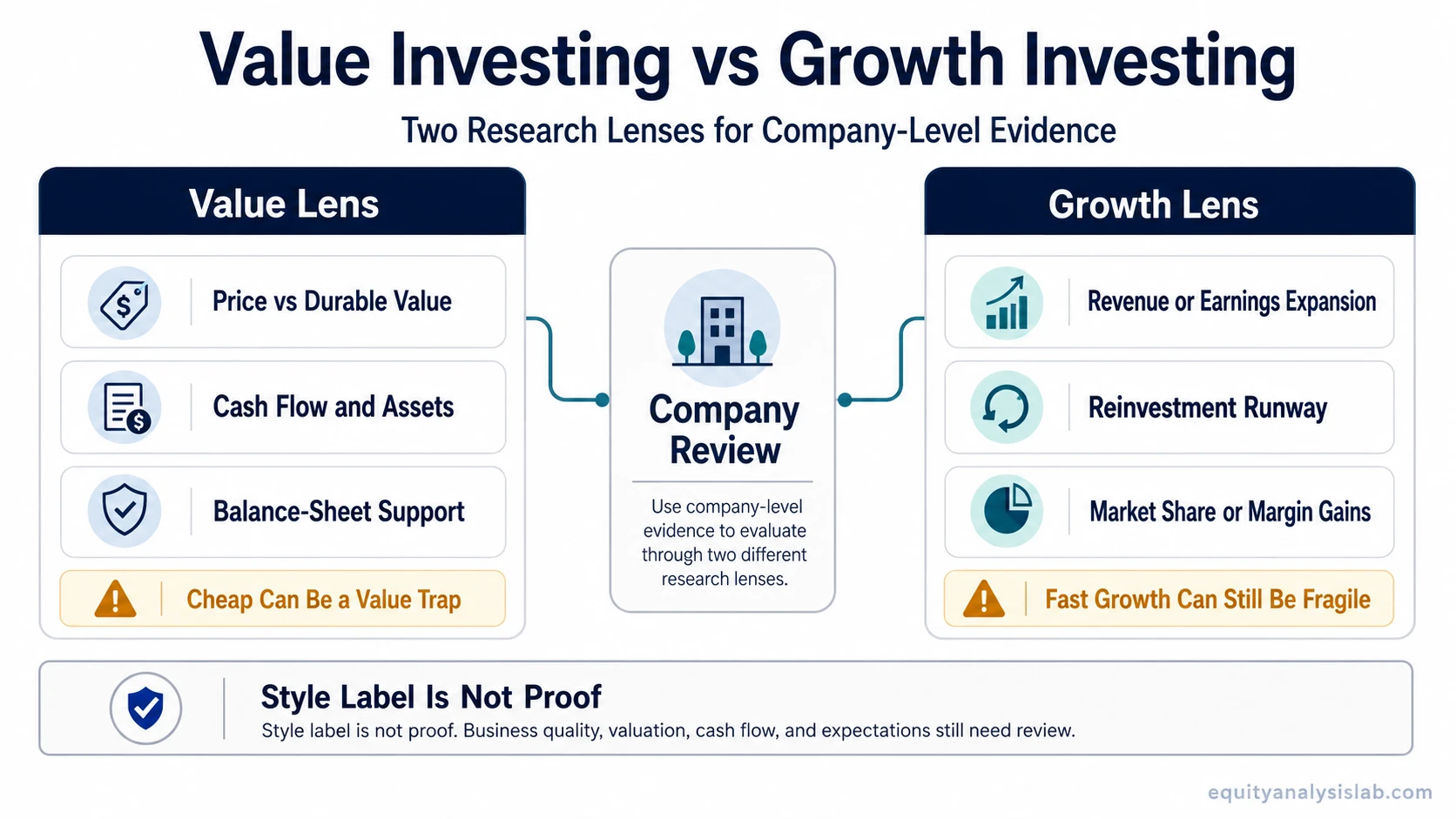

Value investing vs growth investing compares two different research lenses. Value investing asks whether a stock’s price is low relative to durable fundamentals, intrinsic value, assets, earnings, or cash flow. Growth investing asks whether a business can expand revenue, earnings, cash flow, market share, or reinvestment opportunity enough to justify higher expectations.

Neither label proves that a stock is attractive. A cheap stock can still be a weak investment if the business is deteriorating, and a fast-growing company can still be risky if the market already prices in more growth than the business can realistically deliver.

Key Points

- Value investing emphasizes valuation discipline and the risk of overpaying for fundamentals.

- Growth investing emphasizes business expansion, reinvestment runway, and durable earnings or revenue growth.

- A cheap stock is not automatically a good value investment.

- A fast-growing company is not automatically a good growth investment.

- The strongest comparison asks what evidence would make each lens wrong.

Value Investing vs Growth Investing Criteria

The practical difference is not only “cheap versus expensive.” The difference is the question each lens asks before a company is judged.

