Comparing ETFs starts with checking what each fund actually owns and tracks, then testing whether its cost, tracking quality, liquidity, income treatment, domicile, currency exposure, and portfolio role fit the investor’s objective.

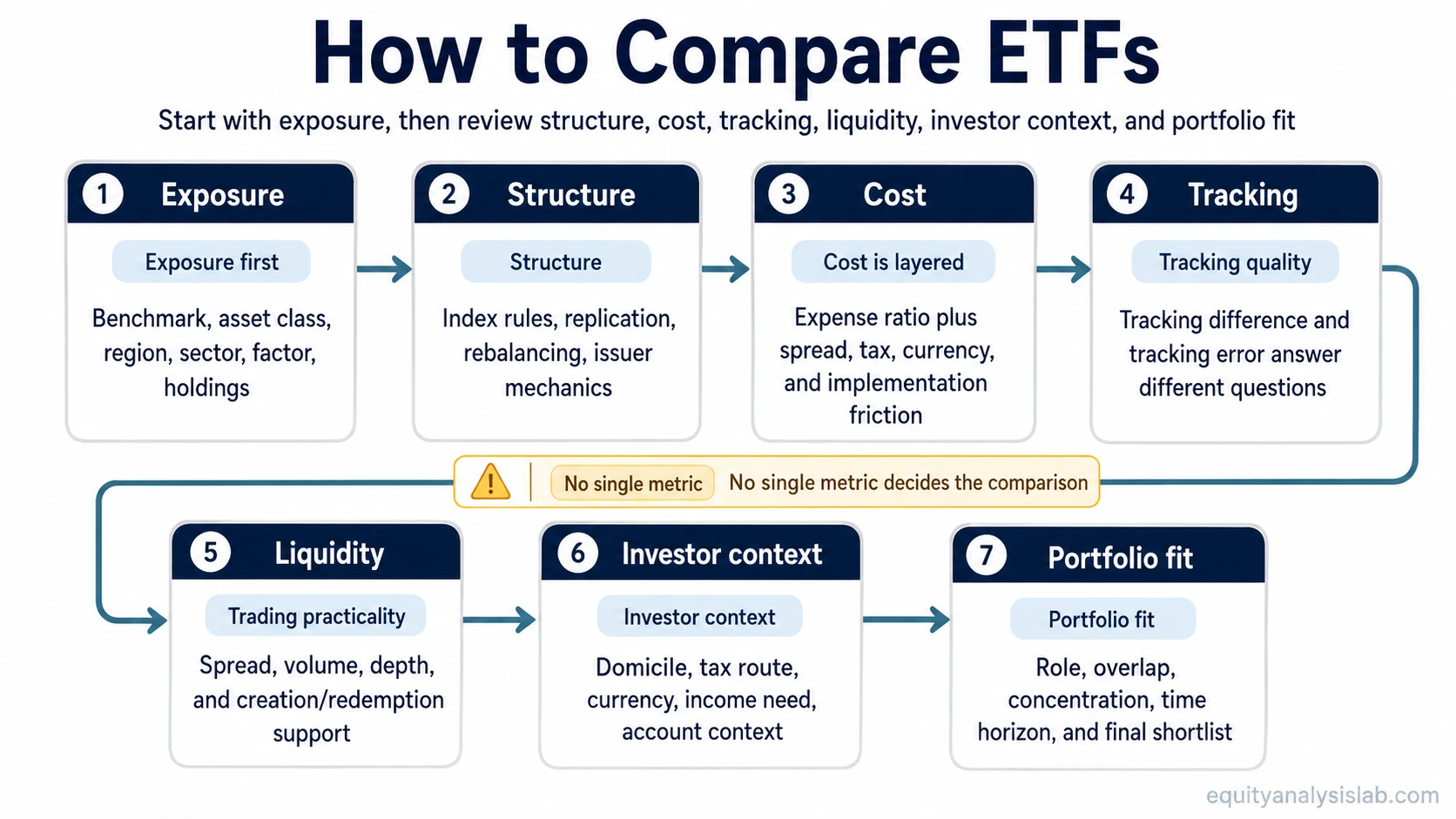

A practical comparison usually moves in sequence: exposure first, structure second, then cost, tracking, liquidity, income treatment, domicile, currency, and portfolio fit. A screener can display ETF fields side by side, but the fields still need interpretation.

A low fee, familiar label, large asset base, or strong past return can point in the wrong direction if the exposure, index rules, trading conditions, or investor-specific tax and currency context do not match the intended use.

Definition: ETF comparison is the process of reviewing two or more exchange-traded funds across exposure, structure, cost, tracking, liquidity, income treatment, currency, domicile, issuer, and portfolio fit before deciding which fund deserves deeper review.

Key Points

- Start with exposure, benchmark, and holdings before comparing fees.

- Compare ownership cost and trading cost, not the expense ratio alone.

- Check tracking quality and liquidity as separate issues.

