timing, and account-level handling. The presence of a net debit does not remove assignment risk.

What is the difference between a debit spread and a credit spread?

A debit spread begins with net premium paid. A credit spread begins with net premium received. That difference changes how maximum loss, maximum profit, and breakeven are framed at expiration.