| Criterion | Value investing lens | Growth investing lens | Main risk if misread |

|---|---|---|---|

| Main question | Is the price low relative to durable value? | Can the business expand enough to justify expectations? | The investor treats a label as proof instead of testing the evidence. |

| Price focus | Current price compared with assets, earnings, cash flow, or intrinsic value. | Current or future price compared with expected business expansion. | A low price can reflect real business decline, while a high price can reflect unrealistic optimism. |

| Business evidence | Stable or recoverable fundamentals, balance-sheet strength, and cash-flow support. | Revenue growth, earnings growth, market-share gains, reinvestment opportunity, and margin expansion. | Surface numbers may hide weakening quality, dilution, competition, or weak cash conversion. |

| Valuation evidence | Low valuation relative to normalized fundamentals, peers, assets, or estimated intrinsic value. | Valuation judged against the durability, scale, and quality of future growth. | Low multiples can be value traps, and high multiples can compress if expectations reset. |

| Earnings / revenue evidence | Earnings and cash flow should support the value case or show recoverability. | Earnings or revenue growth should be strong enough, durable enough, and financially supported. | Reported growth may be less useful if margins weaken, cash flow lags, or share count rises. |

| Typical failure mode | The stock looks cheap because the business is structurally weakening. | The business grows, but not enough to support the valuation already embedded in the price. | The thesis fails even though the headline style label still sounds attractive. |

| Risk control question | What would prove that the discount is justified rather than temporary? | What would prove that growth expectations are too high or too fragile? | The investor ignores the evidence that would invalidate the style lens. |

| Best use as research lens | Testing price-to-value discipline and the quality of the apparent discount. | Testing whether growth, reinvestment, and business quality can support expectations. | The lens becomes too broad and replaces company analysis. |

What Value Investing Looks For

Value investing looks for a gap between market price and business value. The evidence usually centers on valuation discipline: earnings, assets, cash flow, balance-sheet strength, normalized profitability, and whether the current price leaves room for error.

The value lens does not mean buying anything with a low P/E ratio or a low price-to-book ratio. The discount has to be tested against business quality. If earnings are declining, debt is rising, cash flow is weak, or the industry is structurally pressured, the low valuation may be a warning rather than an opportunity.

What Growth Investing Looks For

Growth investing looks for companies that can expand at a rate strong enough to support present and future expectations. The evidence can include revenue growth, earnings growth, free cash flow growth, margin expansion, market-share gains, product expansion, or reinvestment opportunities.

The growth lens does not mean buying any company with fast revenue growth. Growth becomes more useful when it is durable, cash-flow supported, and not fully offset by dilution, falling margins, excessive valuation, or competitive pressure.

Same Company, Different Lens

Consider a hypothetical software company with rising revenue, improving customer retention, and a high valuation multiple. A value-oriented analyst would ask whether the current price already assumes too much future success. That analyst may focus on normalized free cash flow, margin durability, balance-sheet strength, and whether the stock offers enough price-to-value discipline.

A growth-oriented analyst looking at the same company would ask a different question: can the business keep expanding fast enough to justify the premium? That analyst may focus on revenue runway, reinvestment efficiency, market-share gains, customer economics, and whether future earnings can scale without excessive dilution or margin pressure.

The company has not changed. The evidence lens changed. That is why value investing vs growth investing is best understood as a difference in research questions, not a simple split between “cheap stocks” and “expensive stocks.”

Common Confusion: Cheap Is Not Always Value, Fast Growth Is Not Always Attractive

Cheap can be a value trap: A stock may trade at a low valuation because the market expects earnings deterioration, balance-sheet pressure, weak cash generation, or industry decline. In that case, the discount may reflect risk rather than mispricing.

Fast growth can still be fragile: A company can grow revenue quickly while margins weaken, cash flow stays poor, share count rises, or competition reduces future returns. High growth is less useful if the market has already priced in perfection.

Both styles need evidence beyond the label: A value case still needs business durability, and a growth case still needs valuation awareness. The two lenses differ, but both can fail when company analysis is shallow.

How Risk Differs

Value investing risk often appears when the apparent discount is attached to a weakening business. The main risks include value traps, declining fundamentals, weak balance sheets, poor cash conversion, management misallocation, and industry deterioration.

Growth investing risk often appears when expectations are too high. The main risks include multiple compression, missed growth expectations, rising competition, reinvestment inefficiency, margin pressure, dilution, and a gap between narrative growth and cash-flow quality.

The shared risk is style overconfidence. A stock can be described as value or growth while still failing a deeper review of business quality, valuation, earnings durability, cash flow, and balance-sheet risk.

Can Investors Use Both Lenses?

Yes. Value and growth are not always mutually exclusive. A company can have growth characteristics while still requiring valuation discipline, and a value-oriented stock can still need some evidence of earnings stability, recovery, or reinvestment quality.

The safer framing is not whether one style is universally better. The useful question is which lens fits the research problem. If the main issue is whether the market price is too low relative to durable fundamentals, the value lens is more relevant. If the main issue is whether future expansion can justify demanding expectations, the growth lens is more relevant.

When the Growth Lens Becomes Too Optimistic

The growth investing lens becomes weaker when expansion depends on assumptions that are difficult to sustain. Warning signs can include slowing revenue growth, falling margins, weak free cash flow, heavy dilution, high customer acquisition costs, or valuation multiples that leave little room for disappointment.

This does not mean a high-multiple company is automatically unattractive. It means the growth evidence has to be strong enough to carry the expectations already embedded in the price.

FAQ

Is value investing safer than growth investing?

Not automatically. Value investing can reduce the risk of overpaying, but a cheap stock can still be risky if the business is deteriorating. Growth investing can be risky when expectations are excessive, but some growth companies may have strong business quality and durable cash-flow potential.

Can a stock be both value and growth?

Yes. A company can have growth characteristics and still trade at a price that appears reasonable relative to fundamentals. The categories are research lenses, not fixed labels that fully describe a company.

Is growth investing only about technology stocks?

No. Technology companies are often associated with growth investing, but the growth lens can apply to any business with durable expansion in revenue, earnings, cash flow, market share, or reinvestment opportunity.

Is value investing only about low P/E stocks?

No. A low P/E ratio can be part of a value case, but it is not enough by itself. Value investing also requires judgment about earnings quality, cash flow, balance-sheet strength, business durability, and whether the market discount is justified.