- Treat distributions, domicile, tax, and currency as investor-specific checks.

- Use fund size and age as viability inputs, not as standalone quality scores.

What ETF Comparison Should Answer

A useful ETF comparison answers four questions before a ranking, shortcut, or sorted screener column becomes persuasive.

| Comparison question | What it tests | Why it matters |

|---|---|---|

| What exposure is being bought? | Asset class, region, sector, factor, index, benchmark, and holdings | Two ETFs with similar labels can hold different securities or weight them differently. |

| How does the fund deliver that exposure? | Index rules, replication method, rebalancing, issuer structure, and fund mechanics | The same headline exposure can behave differently when the underlying rules differ. |

| What does ownership and trading cost? | Fee, spread, liquidity, tracking, tax friction, and currency effects | The visible fee is only one part of the cost picture. |

| Where does it fit? | Portfolio role, time horizon, income need, account context, and risk concentration | A fund can be well built and still be the wrong match for a specific objective. |

ETF Comparison Criteria That Usually Matter

The strongest comparison starts with fund exposure and ends with fit. Cost matters, but it should not move ahead of the question of what the ETF owns and how it is designed to behave.

| Criterion | What to compare | What needs caution |

|---|---|---|

| Exposure and benchmark | Asset class, geography, sector, factor tilt, benchmark, and stated objective | A broad label can hide a narrow or concentrated exposure. |

| Holdings and weights | Top holdings, number of holdings, concentration, overlap, and weighting method | Two funds can share a category while giving very different weight to the largest positions. |

| Index or strategy rules | Selection rules, rebalancing rules, replication approach, and screening methodology | A similar benchmark name does not guarantee a similar construction process. |

| Expense ratio | Annual fund operating cost shown as a percentage of assets | It does not capture tracking, spread, tax, or currency effects. |

| Tracking quality | How closely the ETF follows its benchmark over time | Average benchmark drag and benchmark-relative variability answer different questions. |

| Tracking variability | How much the fund’s benchmark-relative result fluctuates | Tracking error can matter even when the average return gap looks acceptable. |

| Liquidity and spread | Bid-ask spread, trading volume, market depth, and creation/redemption support | Fund size and trading practicality are related inputs, not identical measures. |

| Fund size and age | Assets under management, trading history, closure risk, and operating scale | A larger ETF is not automatically better; a very small ETF may deserve extra viability review. |

| Income treatment | Distribution frequency, dividend policy, accumulation/distribution format, and income consistency | ETF dividend treatment belongs to the income and tax review, not the exposure review. |

| Domicile and tax context | Fund domicile, withholding-tax path, account type, and investor jurisdiction | A tax feature can help one investor and be irrelevant or different for another. |

| Currency and hedging | Base currency, underlying asset currency, share class currency, and hedging policy | The trading currency may not be the same as the economic currency exposure. |

| Issuer and structure | Provider, fund structure, replication method, securities lending policy, and operational transparency | Issuer reputation is useful context, but it does not replace fund-level checks. |

| Portfolio fit | Role, overlap with existing holdings, risk concentration, time horizon, and income need | A strong standalone fund can still duplicate exposure already present in the portfolio. |

Objective Criteria vs Investor-Specific Checks

Some ETF comparison fields can be reviewed in the same way by most investors. Others depend heavily on tax status, account type, base currency, income need, and portfolio role.

| Comparison type | Examples | How to use it |

|---|---|---|

| Objective fund criteria | Benchmark, holdings, weighting, expense ratio, fund size, tracking difference, tracking error, liquidity, bid-ask spread | Use these to compare fund design, implementation quality, and trading practicality. |

| Investor-specific checks | Domicile, withholding tax, account type, currency exposure, hedging preference, distribution preference, portfolio overlap | Use these to decide whether the same ETF fits a specific investor context. |

| Context-dependent evidence | Past returns, yield, AUM growth, issuer reputation, and recent flows | Use these as supporting inputs only after exposure, structure, cost, tracking, and fit are clear. |

Important distinction: Objective criteria can narrow the shortlist, but investor-specific checks often decide whether a fund is suitable for a particular portfolio. Domicile, currency, and income treatment are especially sensitive to personal context and should not be treated as universal advantages.

Common Mistakes When Comparing ETFs

| Mistake | Safer interpretation |

|---|---|

| Expense ratio alone | A low fee can be attractive, but it does not tell the full cost story if tracking quality, spreads, tax drag, or exposure differences are material. |

| Same label, different fund | Two ETFs can both describe themselves as broad equity funds while tracking different indexes, weighting holdings differently, or concentrating exposure in different sectors. |

| AUM as a quality score | Fund size can help assess scale and viability, but large assets do not prove that the exposure, cost, or portfolio role is right. |

| Past performance without context | Return history can reflect exposure, currency, sector concentration, benchmark design, or valuation starting point rather than superior fund quality. |

| Liquidity checked too late | Trading cost becomes visible when the investor actually enters, exits, or rebalances. Spread and market depth should be reviewed before execution becomes urgent. |

Simple ETF Comparison Example

Two ETFs both describe themselves as broad equity funds. One tracks a market-cap-weighted index with heavy concentration in a small group of large companies. The other follows a broader index with more holdings and a different weighting approach.

The cheaper fund may still be less suitable if it creates unwanted concentration or overlaps heavily with existing portfolio holdings. The fund with the higher visible fee may still deserve review if it tracks the intended exposure more cleanly, trades with tighter spreads during normal rebalancing, or matches the desired income and currency profile.

The comparison is stronger when it separates the exposure question from the cost question, then checks tracking, liquidity, distribution treatment, currency, and portfolio role in sequence.

ETF Comparison Route Table

Each comparison field should answer one investor question. If the field becomes decisive or unclear, the narrower explanation belongs with the concept that owns the deeper check.

| Comparison field | What it answers | What can mislead | Deeper check |

|---|---|---|---|

| Exposure and benchmark | What market, asset class, sector, factor, or theme the ETF is designed to represent | A name that sounds broad can still hide concentration or a narrow rule set. | Review benchmark, holdings, and weighting before comparing cost. |

| Holdings and weights | What securities drive the fund’s behavior | Category labels can make different portfolios look similar. | Compare top holdings, sector weights, and overlap with existing positions. |

| Expense ratio | What the fund charges annually at the operating-cost level | The lowest visible fee may not create the lowest all-in outcome. | Use expense ratio as one cost input, not the full decision. |

| Tracking difference | How far the ETF’s result has been from its benchmark result | A small fee can still be offset by implementation drag or structural frictions. | Review tracking difference when benchmark-relative performance matters. |

| Tracking error | How stable or variable the benchmark-relative gap has been | A fund can have an acceptable average gap while showing unstable benchmark-relative behavior. | Use tracking error when consistency around the benchmark matters. |

| Liquidity and spread | How practical it may be to trade the ETF at reasonable cost | Large AUM does not automatically mean tight spreads in every trading condition. | Check ETF liquidity, spread, and market depth before focusing only on fund size. |

| Fund size and age | Whether the fund has operating scale, history, and viability | AUM can become a shortcut that hides weaker exposure or higher all-in cost. | Use AUM and fund age as review inputs, not a quality ranking. |

| Dividends and income treatment | How income is distributed, accumulated, or reported | A higher distribution does not automatically mean a better investment outcome. | Review income mechanics through ETF dividend policy and investor tax context. |

| Domicile and tax route | How fund location and investor jurisdiction may affect tax treatment | A tax-efficient structure for one investor may not apply to another. | Keep domicile and withholding-tax conclusions jurisdiction-specific and cautious. |

| Currency and hedging | Which currency risks the investor is actually taking | The exchange trading currency can differ from the fund’s underlying economic exposure. | Separate trading currency, fund base currency, asset currency, and hedging policy. |

| Portfolio fit | Whether the ETF improves the intended portfolio role | A fund can look attractive in isolation while duplicating existing exposure. | Compare overlap, risk concentration, income need, and time horizon before final review. |

How to Use a Screener Without Letting It Decide

ETF screeners are useful for collecting comparable fields, but a sorted column is not the same as an ETF comparison. Fee, AUM, yield, volume, or past return should be read only after the intended exposure and portfolio role are clear.

A better sequence is to filter for the intended exposure first, remove funds that do not match the portfolio role, then compare costs, tracking, liquidity, income treatment, domicile, and currency. The final shortlist should reflect both the fund’s objective characteristics and the investor’s own constraints.

Limitation: A screener can show available data, but it cannot know whether an ETF’s exposure duplicates existing holdings, creates unwanted currency risk, or fits a specific tax and income situation.

Diagnostic Comparison Checklist

A stronger ETF comparison separates useful evidence from shortcuts that feel decisive too early.

| Comparison behavior | Stronger use | Weaker use |

|---|---|---|

| Expense ratio | Compare alongside tracking, spread, tax context, and exposure | Treat the lowest fee as the automatic winner |

| Fund size | Check scale, viability, and trading practicality | Treat AUM as a fund-quality score |

| Past performance | Compare relative to benchmark, exposure, currency, and starting conditions | Rank funds by return alone |

| Liquidity | Review spread, market depth, and trading conditions | Look only at AUM or average volume |

| Distribution | Match income treatment to investor context | Assume a higher distribution is automatically better |

FAQ

What is the first thing to compare between ETFs?

Start with exposure. Compare the benchmark, holdings, weights, and strategy rules before comparing fees or past performance.

Is the lowest expense ratio always the best ETF choice?

No. A lower fee can help, but tracking quality, spreads, tax treatment, liquidity, currency exposure, and portfolio fit can change the comparison.

Should ETF domicile and currency be compared for every investor?

They should be reviewed when they can affect tax treatment, income routing, withholding tax, reporting, or the currency risk the investor actually holds.